The American P&I Club reports positive developments in 2016

- positive investment performance

- increased net tonnage by 10\%

- American Hellenic’s tonnage ahead of projections

- Eagle Ocean Marine remains profitable

The American P&I Club, one of the 13 members of the International Group of P&I Clubs attracted maximum capacity at events held in two of the world’s major shipping hubs, Piraeus and London on December 7th and 9th 2016 for their annual Market Presentations. Placing emphasis on and crediting the know-how of the people behind the Club’s service, the Club’s Managers, SCB Inc. as well as the Club’s subsidiary American Hellenic Insurance Company’s CEO made a series of presentations highlighting the following positive developments:

- the Club continues to expand it service capabilities with the opening of an office in Houston

- investment performance shows positive despite volatile markets

- that the Club has been successful in increasing its net tonnage by 10\% since last 2016 renewal date

- American Hellenic’s insured tonnage ahead of projections for year end

- Eagle Ocean Marine, the Club’s fixed P&I premium cover in conjunction with Lloyds Underwriters continues to increase in volume and remains profitable

Coming in to the Club’s centennial year, Joseph Hughes, CEO and Chairman of SCB Inc, Managers of the Club, explained that the Club continues to expand it service capabilities with the opening of an office in Houston, making it the only IG P&I Club based in the region with full claims handling abilities and emphasized that “the recent years of the unstable economic environment has strengthened the Club’s uncompromised solidarity with its membership in difficult times.” Mr. Hughes then went on to report that Eagle Ocean Marine, the Club’s fixed P&I premium cover in conjunction with Lloyd’s Underwriters continues to increase in volume and remains profitable.

Vince Solarino, COO and President, advised on the global strategy of growth through its regional business development plans implemented over recent years. He explained that this strategy played a key role in the Club’s net tonnage growth of approximately 10\% during the ongoing 2016 policy year despite the greater insurance industry dealing with the continuing consequences of the recession as well as increasing competition and capacity.

Ilias Tsakiris CEO of the Club’s subsidiary American Hellenic Hull Insurance Company, Ltd. provided the update on the current market position of the now fully licensed and active insurance company indicating that the insured tonnage is ahead of projections for year end with a well-balanced and healthily diversified portfolio both regionally by broker production as well as by vessel type.

The presentations were concluded by Dorothea Ioannou, Global Business Development Director, who gave insight and a picture panoramic tour on the people behind the Club and its history; from the Club’s birth in 1917 arising out of WWI sanctions, up to the leadership of Hughes and Solarino taking the Club from a domestic US insurer in the 90’s, to global insurer and member of the IG, with five times more tonnage and a service reach and capability leading to six offices world-wide today. Ms. Ioannou stated that “it is the people that make all the difference”.

Both events which took place at the Piraeus Marine Club and Trinity House respectively attracted over 500 people when combined, with major names in both the shipowning and broking sectors in addition to the greater shipping cluster sectors.

The American Club

American Steamship Owners Mutual Protection and Indemnity Association, Inc. (the American Club) was established in New York in 1917. It is the only mutual Protection and Indemnity Club domiciled in the entire Americas and its headquarters are in New York, USA.

The Club is a member of the International Group of P&I Clubs, a collective of thirteen mutuals which together provide Protection and Indemnity insurance for some 90\% of all world shipping. In addition to full cover for Protection and Indemnity, the Club offers Freight, Demurrage and Defense as well as Charterers’ Liabilities risks. In recent years, the Club has grown and diversified its services, offering also fixed-premium solutions and H&M subsidiary insurance options.

The American Club has been successful in recent years in building on its US heritage born from the merging of all nationalities, to create a truly international insurer with a global reach second-to-none in the industry. Day to day management of the American Club is provided by Shipowners Claims Bureau, Inc. also headquartered in New York.

The Club is able to provide local service for its members across all time zones, communicating in eleven languages, and its Managers have subsidiary offices located in London, Houston, Piraeus, Hong Kong and Shanghai, plus a worldwide network of correspondents.

