“Bridge from education to employment”

|

| Irene Notias - Chairwoman Founder & Director Project Connect |

hosting people from the governmental, academic and business world, as well as organizations active in helping the young generation to be linked with the work market and reduce brain drain. Among the organizations focusing on the young generation were ReGeneration, associate of Project Connect and the AIESEC. Project Connect presented its humble project where Ms Irene Notias emphasized the need for synergy in order to increase the young generation’s employability, inside and outside of shipping! The outcome was to cooperate under specific quality standards for more efficient internship programs and in order to enhance chances to get a job for the next generation of Greece, meeting the goal of Project Connect.

The Project Connect initiative is a non–profit organization, created in May 2015 by a team of shipping industrialists, business consultants, HR experts, and students who volunteer their services and time. It is based on New York corporate office organizational structures, systems and methods. It bridges shipping and business school students to the Shipping community. It is a work in progress which welcomes funding so it can function effectively to help sustain excellence in Greek Shipping. The team at this NPO enjoys hosting “fun” events for worthy causes, hence “fun-d-raising”.

Dry Bulk Market Report: Recovery will take at least one more year say 94\% of respondents in S&P Platts Survey

The survey conducted over August and September involved around 120 dry bulk market participants, with respondents including shipowners, ship-operators, charterers, shipbrokers and analysts. Those polled represented all dry bulk sectors including the Capesize, Panamax, Supramax and Handysize markets.

The frustration over the slow recovery of the dry bulk market is evident with most participants, a whopping 94\% of the respondents, saying the market will need more than a year to recover, while 61\% do not see a recovery over the next three years. A similar survey conducted by Platts in July 2015 showed 89\% expecting a recovery after one year and 54\% anticipating improvement in three years. With the dry bulk market showing a semblance of stability since the second half of this year, the shipowners’ camp appears to be a tad more confident. The charterers appeared more bearish compared to shipowners with 61\% of all charterers convinced that it will take more than three years for this sector to recover, while more than half of the owners (52\%) think it could recover in less than three years. On the contrary, the shipowners were more bearish than charterers during the 2015 survey. “To be realistic [the market] won’t improve dramatically even by then,” said a ship-operator source.

TOO MANY SHIPS… REALLY?

It came with a complete lack of surprise that ship recycling and fewer newbuilding orders were touted as the most important factors that would help the market recover. The overwhelming majority – 80\% of respondents – believe that tonnage supply is the main issue. Only 20\% ranked an increase in ton-mile demand ahead of scrapping and curtailed newbuilding orders, as vital factors to help the market recover. Among the various sectors of the dry bulk market, 44 \% of the respondents think Capesize vessels require the most scrapping. The Supramax vessels were chosen by 26\% of respondents, while 25\% went for Panamax. However, only 5\% chose the Handysize sector as the one that needs large-scale scrapping. “Tonnage growth has been largest for Capesize [vessels] but demand growth has been subdued for iron ore and coal,” said Jayendu Krishna, a director at Drewry Maritime Advisors, adding that demand from these would not grow as it has done historically. According to Krishna, it is difficult to anticipate that coal and iron ore will grow at the rate it did in the past. “Volumes have grown but not tremendously. Also very large ore carriers [VLOC] and Valemaxes have been ordered. This will also pressure [demand for Capesizes]. But new Capesize cargoes are not emerging. Bauxite is seen from West Africa to China. But that is not going to be a savior,” he said. Data from Bancosta Research show that during the first three quarters of 2016, 11.28 million dwt of Capesizes and 7.07 million dwt of Panamaxes were scrapped. For Supramax and Handysize segments, scrapping totaled 3.12 million dwt and 2.15 million dwt respectively.

