Euronav announces second quarter and half year results 2017

Freight rates challenging given seasonal patterns and concentration of deliveries of

newbuildings

FSO contracts extension provides further fixed income until 2022

Two additional seven-year Suezmax time charters signed during quarter adding to the

fixed income until 2025

Return to shareholders policy upgraded with a minimum fixed annual dividend of

USD 0.12 per share

Return to shareholders policy retains capability for additional dividend and share buy

back

USD 150 million unsecured bond raised diversifying and boosting balance sheet

strength

USD 110 million ECA (KSure) financing for the 2 VLCCs delivered in January

TEN Expands its Strategic Relationship by Chartering Two Additional Suezmaxes to a Major US Oil Concern

Two suezmax vessels have been chartered for three years, bringing the relationship to six vessels. These charters are scheduled to commence in early September upon completion of the current employment of each vessel and contain profit sharing arrangements.

"We are pleased that these new charters not only solidify the Company's cash generating ability and visibility, but also emphasize the fleet's competitive advantage when seeking to secure charters with high quality oil concerns," stated Mr. George Saroglou, Chief Operating Officer of TEN. "With more than 75\% of the fleet in secured employment, resulting to $1.5 billion already in minimum secured revenues and the possibility of generating considerable additional income through profit sharing, we are very confident that TEN will be one of the prime beneficiaries going forward once we enter the seasonally stronger fourth quarter and beyond," Mr. Saroglou concluded.

ABOUT TSAKOS ENERGY NAVIGATION TEN, founded in 1993, is one of the first and most established public shipping companies in the world today. TEN’s pro-forma fleet, including one Aframax tanker under construction, consists of 65 double-hull vessels, constituting a mix of crude tankers, product tankers and LNG carriers, totalling 7.2 million dwt. Of these, 45 vessels trade in crude, 15 in products, three are shuttle tankers and two are LNG carriers.

How long to get to your destination?

With the advent of cheaper air travel, the UK has seen a 68\% increase in the average number of holidays taken over the past 20 years, according to the UK Office for National Statistics. However, if you wanted t a holiday before 1950s, it could take up to 50 times as long to arrive at your desintation by boat.

VesselsValue has used it's Port Distance Calculator to work out how many nautical miles and hours it would take to arrive via a direct route from port to port.

|

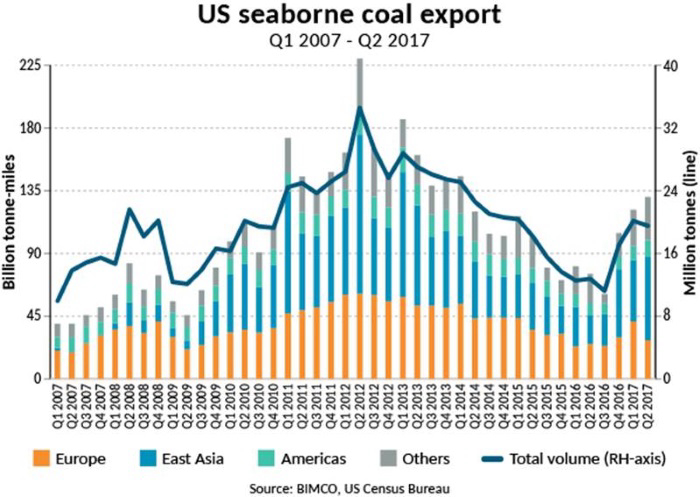

US coal export rebounds to support the improvement of the dry bulk shipping industry

The increase in total volume is predominantly driven by a growing demand from European importers. East Asian buyers have also ramped up their import of US coal, which is beneficial for the dry bulk shipping industry as it generates a substantial amount of tonne-miles, relative to other destinations.

BIMCO reported back in December 2016, that the tonne-miles from US coal exports halved over three years due to long-haul routes carrying coking coal to East Asia not operating to the same extent and diminishing demand from Europe. After reaching the lowest levels for exported coal in Q3 2016 since Q1 2007 in terms of total volumes, US coal exports now look to return to recognisable heights and become a dominant player in global seaborne coal transport once again.

BIMCO’s Chief Shipping Analyst Peter Sand comments:” A rising US coal trade has a multiplying effect on the dry bulk shipping industry, as it provides some of the longest sailing distances. East Asian importers source 61\% of their US coal from Norfolk, Virginia and Baltimore, Maryland and thereby accept a journey of up to 45 sailing days at an average speed of 13 knots (14,000 nautical miles)”.

|

US seaborne coal exports are up 57\% in total volume and 61\% in terms of tonne-miles for the first half year of 2017 compared to the same period last year. As the average sailing distance has grown more than total volume, it emphasises how the US has exported more to importers further away, primarily to East Asian destinations.

