-

Home

-

Maritimes NEWS

-

Ports

- maritimes

maritimes

Monthly Newbuilding Market Report

Golden Destiny : Monthly Newbuilding Market ReportMonthly Newbuilding Market ReportIssue: April 2020

Attached please find our:

- Monthly Newbuilding Market Report ( Ordering activity per vessel type for greek and foreign shipping players / Newbuilding Trends)

Weekly Market Report

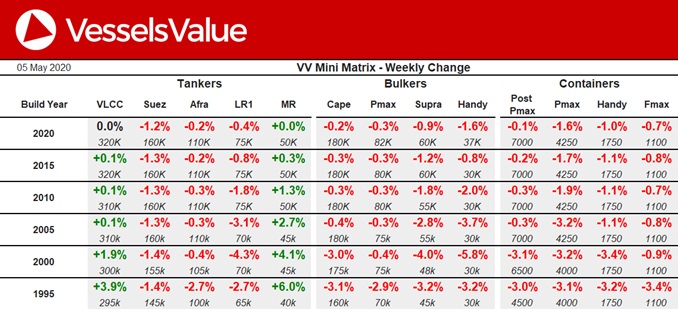

Weekly Vessel Valuations Report, May 05 2020

Tanker:Older VLCC and MR values have firmed.

Aframax Pallas Orust (114,800 DWT, Jan 2004, Samsung) sold for USD 14.00 mil, VV value USD 14.39 mil.

MR2 Glenda Meredith (46,100 DWT, Feb 2010, Hyundai Mipo) sold for USD 19.00 mil, VV value USD 18.03 mil – SS/DD Passed.

Bulker: Bulker values have softened.

Capesize China Steel Excellence (175,800 DWT, Feb 2002, CSBC Kaohsiung) sold to Taiwanese buyers for USD 8.00 mil, VV value USD 6.87 mil – DD Due.

Panamax Paganini (75,100 DWT, May 2008, Hudong Zhonghua) sold to Modion Maritime for USD 8.10 mil, VV value USD 8.65 mil.

Container: Panamax values have softened.

No sales have been reported.

Setting sail for 2050: Imagining the future of marine lubrication

hese are turbulent times for our industry. Ship owners have been thrust from the relative comfort of gradual change to seismic shifts and mounting complexity – a process set in motion by the International Maritime Organization’s (IMO) 2020 sulphur cap on marine fuels. This pace is set to accelerate as the various hurdles of greenhouse gas (GHG) emissions reductions looms towards 2050 targets.

Driven by regulatory and commercial pressure, the progression towards more efficient engines and lower sulphur fuels will require increasingly sophisticated technology from bow to stern. This is especially true in the area of cylinder lubrication, where higher levels of performance will be instrumental in meeting evolving engine needs. It’s a situation ExxonMobil is prepared for – we have been here before as an industry. In a process which began 20 years ago in on-highway transportation, engine lubrication proved a critical enabler for leaps forward in engine design, fuel quality and emissions performance. Importantly, our experience proves that operators can never be too prepared.

The 2050 deadline may seem far away, but vessels being designed and commissioned today may still be on the water in 30 years, rendering the timescale rather more immediate. In this white paper, we will explore what the changes we expect over the coming decades mean for marine lubrication, and how this knowledge can help operators build resilience into their businesses ahead of IMO 2050.

Rising to the challenge of more severe operating conditions

Next generation marine engines will require next generation oils

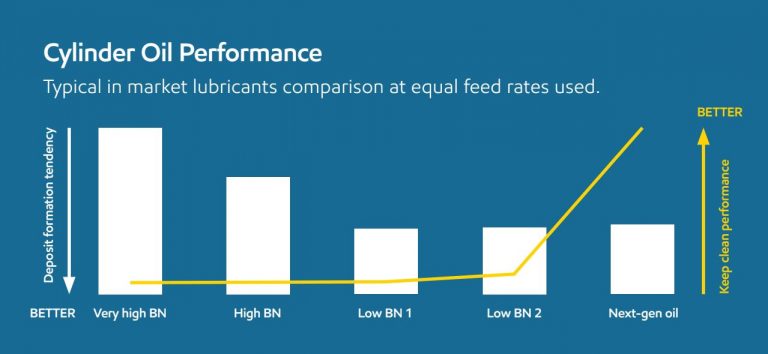

Meeting the IMO’s 2050 GHG reduction targets requires engine builders and ship designers to deliver significant efficiency improvements. To achieve this, many operational fundamentals are changing. Next generation engines will operate at higher pressures and combustion temperatures, creating a far more severe environment for lubricating oils. Put simply, as OEMs continue to push the boundaries of engine design, there is a pressing need for cylinder lubricants to ‘do more’.