MOVEMENT IS MONEY

During the beginning of the year, when returns across most dry bulk sectors were below operating expenses (opex), the talk of layup was big as a temporary measure to control vessel supply. According to market estimates during Q1 2016, a few hundred ships were pulled out of the market and put into hot or cold layup. With the scrapping rates getting better during the first half of the year along with improved demand, shipowner returns were able to cover opex, which saw the talks of laying up ships evaporating. Layup didn’t find much favor among the respondents with 48\% of the view that “shipowners are more worried about cash flow” — a reason why layup did not catch on as a huge trend.

Only 19\% felt that fragmented ownership deterred laying up of ships. “As rates picked up from the lows seen in Q1, talk of laying up vessels has reduced as most shipowners seek to continue operating as long as rates are still able to cover their running cost. Some shipowners also face pressure from banks to continue operation in order to meet repayment obligations,” said Chong Hui Ru at Bancosta Research. It’s a fact that shipowners are under a lot of pressure from their lenders to show that cash flow is in order for the financial

institutions to continue supporting them and refinancing the ships, a researcher with a shipbroking house said. Furthermore, because of the low concentration of shipowners in the dry bulk market, one shipowner idling his ships is perceived as helping out the neighbor, who will carry on operating his fleet, the researcher added. The strategy of running a shipping business on cash flow is unsustainable in the long run and the current environment seems to be a ripe recipe for the consolidation of the industry as shipowners play the survival game of seeing who runs out of cash first. “While this will be a painful process for shipowners, the industry would benefit in the long term as excess capacity is permanently removed. In comparison, the laying up of vessels only serves to delay the market recovery for dry bulk shipping, as vessels are able to return to operation as soon as rates pick up,” Bancosta’s Hui Ru said. The overall costs of laying up a ship, particularly in cold layup, are still very delicate to assess, specifically in regards to the damage sustained by the engine, electronics and other hardware of the ships while they are turned off. “Laying up a vessel might represent a cost saving exercise in the short term, but a mightier cost in the long term,” the researcher with the shipbroker said.

NEW LADIES IN TOWN

While Supramaxes have indeed been quite resilient, this sector is facing some internal competition as the popularity of Ultramax vessels increases. These slightly larger ships in the Supramax family boast a size of 60-64,000 dwt and an improved design, which allows better fuel efficiency. The flurry of Ultramax deliveries could apply pressure on the Supramax sector’s ability to generate cash. “It is good to see such a healthy grain season, but the trade barriers that are increasingly lifting up in the steel industry will eventually translate in fewer steel stems moved about, which had heavily contributed to support Supramax rates,” the researcher added.

Close to 150 Ultramax size vessels have been delivered during the first nine months of 2016. The effect of a burgeoning Ultramax fleet size was not immediately seen on the Panamaxes or the Supramax sectors by 65\% of respondents. They perceive these sectors either have their niche markets or that the intrinsic demand still remains for them. Considering the geographies of the respondents, 56\% of those based in the west of Suez, think the Ultramaxes are eroding demand for Supramax and Panamax vessels. Only 29\% of respondents from the east of Suez thought along the same lines. “It seems possible for the Supramax segment to give way to the Ultramaxes, due to increased fuel efficiency and cost savings when the larger carrying capacity of Ultramaxes is fully utilized.

This can make a large difference when trading margins are thin, as is the case currently with most commodity prices pressured due to oversupply,” Bancosta’s Hui Ru said. A few market sources echo that the Ultramax ships have already started to impact the Supramax vessels, while not having much of an effect on the Handysize tonnage. Expectations are rife that in the next three to four years, more Ultramax ships could eat into the Supramax vessels’ cargo share with the parcels of minor bulk products increasing. “Maybe for expensive cargoes like grains, it does not make sense to load additional volumes as we won’t know if it would get sold. But for coal, I don’t see any reason why with time, a larger vessel won’t help,” a second source with a ship-operator said.

Source: S&P Platts

An Equinox Maritime Case Study!

|

Franman Signed an Exclusive Cooperation Agreement with WME for the Greek Market

The company has extensive experience in fire engineering, system building, process, product and systems development within air-gas separation services and commissioning. Notably, it has developed a method for regeneration of air-gas separation membranes – a technique which up until now has not been available in the industry by other suppliers.