Europe imports the highest volume while East Asia generates the most tonne-miles

The main importers of US coal for the first half of 2017 are the Netherlands, South Korea and India, importing 32\% of all US seaborne coal export. The most influential importers for the dry bulk shipping industry are South Korea, India and Japan, generating 49\% of total tonne-miles.

|

Europe continues to be the largest importer of US coal and has for the first half year of 2017 imported 41\% of all US seaborne coal exports. Europe has sourced 4.8 million tonnes more coal from the US in the first six months of 2017 compared to the same period in 2016, which is an increase of 43\%. US coal exports to Europe occupies both the panamax and capesize segment.

The Netherlands have, in the last 10 years, been the main importer of US coal both in Europe and on a global scale. Due to its shorter distance to the US East Coast compared to East Asian buyers, it has in the past 10 years only generated the fifth highest number of tonne-miles.

East Asian importers are the main reason why tonne-miles are growing more than total volume, despite only 24\% of total US seaborne coal exports were destined for East Asia in 2017. The East Asian imports of US coal surged 172\% in the first six months of 2017 compared to 2016, amounting to an increase of 5.9 million tonnes. US coal shipments to East Asia generated 112\% more tonne-miles in the half year of 2017 compared to the same period in 2016. South Korea is the most influential importer in terms of tonne-miles over the last 10 years, but it is only the fifth biggest importer on a global scale measured in volumes imported.

The Americas imported an additional 22\% of US seaborne coal during the first six months of 2017 compared to the same period in 2016. This surge in total volume generated an additional 23\% tonne-miles. The Americas have so far for 2017, imported 17\% of all US coal exported via sea, but due to the geographical proximity to US ports, the Americas only generated 9\% of the total tonne-miles.

Higher US coal production but still close to lowest level since 1978

The US have produced 351 million tonnes of coal in the first half of 2017, this is an increase of 16\% compared to the same period last year, amounting to an increase of 49 million tonnes. This year–on–year increase does not indicate a high production level compared to years prior to 2016, as the amount of coal produced in 2016 was the lowest level since 1978.

US coal consumption numbers released so far only cover the first four months of 2017, but show an increase of 6\% compared to the same period in 2016. The production of US coal rose 16\% in the same period. This amounts to a surplus of 32 million tonnes of coal for the first four months.

Peter Sand adds: “If US coal exports remain high throughout 2017 it will have a solid effect on the global seaborne coal trade and support the overall improvement in the dry bulk shipping industry”.

Source: Peter Sand, Chief Shipping Analyst; BIMCO

Kassidokostas-Latsis Form New Dry Bulk Joint Venture Called Ivy Shipping LLC

Ivy Shipping has consummated its first deal, the acquisition of four Japanese built Supramax vessels, six years of age. The ships are expected to be delivered by the end of summer 2017 and will be managed by Marla Shipmanagement Ltd, a company owned by Mr. Paris Kassidokostas-Latsis. Ivy Shipping will be monitoring the developments of the dry bulk market, looking to expand the fleet opportunistically by the end of 2017.

Mr. Paris Kassidokostas-Latsis commented on this new investment: “In 2014, we set out to increase our LPG and tanker fleet. Three years later our goal has been successfully realized. Taking under consideration the current market conditions, we opted to expand our shipping business activities by collaborating with very important global strategic investors. I am highly optimistic about this joint venture and very confident of its future “.

Source: Ivy Shipping LLC

Greek shipowners buck declining newbuild ordering trend

This as it maybe, Greek shipowners have doubled their contracting in the first half, according to data from VesselsValue.

In all 245 vessels were ordered to end June, a slight decrease from 254 seen in the same period in 2016, and less than half of the 594 orders seen for first half 2015.

Greek-run companies placed orders for 58 new ship orders in the first half of the year, more than twice the number of orders made in the same period last year, and 24\% of all order placed, according to ship values specialist, VesselsValue.

VesselsValue data show that in January-June 2016 Greek shipowners ordered 28 vessels, a far cry from the 72 orders in the first half of 2015.

But, in July Greeks were reported to have inked orders for another 28 firm vessels and six options – 16 bulk carriers and 12 tankers firm. The dry ships range from capesize to kamsarmaxes (10) to handies, while the tankers comprise VLCCs, aframaxes and long and medium range units. Twelve different companies are seen to be behind the latest influx of new orders.