For more information, please visit the Club’s website: http://www.american-club.com/ .

P&I Insurance

Protection and Indemnity insurance (commonly referred to as "P&I") provides cover to shipowners and charterers against third-party liabilities encountered in their commercial operations; typical exposures include damage to cargo, pollution, death/injury or illness of passengers or crew or damage to docks and other installations.

Running in parallel with a ship's hull and machinery cover, traditional P&I cover distinguishes itself from usual forms of marine insurance by being based on the not-for-profit principle of mutuality where Members of the Club are both the insurers and the assureds.

|

| The American Club’s Piraeus team with the Managers of SCB Inc. |

|

| Nikos Tourvas (The Aegean Experience), Joanna Koukouli and Antonis Bavas (The American Club), Ioannis Roussos (Rev Maritime Ltd.) |

|

| Maria Mavroudi (The American Club), Yiannis Pavlakis (Faros Marine Services S.A.), Capt. Nikolaos Liadis (Genimar Shipping & Trading S.A.), Tom Hamilton (The American Club) |

|

| Room view |

|

| Audience view with the BoD members of the American Club, including Panayiotis J. Christodoulatos (Ikaros Shipping and Brokerage Co., Ltd.), George Vakirtzis (Polembros Shipping, Ltd.), Angelos D. Kostakos (Oceanstar Management, Inc.), Elias Gotsis (Eurotankers Inc.) |

|

| Vincent J. Solarino (The American Club) |

|

| Ilias Tsakiris (American Hellenic Hull Insurance Co.) |

|

| Spilios H. Fasois (Faros Marine Services S.A.), Ilias Tsakiris (American Hellenic Hull Insurance Co.), George Alexandratos (Apollonia Lines S.A.), Lilian Evgenidis (Teekay Shipping (UK) Ltd.), Angeliki Rigos (John J. Rigos Marine Enterprises), Panayiotis J. Christodoulatos (Ikaros Shipping and Brokerage Co., Ltd.) |

|

| Markos K. Marinakis (Marinakis Chartering Inc.), Lambros Varnavides (Baltic Exchange), Dorothea G. Ioannou, Joseph E.M. Hughes (The American Club) |

|

| Tom Hamilton and Sebastian Tjornelund (The American Club), Mike North (Seascope Insurance Services Ltd.) |

|

| Tom Kite (Kite Warren & Wilson Ltd.-Integro), Lewis Cadji (Union Maritime), Martin Cook (Kite Warren & Wilson Ltd.-Integro), Gustavo Gomez, Brian Davies, Joseph E.M. Hughes, Niki Tiga (The American Club) |

|

| The American Club’s London team with the Managers of SCB Inc |

|

| Joseph E.M. Hughes (The American Club) |

|

| Dorothea G. Ioannou (The American Club) |

|

| Petros Mandarakas (National Insurance Brokers S.A.), Philippos A. Piperas (Ness Marine Brokers (Hellas) Ltd.), George M. Vourlides (Minimar Insurance Brokers), Antonis Bavas (The American Club) |

|

| George D. Gourdomichalis (Phoenix Shipping & Trading S.A.), Joseph E.M. Hughes, Dorothea G. Ioannou, Vincent J. Solarino (The American Club), Panayiotis J. Christodoulatos (Ikaros Shipping and Brokerage Co., Ltd.) |

|

| Marina Papaioannou (DNV-GL), Theano Kalapotharakou (ELNAVI), Elpi Petraki (ENEA Shipmanagement), Elina Kassotaki (Holland Hellenic Shipping Agencies), Angeliki Karagianni (Navia Hellas), Maria Mavroudi (The American Club), Ioanna Topaloglou (Orion International Brokers & Consultants Ltd.) |

Capital Ship Management Corp. takes delivery of M/T ‘Aristaios’

|

About Capital Ship Management Corp.