Otherwise, inadequate lubrication performance can cause insufficient engine cleanliness and protection, resulting in lubricant related deposits and engine damage, higher maintenance costs and increased engine downtime. Given the competitive nature of the shipping market, this is a risk operators can ill afford. Like developments seen in on-highway lubrication, the solution will come in the form of more advanced, higher quality oil formulations.

Cylinder lubricants of the future can, therefore, be expected to offer improved high-temperature viscosity, greater thermal stability and better detergency. Product lifecycles are also likely to shorten significantly, favouring suppliers who can invest heavily in R&D to keep pace with engine builders’ performance requirements.

Source: ExxonMobil

Adjusting to a multi-fuel reality

Following the IMO 2020 sulphur cap, and in preparation for 2050 emissions targets, vessels’ inventories will increasingly comprise a variety of fuels, including alternative fuels. Operators also need to prepare for more fuel switching as legislation evolves, further impacting the engine and cylinder oil requirements. Given the unpredictability ahead, ship owners will need engine designs that offer maximum fuel flexibility. They will also need strategies to cope with increasing complexity, placing growing emphasis on strong relationships with fuel and lubricants suppliers, as well as on lubrication solutions that meet their changing needs. Again, we can expect shorter product lifespans and a growing need for formulations to be flexible – both to changing fuel specifications and quality. Critically, cylinder oils of the future will need to control deposit levels more than ever before. Detergency and oxidation control will become increasingly important, and we may even see oils that are compatible with multiple fuel types.

Exploring real time engine oil optimization

Over the coming decades, we will also see growing on-board digitalization, accompanied by a proliferation in available performance data. Given the introduction of more complex engine and fuel technology, it will be critical to make full use of this potential. Scrape down oil analysis services such as Mobil ServSM Cylinder Condition Monitoring have already seen an increase in development due to its ability to deliver a range of critical preventative maintenance and operational benefits, from optimising cylinder oil feed rates to identifying issues with abnormal wear. Importantly, they can be tailored to the needs of each operation and supported with training to ensure maximum long-term gains.

Mobil ServSM Cylinder Condition Monitoring helps triple piston ring life

Orient Overseas Container Line (OOCL) was looking to safely extend piston ring life in a vessel’s engine, beyond the designer’s recommended 24,000 hours. ExxonMobil suggested implementing Mobil ServSM Cylinder Condition Monitoring as part of a Condition Based Overhaul (CBO) approach. An engine inspection after 53,000 hours revealed that components were free from deposits, and that wear on the piston rings was well within acceptable tolerances. This information enabled the vessel operator to extend the life of the piston rings to 72,000 hours, achieving significant savings and reducing downtime.

Preparing for tomorrow, today

As the industry charts its course towards 2050, ship owners face a journey punctuated by disruption. The increasingly severe operating conditions of next generation engines will change several important parameters. These, without optimum lubrication, risk causing significant maintenance issues – more frequent machinery replacements, increased downtime and escalating costs – with a direct impact on operators’ bottom lines. In short, it has never been more important to start planning for tomorrow, particularly if you are considering purchasing new build vessels now and running them for their full lifecycle – by which point the 2050 deadline will be upon us.

Looking to next generation lubricants for help weathering the storm

Lubrication will be a critical factor in helping newer, more efficient engines achieve optimum performance. Faced with an ever-expanding operational envelope, next generation cylinder oils will require a far greater investment in development and testing, and reformulations will become more common. In parallel, cutting-edge condition monitoring platforms will play a growing role in identifying potential issues and offering solutions to mitigate them.

Act now to stay one step ahead

Rising to the challenges outlined in this white paper will require new levels of sophistication and collaboration throughout the industry. Operators looking to safeguard the efficiency of their fleets tomorrow need to understand and prepare for the changes to come today. Lubricants manufacturers, meanwhile, should be well on their way.

Backed by over 60 years of heritage of our MobilGard™ marine lubricants, ExxonMobil is already addressing these challenges by working closely with leading engine builders and components manufacturers to keep ahead of the curve. Is your lubricant supplier doing the same? Find out what they are doing to ensure their offer supports the long-term resilience of your operation.

To find out more about ExxonMobil’s marine lubrication solutions, visit www.exxonmobil.com/en/marine.