So, if the options are taken up, the new ship orderbook for Greek interests in the first seven months of 2017 will be 92 ships booked during a period when the international market was in decline.

Greek activity has restored Greek shipping on top of the shipbuilding orders, with China a distant second with 40 new ships ordered. There was a significant decline in demand from Japanese companies, to just 13 in the January-June 2017 period from 36 last year and 105 in the first half of 2015.

Data also point to Greeks sticking exclusively with the two main categories of ships: Greeks ordered 42 tankers and 16 dry-bulk carriers in the January / June period. Notably in the last three years the 151 Greek orders have included 104 tankers, given the crisis in the dry bulk sector.

David Glass

Greece Correspondent, Seatrade Maritime

Interlegal has opened its office in Varna, Bulgaria

Mladen has got more than 20 years practice experience in shipping and international trade business and many sound court cases in Bulgaria. “Our cooperation has started some years ago. Time confirmed together we are more efficient and are able to solve any legal task” – Mladen Popov says.

The Varna opening follows the recent expansion in Istanbul, Turkey and Batumi, Georgia. Interlegal’s purpose is becoming a legal one-stop-shop for shipping and trade business in the Black Sea.

DNV GL carries out its first offshore drone survey

|

| DNV GL has carried out its first offshore drone survey on board the tender support vessel Safe Scandinavia |

“Innovation is one of Prosafe’s core values. We are very pleased that we chose to try the drone survey, as it helped us optimize our survey requirements and allowed us to save significant amounts of time and money. Normally, this kind of operation would cause disruption to our client for several days. The drone survey took only a few hours and was just as effective,” says Ian Young, Chief Operating Officer at Prosafe.

“This was a great opportunity for us to demonstrate our drones’ abilities to check the condition of remote external components in challenging offshore conditions. The inspection only required the semi-submersible to de-ballast, then we flew the drone approximately 25 metres below the main deck to check the condition of the fairleads and their connections to the columns that hold up the TSV. With wind speeds of approximately 15 knots, this went very well and the survey showed that the fairleads and their connections were in a good condition,” explains Cezary Galinski, Project Manager Classification Poland at DNV GL.

The classification society has carried out multiple drone surveys on both ships and offshore units, inspecting many areas on board, ranging from tanks and cargo holds to external structures such as jack-up legs. The inspection of such spaces can be both costly and time consuming, and even in some instances potentially dangerous. Using drones to visually check the condition of remote structural components can significantly reduce survey times and staging costs, while at the same time improving surveyor safety.

DNV GL has built a network of trained drone pilots based in Gdynia, Piraeus, Singapore, Houston and Shanghai. This allows drone survey inspections to be offered from any of these hubs. At the same time, DNV GL is developing guidelines and updating our rule set to reflect the use of remote inspection techniques.

Video: https://www.youtube.com/watch?v=6eAaaRrwgZg&feature=youtu.be

About Prosafe

Prosafe is a leading owner and operator of semi-submersible accommodation vessels. Prosafe owns/operates eight semi-submersible accommodation, safety and support vessels and one tender support vessel (TSV) that is providing drilling support services on the NCS.

Prosafe's fleet consists of a combination of dynamically positioned and anchored vessels. Thereby, the fleet is versatile and able to operate in nearly all offshore environments. At present, Prosafe is the leader in the provision of offshore accommodation vessels in harsh and semi-harsh environments.

Prosafe has extensive experience from operating gangway connected to fixed installations, FPSOs, TLPs, semis and spars. The company’s track record comprises operations offshore Norway, UK, Mexico, USA, Brazil, Denmark, Tunisia, West Africa, North-west and South Australia, the Philippines and Russia.

About DNV GL

Driven by our purpose of safeguarding life, property and the environment, DNV GL enables organizations to advance the safety and sustainability of their business. We provide classification, technical assurance, software and independent expert advisory services to the maritime, oil & gas and energy industries. We also provide certification services to customers across a wide range of industries. Operating in more than 100 countries, our professionals are dedicated to helping our customers make the world safer, smarter and greener.

About DNV GL – Maritime

DNV GL is the world’s leading classification society and a recognized advisor for the maritime industry. We enhance safety, quality, energy efficiency and environmental performance of the global shipping industry – across all vessel types and offshore structures. We invest heavily in research and development to find solutions, together with the industry, that address strategic, operational or regulatory challenges. For more information visit www.dnvgl.com/maritime

Eagle Ocean Marine enjoys another successful year amid American Club’s centennial celebrations

|

EOM offers attentive, competitively-priced Protection and Indemnity and Freight, Demurrage and Defense insurance to the operators of smaller vessels, typically those in local and regional trades, who prefer a fixed premium approach to their P & I needs.