Capital Ship Management Corp. is a distinguished oceangoing vessel operator, offering comprehensive services in every aspect of ship management, currently operating a fleet of 55 vessels with a total dwt of 5.70 million tons approx. The fleet under management includes the vessels of Nasdaq-listed Capital Product Partners L.P.

Japanese yards overtake Korean rivals

According to Clarkson Research data released yesterday, the shipbuilding orderbook held by Korean shipyards stood at 19.92m cgt (473 units) as of the end of December 2016, while Japanese shipyards had an orderbook of 20.96m cgt (835). China remains out on top.

During their heyday in 2008, Korean shipbuilders had an order backlog 30m cgt bigger than their Japanese counterparts. This is also the first time since 2003 that Korea’s order backlog has fallen below 20m cgt.

splash247.com

Brazilian Iron Ore and Grain Exports in 2016

By contrast, Brazil’s corn and soya (beans & meal) shipments both fell in 2016 with 21.9 Mt and 66.0 Mt exported, down by 7.4 Mt and 3.1 Mt on 2015, respectively.

Comparison Of Hong Kong And London Arbitration

The purpose of this article to discuss the major procedural differences between arbitrations in London and Hong Kong.

It may be helpful to explain at the outset that the procedural law of the seat of the arbitration will apply unless the parties agree otherwise. The substantive law or the law governing the dispute, may be the same as the procedural law or the parties may have agreed that a different law will apply to the dispute.

Where the seat of arbitration is London, the procedure will be governed by the Arbitration Act 1966 of England and Wales. Where the seat of arbitration is Hong Kong, the procedure will be governed by the Arbitration Ordinance, Cap 609.

Appointment of arbitrators

If the charterparty contains a detailed arbitration clause along the lines of the BIMCO/ LMAA Arbitration Clause, the parties are each to appoint one arbitrator. If the respondent fails to appoint its arbitrator within the 14 day time limit the party who commenced arbitration may appoint its chosen arbitrator as the sole arbitrator. However, in many cases those fixing the charterparty are operators and they may not recognise the significance of having a properly drafted arbitration clause. It is not uncommon for fixture notes to simply provide for “London arbitration, with English law to apply” or “Hong Kong arbitration, with English law to apply”, without stating the number of arbitrators or the mechanism of appointment. We will now look at what the legal position is under English law and Hong Kong law respectively if a party wishes to commence arbitration under an arbitration agreement which does not specify the number of arbitrators and/or how they are appointed.

Where the number of arbitrators is not specified

In a London arbitration, if there is no agreement as to the number of arbitrators, the tribunal will consist of a sole arbitrator pursuant to section 15(3) of the Arbitration Act 1996. There is no equivalent provision in the Arbitration Ordinance. In a Hong Kong arbitration, if the charterparty does not specify the number of arbitrators, the matter is referred to the Hong Kong International Arbitration Centre (“HKIAC”) pursuant to section 23(3) of the Arbitration Ordinance who will determine whether the matter should be referred to one or three arbitrators. The HKIAC will charge a fee for making a decision on the number of arbitrators, currently HKD8,000, which is a little more than USD1,000.

Where the parties fail to agree on whom to appoint as sole arbitrator

Assuming that the number of arbitrators is to be one (whether because of the parties’ agreement or the operation of law referred to in the preceding paragraph), what will happen if the parties are unable to agree who should be appointed as the sole arbitrator, or if one party simply fails to respond to the other’s proposed candidates? Again the position under English law and Hong Kong law is different.

Pursuant to section 15(3) of Arbitration Act where the charterparty does not specify the number of arbitrators, in a London arbitration the Tribunal will consist of a sole arbitrator. However, the claimant may face considerable difficulty if the opponent refuses or fails to agree on the candidate. This is because, an application will need to be made to the English court for the appointment of an arbitrator which will then need to be served on the opponent who may be resident outside the jurisdiction. The requirements for service of documents are far more stringent in court proceedings than in arbitration: service cannot be effected by email, fax or post as in arbitration proceedings; instead the claimant must obtain the leave (permission) of the court to serve the proceedings out of the jurisdiction. Service within the EU will be relatively straightforward, but if service is to be effected in a country which does not use English as its official language (so that translation of all relevant documents may become necessary) and/or which has a complicated service procedure (e.g. where court documents must be served through the local courts), the process may well take months and be costly.