WME focuses on delivering innovative engineering services as well as cost efficient and high quality systems, according to leading international standards, including NORSOK, DNV, NFPA and BV, among others. WME holds numerous references within Maritime and Offshore installations as well as chemical industry systems, worldwide.

The new cooperation agreement between Franman Ltd. and WME allows for further development of Franman’s Shipbuilding Equipment portfolio with reliable Fire Protection and Nitrogen Generator systems of a prominent European maker.

Source: Franman

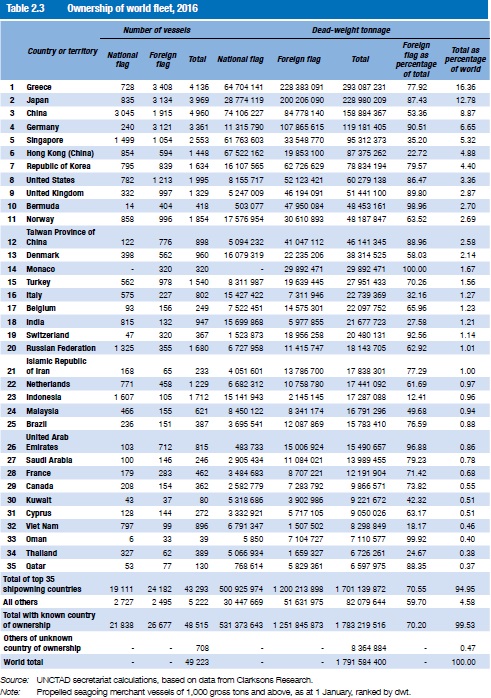

Hellas: Shipping Fleet Retains World Crown says latest UNCTAD Report

Hellas’s share grew to 16.36\% from 16.1\% in terms of dwt capacity, as all other competitors saw their fleets diminish, with the exception of Singapore.

The global commercial shipping fleet in terms of dwt grew by 3.48 per cent in the 12 months to 1 January 2016 (figure 2.1), the lowest growth rate since 2003. Yet the world’s cargo-carrying shipping capacity still increased faster than demand (2.1 per cent; see chapter 1), leading to a continued situation of global overcapacity. In total, as at 1 January 2016, the world commercial fleet consisted of 90,917 vessels, with a combined 1.8 billion dwt. The highest growth was recorded for gas carriers (+9.7 per cent), followed by container ships (+7.0 per cent) and ferries and passenger ships (+5.5 per cent), while general cargo ships continued their long-term decline, with the lowest growth rate of major vessel types (table 2.1). Their share of the world’s tonnage is currently only 4.2 per cent, down from 17 per cent in 1980 (figure 2.2). In 2015, there were 211 new container ships delivered, less than half the number (436 ships) delivered in the peak year of 2008. However, as vessel sizes in this market segment have increased significantly, in terms of container-carrying capacity, 2015 set a historical record in the building of container ships. Globally, shipyards produced 1.68 million TEUs in 2015, an increase of 12.7 per cent over 2014 and 12.4 per cent over the previous peak number of deliveries in 2008. The average size of container ship newbuildings has risen by 132 per cent over the last seven years. Only 5 per cent of TEUs built in 2015 were geared ships (that is, ships that carry their own container-handling equipment), compared with 12 per cent in 2008. Large container ships invariably depend on the availability of ship-to-shore container cranes in terminals, still a challenge for some smaller seaports in developing countries.