It provides the benefits of American Club primary cover and service capabilities, co-venturing the first layer of insurance protection with underwriters at Lloyd’s on a quota-share basis. Lloyd’s syndicates also participate in the facility’s excess reinsurance arrangements for limits up to $500 million per risk. In this way, Eagle Ocean Marine offers the unsurpassed levels of service associated with an International Group club, underpinned by the impeccable security of reinsurance at Lloyd’s.

EOM insures ships from all over the world except the United States. It enjoys a strong presence in Asia, approximately 48\% of its business currently being derived from Southeast Asia and 32\% from Greater China. However, its share of the market in Europe, the Middle East and Africa has also grown over the past year and now accounts for about 15\% of its total portfolio.

EOM’s revenue has similarly increased over recent years. The recently concluded insurance year featured a topline increase in revenue of approximately 16\% over the previous twelve months. Total income exceeded $8 million for the first time. It is expected that steady revenue growth will be maintained over the year ahead.

At the operating level, the last several years have enjoyed consistently good results. The incidence and severity of claims have remained at moderate levels, reflecting a prudent policy of risk selection and premium pricing. Since it commenced operations in 2011, EOM has generated an aggregate profit margin in excess of 30\%. This, together with confidence in EOM’s prospects generally, informed the recent favorable renewal of its reinsurances.

|

| Joe Hughes, Chairman and CEO of Eagle Ocean Agencies, Inc. |

“We take the long view when it comes to developing market share, and will continue to ensure that the EOM product is characterized by careful risk selection, sensible pricing, effective loss prevention and unsurpassed claims service. Inspired by the traditions of classic P & I mutuality, EOM occupies a special place in the fixed premium sector for those who desire a high-quality approach to their insurance needs. We are confident that EOM’s business model will enjoy increasing success over the years ahead.”

Eagle Ocean Agencies, Inc., is a member of the New York-based Eagle Ocean Group of companies – North America’s leading provider of mutual management, underwriting, adjusting, claims handling, surveying and loss consultancy services to the international shipping and insurance communities. Eagle Ocean Agencies, Inc.’s core business is the provision of coverholder and related services to a variety of insurance carriers.

American Steamship Owners Mutual Protection and Indemnity Association, Inc. (the American Club) was established in New York in 1917. It is the only mutual Protection and Indemnity Club domiciled in the entire Americas and its headquarters are in New York, USA.![]()

The American Club has been successful in recent years in building on its US heritage to create a truly international insurer with a global reach second-to-none in the industry. Day to day management of the American Club is provided by Shipowners Claims Bureau, Inc. also headquartered in New York.

The Club is able to provide local service for its members across all time zones, communicating in eleven languages, and has subsidiary offices located in London, Piraeus, Hong Kong, Shanghai, and Dalian, plus a worldwide network of correspondents.

The Club is a member of the International Group of P&I Clubs, a collective of thirteen mutuals which together provide Protection and Indemnity insurance for some 90\% of all world shipping.

http://www.american-club.com/

Dry Bulk FFA: Capesize Market Slips

A firm start on paper was justified when the 5TC index jumped 10\%. Despite the justification for the paper premium finally arriving, momentum on paper failed to carry through and rates slipped a touch over a quiet afternoon session. The end result was a curve that looked remarkably unchanged over the day.

Panamax FFA Commentary:

We continued to trade in the top end of the weeks range through most of the day with good volume changing hands at the highs with Aug and Q4 pushing up to $9700 and $10250 respectively, while further out we saw Cal18 and 19 printing $9200. Despite drifting off a touch on the back of some profit taking the tone remains relatively positive.

Supramax FFA Commentary:

Supramax paper was subject to an early initial push with Aug trading $9300 and Q1 7850. However with limited activity we sat at these rates for most the day with little change. Index was slightly disappointing -$77 10TC and -$108 derived 6 TC. The afternoon drifted to a close as we still saw bid support but little appetite to trade. Have a good evening.

Handysize FFA Commentary:

A pretty much unchanged day for the handysize paper, as we lacked interest frim start to finish. No reported trades. Have a good evening.

![]()

Powered by ![]() © Μaritimes 2019

© Μaritimes 2019