By contrast in Hong Kong, whether the opponents are domiciled in Hong Kong or overseas, the claimant may simply apply to the HKIAC for the appointment of the sole arbitrator, albeit at a fee of HKD8,000. The HKIAC will either appoint the claimant’s chosen arbitrator or one of its own choice.

In light of the above, it is a good practice to have a proper arbitration clause so as to avoid the complexities and costs which may arise constituting the Tribunal.

Discrepancy between fixture recap and proforma charter

Gencon 94 is a popular form of voyage charter for bulk cargoes where the parties want to use a relatively simple form of charterparty. Paragraph 19 of Gencon 94 is the law and arbitration clause. It sets out the options of (a) London arbitration English law, (b) New York arbitration and US law, and (c) arbitration at the place specified in Box 25 in Part 1. It goes on to say at sub-paragraph (d) that if box 25, Part 1 is blank, clause 19 (a), which provides for London arbitration, will apply. If the parties do not make any choice of the forum, sub-clause (a) will kick in by default.

The position becomes more complicated however where the parties say in the recap, but not in Box 25, that arbitration is to take place in, say, Hong Kong. One construction is that in such a case the appointment procedure in clause 19(a) will apply by default except that the arbitration will be governed by Hong Kong law. Alternatively, the arbitration clause in the recap and clause 19(a), when read together, provide for Hong Kong to be the geographical location for the hearing subject to the English Arbitration Act. This was the argument raised by Daewoo in the case of Shagang South-Asia (Hong Kong) Trading Co Ltd -v- Daewoo Logistics [2015] 1 Lloyd’s Rep. 504. In this case Shagang applied to the English court to set aside the arbitration award on the ground that the sole arbitrator appointed by Daewoo had no jurisdiction. The court agreed with Shagang that where the recap provides for Hong Kong arbitration, the arbitration clause in the recap will override clause 19 of Gencon, so that Hong Kong law will apply as the procedure law of the arbitration. On the facts the arbitrator had not been properly appointed.

Therefore, if the parties wish to adopt Hong Kong law and arbitration, the proper way to do this is to either put “Hong Kong” in Box 25, Part 1 of Gencon 94, or (if Gencon 94 is incorporated by reference only) copy the entire clause 19(a) into the recap but change the forum from “London” to “Hong Kong” and the legislation from “Arbitration Act 1996” to “Arbitration Ordinance, Cap 609”. Alternatively, if the parties want the arbitration to be governed by English procedural law but the hearing to take place in Hong Kong, they should make this very clear in the arbitration clause.

Arbitration Rules

We will briefly discuss the procedural law applicable to the arbitration.

(a) England

The parties may provide for the arbitration procedure in the charterparty. It is common to see time charters specifying that arbitration is to be subject to the LMAA Terms and that if the disputed amount does not exceed a specified sum, the dispute is to be referred to LMAA Small Claims Procedure. Also, if the charterparty does not say which procedure is applicable, the arbitration will be subject to LMAA Terms if the arbitrators accept appointment under the LMAA Terms.

(b) Hong Kong

As for Hong Kong arbitration, there are a number of procedural rules to choose from; the HKIAC Administered Arbitration Rules; the HKIAC Procedures for the Administration of Arbitration under the UNCITRAL Arbitration Rules and the UNCITRAL Arbitration Rules for ad hoc arbitration. If no arbitration rules are agreed, the procedure sets out in the Arbitration Ordinance will apply by default. If the disputed amount is not large, the parties may consider referring the dispute to HKIAC Small Claims and Documents Only Procedure so as to ensure a simplified arbitration and hence save costs.