Age distribution of world merchant fleet

At the start of 2016, the average age of commercial ships had reached 20.3 years, a slight increase over the previous year (table 2.2). Following additions to the fleet over the last 10 years, the current average age remains low, compared with previous decades. There were slightly fewer newbuildings and somewhat reduced scrapping activity, as many ships are too new to be demolished. Among the main vessel types, only dry bulk carriers were newer in early 2016 than in early 2015; 42.8 per cent of dry bulk ships are 0–4 years old. The oldest ships are general cargo carriers (24.7 years). The age distribution of the fleet also reflects the growth in vessel sizes over the last two decades. In particular, container ships have increased their average carrying capacity; those built 15–19 years previously have an average size of 28,516 dwt, while those built in the last four years are on average 2.8 times larger, with an average size of 79,877 dwt. In the early 2000s, a typical dry or liquid bulk ship was 2–3 times larger than a container ship newbuilding, while at present new container ships are the vessel type with the largest average tonnage.

REGISTRATION

The tonnage registered under a foreign flag (that is, where the nationality of an owner differs from the flag flown by a vessel) is 70.2 per cent of the world total (table 2.3). The system of open registries (that is, where the owner and flag are from different countries) has been an opportunity for many developing countries – including many small island developing States, such as the Marshall Islands, and least developed countries, such as Liberia – to provide the services of vessel registries.

At the same time, the majority of shipowners remain in developed countries, and it is due to the system of open registries that they may remain competitive against fleets owned by companies based in developing countries. For example, under the flags of Liberia, the Marshall Islands or Panama, an owner from Germany or Japan can employ thirdcountry seafarers, for example from Indonesia or the Philippines, who work for lower wages than their German or Japanese colleagues.

As at 1 January 2016, Panama, Liberia and the Marshall Islands continued to be the largest vessel registries, together accounting for 41.0 per cent of world tonnage, with the Marshall Islands recording the highest growth among major registries, at 12 per cent over 2015. The top 10 registries account for 76.8 per cent of the world fleet in terms of dwt. More than 76 per cent of the world fleet is registered in developing countries (including many open registries), a further increase over 2015. Some nationally flagged fleets are also nationally owned. Notably, in countries with long coasts and important cabotage and interisland traffic, national legislation often limits the options of shipowners to flag out. For example, many of the ships flying the flags of China, India, Indonesia and the United States are deployed on cabotage services.

With regard to the share of regional groups among the national flags of the world fleet, 11.42 per cent of the 12.97 per cent of tonnage registered in Africa flies the flag of Liberia and 11.07 per cent of the 11.49 per cent of tonnage registered in Oceania flies the flag of the Marshall Islands. Put differently, 88 per cent of the African-registered fleet flies the flag of Liberia and more than 96 per cent of the Oceania-registered fleet flies the flag of the Marshall Islands. Different registries focus on different vessel types. Antigua and Barbuda has the largest market share of general cargo multipurpose vessels, while Liberia is the most important registry for container ships, the Marshall Islands for oil tankers and Panama for dry bulk carriers. One reason for such specialization is traditional linkages with shipowning countries. Japan – with a large share of dry bulk carriers – often registers its ships in Panama. Germany – specializing mostly in container ships – has a close relationship with Liberia; the two States have an income tax treaty or double taxation agreement, which is beneficial for German officers employed on ships flagged in Liberia (German Federal Ministry of Finance, 1975).

source:hellenic shipping news

Hellenic Society for Systemic Studies - Professional Systemic in Action Conference:

|

Nakilat transitions LNG Mekaines to in-house management

|

With a cargo carrying capacity of 266,476 cubic meters, Mekaines is wholly-owned by Nakilat and chartered by Qatargas. The vessel built in South Korea by Samsung Heavy Industries was delivered in March 2009 and has been in service ever since.

Mekaines is the second Q-Max vessel that will come under the management of Nakilat Shipping Qatar Ltd. (NSQL) this year, bringing the total number of vessels managed by NSQL to 10, comprising of 6 LNG and 4 LPG carriers.