Appeal

A very important difference between London and Hong Kong arbitrations is in relation to the right to appeal.

Pursuant to section 67 and 68 of the Arbitration Act, a party may challenge the arbitration award on the ground of the tribunal’s lack of substantive jurisdiction or serious irregularity affecting the tribunal, the proceedings or the award. Further section 69 provides for an appeal against an award on a question of law.

In contrast, there are very limited circumstances in which a party to a Hong Kong arbitration may challenge or appeal the tribunal’s award.

Section 81 of the Arbitration Ordinance adopts Article 34 of UNCITRAL Model Law on “Application for setting aside as exclusive recourse against arbitral award”. In essence, the grounds for an application to set aside an award are primarily procedural irregularities, e.g. if the applicant was not given proper notice of the appointment of the arbitrator or the proceedings, or if the award deals with a dispute which falls outside the scope of the submission to arbitration etc.. Significantly, unlike London arbitration, a party has no right to appeal against the award on the ground that the tribunal has erred in law in a Hong Kong arbitration. Some may find this disagreeable, and any party who would like to preserve the right to appeal to the court should bear this in mind when he negotiates the arbitration clause. However, the finality of the award is also an attractive feature of Hong Kong arbitration, giving the parties certainty that the award is final and irrevocable.

Source: Skuld

Too many ships, the issue for chem shipping

Most forecasts put the problem of too many ships as the central issue for that sector, not only in the coming year but in the next few after that.

Too many ships chasing too few cargoes has plagued chemical shipping off and on for years, and this dilemma is expected to continue.

The Chemical Forecaster, published by global shipping consultancy Drewry, said recently that rising fleet growth and softening seaborne trade will depress chemical shipping freight rates over the next few years.

The problem surfaced quite visibly in 2016.

Freight rates on the two major chemical shipping routes in the Americas – the transatlantic eastbound and the US Gulf to Asia trade lane – declined by 9\% during the year. New fixtures reported in the ICIS shipping report declined by the same percentage or maybe more, based on totals through November.

Chemical shipping giant Stolt-Nielsen noted the too-many-ships problem in its third-quarter earnings report. CEO Niels G Stolt-Nielsen said a weaker clean petroleum products (CPP) market had pushed ships that would have otherwise been absorbed by a healthy CPP sector into the chemical tanker market. The result: reduced volumes and declining freight rates.

“It is difficult to forecast what the year ahead may bring,” Stolt-Nielsen said. “Volume growth has not kept pace with supply-side growth, a situation made more acute by the recent influx of CPP swing tonnage. On the demand side, the weak return volumes from China and other Asia ports are likely to continue.

The Drewry report noted a reduction in China’s imports of certain products during 2016, not only because of declining demand but also from a surge in domestic production.With new projects there slated to begin operations in the next few years, demand for some chemical imports will decline further, the report said.

In the long term, this will push down on freight rates to Asia.

“While freight rates on some routes are forecast to reduce substantially, other routes may see rollovers or minor increases,” said Hu Qing, Drewry’s lead analyst for chemical shipping, in the report.

Qing said shipowners’ earnings will remain depressed for the next two years, especially those covered mainly by contract business.

Additionally, Qing said time-charter rates in the smaller size categories should remain stable in the next two years, but rates for the larger-sized chemical tankers are expected to decline steeply “because of surplus supply and intense competition”.

Source: ICIS (By Lane Kelley)

Euronav in $186m VLCC quartet sale and leaseback deal

The four VLCCs are the Nautilus (2006), Navarin (2007), Neptun (2007) and Nucleus (2007). The transaction assumes a net en-bloc purchase price of USD 186 million.

The transaction produced a capital gain of about USD 37 million and the transaction should be booked as an operating lease under IFRS. As per Euronav dividend policy, this capital gain will not be eligible for dividend distribution. After repayment of the existing debt, the transaction generated in excess of USD 100 million free cash. The vessels were delivered to their new owners, the investment vehicles advised by Wafra Capital Partners Inc. on 22 December 2016.

Euronav has leased back the four vessels, which were built by Dalian Shipbuilding Industry Co., Ltd. (DSIC), under a five year bareboat contract1 at an average rate of USD 22,000 per day per vessel and at the expiry of each contract the vessels will be redelivered to their new owners.

Pareto Securities advised Euronav on this transaction.

Hugo De Stoop CFO, said: “Euronav is very pleased to have executed this transaction in what have been challenging conditions for asset values in shipping markets. This transaction has the advantage of increasing our liquidity position for 2017 whilst maintaining our exposure to a market that, we believe, will be interesting over the next five years.”

Wafra Capital Partners Inc., a U.S. registered investment adviser that is indirectly beneficially majority owned by an autonomous agency of the government of Kuwait, provides investment advisory services to its clients and principally focuses on structuring and advising investment vehicles on a Shari’ah-compliant basis in the asset-based and structured finance arenas.

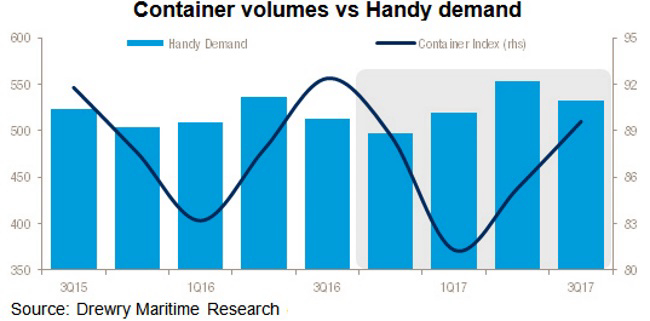

Multipurpose shipping freight rates to improve by end 2017

Dry cargo demand is weak but strengthening with multipurpose shipping market share expected to grow at just under 2\% per year to 2020. Demolition levels are up in both the multipurpose and competing sectors, whilst newbuilding ordering has waned, which will result in minimal aggregate multipurpose fleet growth to 2020.

|

The future market prospects for the multipurpose shipping sector are not only dependent on the supply-demand balance for that segment, but also on the other vessels that compete for breakbulk and project cargo, in particular Handy bulk carriers and container vessels.

“Slow growth in supply, alongside better growth in demand, is expected to help multipurpose charter rates in 2017 and beyond, supported by a recovery in the dry bulk market, albeit a slow one. In particular, the oversupply situation, which has dogged this sector for many years, is expected to level out in the medium term,” comments Susan Oatway, lead analyst for multipurpose shipping at Drewry.

The new International Maritime Organisation (IMO) regulation on Ballast Water Management is likely to have a small effect on demolition levels in the multipurpose sector, and even more so for the bulk carrier sector. At the same time any investment in this sector will be in project carriers (with a lift of 100 tonnes or more) producing fleet growth in this segment of almost 3\% pa to 2020, whilst the general cargo segment will contract at around 2\% pa over the same period, leading to overall MPV fleet growth of less than 1\% pa to 2020.

“On the face of it, the supply-demand balance is levelling out, demand is growing faster than supply and the market is improving. As ever, it is the competition for cargoes from bulk carriers and containerships that will keep rates in this section of the market subdued for at least another 12 months. Until rate increases are sustained in the bulk carrier and container ship sectors, there will be little reprieve in their drive to obtain further market share,” added Oatway.

Source: Drewry

THE SHIPPING MARKET IN 2016 AND LOOKING FORWARD

The longer global economic growth remains weak and lacks investment, the lower future growth potential for shipping.

For eight years, the world has struggled to cope with huge changes and challenges brought around by the crash of the financial market in 2008. The resulting issues have not always been dealt with in the best way, leaving many large economies still in ‘recovery’ mode.