About Nakilat

Nakilat is a Qatari LNG transport company providing an essential transportation link in the State of Qatar’s LNG supply chain. Its LNG shipping fleet is the largest in the world, comprising of 63 LNG vessels. Nakilat also owns and manages four large LPG carriers. Nakilat operates the ship repair and construction facilities at Erhama Bin Jaber Al Jalahma Shipyard in Ras Laffan Industrial City via two strategic joint ventures: N-KOM and NDSQ. Nakilat also offers a full range of marine support services to vessels operating in Qatari waters.

www.nakilat.com.qa

Celestyal Cruises Announces Its Collaboration with AuraPortal

Celestyal Cruises will derive numerous benefits from its collaboration with AuraPortal, including:

• Full modeling and mapping of the corporate business processes in an effective way, without the need for actual programming.

• An end-user-friendly, intuitive, rational working environment which can be used without training.

• Bundled BPM, CRM, and document management with a portal solution that empowers users and reduces dependence on IT.

• Simultaneous execution of hundreds of procedures and processes for enhanced operational effectiveness and reduced response times.

• Document integration.

• Reduction of use of consumables, such as paper and toner, resulting in a “greener” company.

Celestyal Cruises will initiate its use of AuraPortal after a one-year period during which all necessary prerequisites, such as user-role hierarchy, internal corporate hierarchy, allocation to corresponding vessels and amendment of the existing hardcopy forms, etc., will be satisfied. During this period a number of core processes will be implemented within AuraPortal for testing and modification of the suite before its installation throughout the enterprise. Following this introductory year of set-up and testing, the AuraPortal BPMS will host the full range of Celestyal Cruises processes and will provide the company with a timely, efficient and user friendly tool to interconnect all business processes and document management activities between its land-based operations and its vessels.

“The global landscape is changing and moving over to an era of digital transformation,” Konstantinos Smirlis, MIS Director of Celestyal Cruises. “AuraPortal is the platform which will incorporate new digital technologies into our current processes and also will focus on ‘business process agility’ so Celestyal Cruises can respond effectively to changing market dynamics.”

About Celestyal Cruises

Celestyal Cruises is the only home-porting cruise operator in Greece and the preeminent cruise line serving the Greek Islands and the island of Cuba. The company operates five mid-sized ships, each one cosy enough to provide a highly personal service. Every cruise focuses on true cultural immersion, offering an authentic experience of the regions in which the vessels sail.

Sustainability

Celestyal Cruises is deeply committed to sustainability and ethical business practice. The company supports the local communities in the destinations it visits, particularly in the field of education. Since 2015, more than 1,000 students on the islands of Milos, Patmos and Ios have enjoyed a ‘journey to knowledge’ by attending the Museums Program, an initiative by Celestyal Cruises to bring interactive exhibits from the highly respected Herakleidon Museum to remote areas so that students can learn first-hand about the connection between science, art and mathematics. In addition to the above program, Celestyal Cruises supports cultural NGOs as well as promoting entrepreneurship, marine student development and child welfare.

ISO certification

Following the successful ISO 9001/14001 auditing of two of the company’s ships and the company’s office, Celestyal Cruises’ operations are now certified in accordance with ISO 9001/14001 standards. This relates to the entire spectrum of cruise ship management including technical, hotel and crew management; the certifying authority is DNV-GL, which is by far the biggest and most respected classification society in the marine industry.

Awards

In 2016, the company won the prestigious Editor’s Pick award from Cruise Critic UK, the world’s largest online cruise community, in the ‘Best Value for Money (Ocean)’ category. Celestyal Cruises has enjoyed recognition in such prestigious awards as the Greek Tourism Awards (winning gold and silver in four categories in 2016); the Efkranti Awards; the HR Community Conference & Awards; and was finalist in the UK’s WAVE Awards.