The full restoration of shipping markets will need several years of solid improvements to lift fleet utilisation rates. Sector overcapacity almost everywhere must be reduced. Government support for any industry – including shipping – which is feeling the heat of global competition might seem like a good thing. But direct subsidies from governments in fact have a negative impact on the global shipping industry as they affect free trade and undermine the level playing field for businesses.

In pure economic terms, 2016 has seen Europe improving, the US stagnating and Japan at a standstill. So, we have not seen much global change aside from some interregional trade flows and there has been no real growth of demand on a broader scale.

In shipping, we rely on global imbalances in raw materials, energy and manufacturing facilities. Regardless of reported statistics of economic growth being right or wrong, China remained at the centre of shipping imports and exports in 2016.

Will the world grow its GDP in 2017 in a way that will benefit shipping? Probably not, as global GDP growth is currently driven by service sectors and developing/emerging economies which result in a lower “GDP-to-trade multiplier”, and thus generate a lower level of shipping demand than we have been accustomed to in the past.

Dry bulk: worst year on record - heavy demolition activity needed to relieve the pain

2016 has been a horrible year for the dry bulk shipping industry. After the Baltic Dry Index (BDI) reached an all-time-low of 290 on 10 February, it improved steadily throughout the year to peak in mid-November at 1,261. This was driven by and benefitted mainly the capesize ships as they transported the key commodities of iron ore into China. As the year progressed, the situation eased as demand growth outstripped the impact of the net supply growth of the fleet.

Chinese steel mills grew production and kept on substituting domestically mined ore with imported ore. Additionally, the reduction in operational days at Chinese coal mines reversed the declining trend for coal imports, adding much needed tonne-miles to the demand side.

In May, BIMCO provided industry leadership with some new and unique market analysis on the “Road to Recovery” for dry bulk. This analysis identified what the shipowners must do to return to profitability in 2019. Scrapping ships and refraining from building new ships is essential as we can’t expect the same levels of demand growth as we have experienced in the past.

For 2017, it is vitally important that shipowners handle the supply side of the market with great care. A continuance of the alarmingly low level of demolition activity in the second half of 2016 simply will not deliver the needed zero fleet growth. A significant number of new ships are on order for 2017 and 2018. The only way to neutralise the impact of this influx of new ships will be to scrap 30 million DWT annually. This is not a tall order in theory, but the slowdown in scrapping seen since June 2016 causes alarm bells to ring. BIMCO expects the supply-side to grow by around 1.6\% in 2017 (2.2\% in 2016E).

Tanker: reversal of fortune after a perfect year

In the wake of a very strong 2015, fortune faded as expected for crude oil and oil product tankers. A strong freight market was created by an increased throughput at global refineries causing up-front oil demand to run ahead of end-consumption and a moderate supply side growth for crude oil tankers.

In 2016 the fleet grew by 6\% for both tanker segments. This unbalanced the market because demand growth eased off. BIMCO suggests that in coming years the end-consumption of oil will need to catch up – and bloated oil stocks must be drawn on – before the market can be rebalanced.

Global oil supply continued to grow in 2016 despite many disruptions to production in key exporting countries. The re-entry of Iran into international oil stood as the single-most disruptive event to an established oil market and it had a knock-on effect into the tanker market. Whether the changes to trade patterns end up benefitting the tanker market remains to be seen and depends on the West African exporters’ ability to defend their market shares in Asia, particularly in India.

Tanker demand growth in 2017 is expected to come predominantly from the greater Asian region led by China and India.

BIMCO expects the crude oil tanker segment to see a net fleet growth of around 3\% in 2017 (6.0\% in 2016E). We estimate the supply side growth rate of the oil product tanker fleet to be around 2.5\% (6.1\% in 2016E). We foresee demolition of tanker capacity to reach a five-year high, but not enough to prevent the onset of a loss-making freight market.

Showing leadership to the global shipping industry, in 2017 BIMCO will continue its unique series of analysis on the “Road to Recovery” for the crude oil tanker market, following the analysis published in 2016 on what is needed for the dry bulk sector to recover.

Container: fundamental market balance improved as demolition went through the roof

After deteriorating market conditions in 2015, with a very high fleet growth and a sensationally high number of new orders for future delivery, 2016 got off to a bad start. The need to match the supply of container shipping capacity with global demand for containerised goods became even more urgent.

How did the container shipping industry act in this “self-inflicted” shipping market crisis? By using some tools that had seemingly been forgotten. Many operational tools have been successfully applied in the market already (slow-steaming and idling), leaving the non-operational tools to be put into action in 2016 (limiting new orders, scrapping and consolidation).

2016 stands out in terms of consolidation, both in the form of outright mergers but also in the newer and larger alliances being forged to cut cost. We also saw the unprecedented event of a government-sponsored shipowner filing for court protection.

Additionally, the very low number of newbuilding orders was backed up by an all-time high of demolition capacity reducing the harmful effects of new ships being delivered. Panamax ships went out of fashion, resulting in further value erosion of the ship size that turned out to be the one which was squeezed out between the feeders and the very large ships.

Generally, the container shipping industry has found it difficult to adapt to the new normal where demand grows by a multiple of global GDP growth of one or even below, unlike the multiplier of two or more experienced year on year in the past. Nevertheless, market conditions ended up improving in 2016 as fleet growth was lower than demand growth, the first time since 2010.

BIMCO expects the container shipping segment to see a net fleet growth of around 3.1\% in 2017 (1.1\% in 2016E). If the multiplier gets back to one, and the IMF forecast of 3.4\% becomes reality, the market will neither improve or worsen in 2017.

By Peter Sand in Copenhagen, DK

BIMCO

Atlantis Acquires Tanker Duo

The Ionian Trader and Lydian Trader. Both are sister-ships in the size of 5500 dwt, with Marine-Line tank-coatings and built in 2008.

The vessels were built by Turkish KGS, a joint venture (JV) between Ares Tankers and Galatasaray Holding at Celik Tekne Shipyard with the intention of selling all six of the sister-ships to another 50-50 JV between Mowinckels and Ares. After delivering the first four vessels: Lycian, Ionian, Lydian and Hada, Mowinckels’ appetite for the remaining two became obsolete due to the Lehmann-crisis. Thus the fifth and sixth ship remained with KGS and are managed by Ares Tankers Management as RC Behar and Hitra.

The four joint venture ships were financed by a consortium of Nordea and Deutsche Bank. The JV ran into financial problems which brought the Norwegian/Turkish partnership to separate, leaving the ships with Mowinckels Rederi. The lenders sought new buyers and sold all four vessels in 2012. The first chem-tank duo was sold to Borealis Maritime, the ships were renamed Bomar Pluto and Bomar Ceres. The other two, Lydian and Ionian were sold to Restis’ company: Enterprises Shipping & Trading.

Bomar Pluto and Bomar Ceres were under the technical management of Armona Denizcilik (the management arm of Atlantis Tankers) for 3 years. The ship and shore staff are very familiar with the vessels and know the quality of the design. The tankers meet the high quality standards of Atlantis Tankers.

Currently the Ionian and Lydian Trader are on T/C to Uni-Chartering. The handover of the vessels is expected to take place in the next 45 days to one safe berth in the ARA; free of cargo and free of slops. The duo will be taken under the technical & crewing management of Armona Denizcilik, and will be commercially managed by Atlantis Tankers.

The Ionian Trader will be renamed: Atlantis Arki, and the Lydian Trader will be renamed: Atlantis Araceli.

Lastly, the two new-buildings: Atlantis Augusta and Atlantis Alicante will be delivered by early 2017. Consequently, the German-owned company will experience a fleet-growth of 50\%. The fleet is not only expanding, it is also becoming younger, as the average fleet age will fall from 10.25 to 8.33 years by next year.

![]()

Powered by ![]() © Μaritimes 2019

© Μaritimes 2019