For more information, please visit www.celestyalcruises.com

Facebook: (full URL) https://www.facebook.com/CelestyalCruises

YouTube: (full URL) http://www.youtube.com/user/CelestyalCruises

Google+: http://plus.google.com/u/1/+celestyalcruises

Twitter: @celestyalcruise | Pinterest: http://pinterest.com/celestyalcruises

Instagram: https://www.instagram.com/celestyalcruises

Foursquare: https://foursquare.com/v/celstyal-cruises

Poseidon Med II engages National Authorities towards the development of the regulatory framework for the LNG bunkering in Greece

|

The event, which brought together representatives from key project partners (DEPA, DESFA, Lloyd’s Register & Rogan Associates) with public officials, gave the chance to present to public authorities the scope and objectives of Poseidon Med II project as well as the progress already achieved. Specific emphasis was given to the work on regulatory issues, as well as on the issuance of necessary permits & licences for the construction of the relevant port infrastructures.

During the workshop, the participants thoroughly discussed the international environmental and safety standards and provisions that should be incorporated into the national strategic policy framework for alternative fuels, so that LNG will be a feasible and available option for the shipping society in Eastern Mediterranean, meeting the marine fuel sulphur limits by 2020.

This event offered an excellent opportunity for establishing synergies with national authorities, to ensure adequate and effective regulatory framework for LNG bunkering will be in place.

What is Poseidon Med II project?

Poseidon Med II project is a practical roadmap which aims to bring about the wide adoption of LNG as a safe, environmentally efficient and viable alternative fuel for shipping and help the East Mediterranean marine transportation propel towards a low-carbon future. The project, which is co-funded by the European Union, involves three countries Greece, Italy and Cyprus, six European ports (Piraeus, Patras, Limassol, Venice, Heraklion, Igoumenitsa) as well as the Revithoussa LNG terminal. The project brings together top experts from the marine, energy and financial sectors to design an integrated LNG value chain and establish a well-functioning and sustainable LNG market.

a photo from the event

Cyprus shipping fleet in ‘quantitative stagnation’: But 4\% of world shipping fleet controlled from Cyprus

However, comparing the statistics of the last 15 years, one can easily diagnose that the Cyprus Fleet has not increased for many years, according to Cyprus Shipping Chamber Director General Thomas Kazakos.

“This quantitative ‘stagnation’ remains, despite maintaining the very competitive Shipping Taxation System and the Cyprus Flag in the ‘White Lists’ of quality ship registers in relation to high levels of maritime safety,” Kazakos said, adding that there are a number of reasons to this, amongst them being the imposition of the Turkish embargo on Cyprus ships, as well as the limited promotion of shipping abroad, due to lack of sufficient available public funds.

“Today, Cyprus is the largest third-party shipmanagement centre in Europe and one of the largest crew management centres in the world. A substantial number of shipowning, shipmanagement and shipping related companies maintain fully-fledged offices and conduct their international operations and activities from Cyprus.

“It is estimated that approximately 4\% of the world’s fleet and around 20\% of global third-party shipmanagement activities are controlled from Cyprus.”

Kazakos said that whilst there was a noticeable increase in shipmanagement revenues during the first half of 2015, with total revenues rising to EUR 464 mln, this amount was slightly decreased in the second half of 2015, which, as turnover (not value added), corresponds to 5.2\% of Cyprus’s GDP. This is the second highest level of revenues reported since 2010.

“Cyprus has also recently become more attractive to Greek shipping professionals, with Greek shipowners and shipmanagement companies seeking to transfer part of their operations to Cyprus amidst the uncertainties surrounding the Greek economy.”

“Based on a study which was recently commissioned by the Ministry of Transport, Communications and Works on the ‘Future of Cyprus Shipping’, we were pleased to note that the contribution of the shipping sector to the Cyprus economy (according to data from the Statistical Service) is even higher than what was originally expected and currently stands at 7\% GDP,” Kazakos said.

“In terms of value added, this high level of financial contribution, becomes even more important, if one considers that during the last eight years at least, the freight rates remain internationally too low and a number of international shipping sectors are fighting for their commercial survival, due to the ongoing, unsatisfactory development of world trade. In addition, it is worth mentioning that only in very few other maritime developed countries, does the financial contribution of the domestic shipping industry reach such a high level.”

Source: Financial Mirror

![]()

Powered by ![]() © Μaritimes 2019

© Μaritimes 2019