Source: ExxonMobil

PM Mitsotakis urges bankers to help businesses with liquidity tools

Prime Minister Kyriakos Mitsotakis discussed how banks can infuse liquidity into the Greek economy following the coronavirus pandemic, at a Tuesday video conference with key ministers, the governor of the Bank of Greece and bank executives.

Mitsotakis noted that the survival of coronavirus-afflicted businesses is the government's primary concern, and that banks must ensure that liquidity tools provided by the government to them are channeled to Greek businesses, regardless of size.

They also discussed how the new European financial instruments can be best utilized to increase liquidity after the negative impact of the pandemic's first wave.

"We need to absorb the shocks as best we can and lay the groundwork for a dynamic restart," Mitsotakis underlined.

Responding to the Prime Minister's call for recovery, bankers estimated that approximately 16 billion euros of support funds can be directed into the Greek economy in the rest of 2020.

https://www.amna.gr/

DNV GL and Alpha Ori sign new MOU to spur digital transformation in shipping

Singapore, 4 May 2020: The maritime industry can benefit from digital technologies in a way that can have an immediate and transformative impact on design, operations, business models, and environmental impact. To harness this transformational power, the world’s leading classification society DNV GL and technology company Alpha Ori Technologies (AOT) have signed a Memorandum of Understanding (MoU) in which they agree to work together to contribute to the marine industry’s ongoing digital transformation. The MOU will also see the companies work together to unlock the benefits of new digital technologies and methods, including sharing data collaboratively, and the creation of frameworks and standards, to develop new and enhance existing products and services.

The MOU is based around the installation of Alpha Ori’s SMARTShip systems on BW LPG vessels, piloting the use of digital technologies to further enhance the relationship between ship operator and class. The following areas have already been identified as potential areas for exploration:

Data exchange for digital class services

Possibilities for continuous assurance

Remote operations and monitoring

“There is a tremendous opportunity for the shipping industry to improve the way it works,” says Andreas Sohmen-Pao, Chairman of BW Group and BW LPG. “For those who are interested in cost savings on fuel and maintenance, good technology is critical: even the most brilliant captain cannot see every change in the weather; even the most brilliant chief engineer cannot hear every problem in the machinery. For those who are interested in staying ahead of changing environmental legislation and the related cost of financing, automated measurements will provide an indispensable edge. And for those looking to reduce the cost and challenge of physical inspections and service – even in calmer times where there are no restrictions on mobility – digital solutions provide an answer. Smart use of these systems will gradually separate the winners from the losers, and it is encouraging to see leading players like DNV GL and AOT collaborate to accelerate this development.”

“By deploying AOT’s SMARTShip application on a vessel, surveyors can access real-time data,” says Capt. Rajesh Unni, Co-CEO of AOT. “The resulting advantage is that one can remotely access the health of a vessel and verify whether a ship is compliant with IMO 2020 and other regulatory requirements. This digital approach is reliable, efficient, and can improve savings.”

“By working together with leading technology solution providers, alongside owners and operators we can unlock broader maritime digitalisation and build on the value these new technologies generate,” said Cristina Saenz de Santa Maria, Regional Manager for South East Asia, Pacific & India at DNV GL Maritime. “At DNV GL we want to continue taking advantage of the opportunities created by digitalization to offer new services and ways of working that enhance quality, are more efficient, and improve our customers’ experiences with class. Of course, with every step towards greater digitalization we must make sure that we are continuing to ensure safe operations at sea, while protecting life, property and the environment.”

As the MOU implementation continues, the partners will look to cover many of the most important emerging areas for maritime digitalization, including remote monitoring and operations, the digital supply chain and predictive maintenance systems.

About DNV GL

Driven by our purpose of safeguarding life, property and the environment, DNV GL enables organizations to advance the safety and sustainability of their business. We provide classification, technical assurance, software and independent expert advisory services to the maritime, oil & gas and energy industries. We also provide certification services to customers across a wide range of industries. Operating in more than 100 countries, our professionals are dedicated to helping our customers make the world safer, smarter and greener.

About DNV GL – Maritime

DNV GL is the world’s leading classification society and a recognized advisor for the maritime industry. We enhance safety, quality, energy efficiency and environmental performance of the global shipping industry – across all vessel types and offshore structures. We invest heavily in research and development to find solutions, together with the industry, that address strategic, operational or regulatory challenges. For more information visit: www.dnvgl.com/maritime

Why should I pay any attention to spot container freight rates

Despite lower volumes being fixed in the spot market, it is key to tracking developments in the container shipping market, as it quickly responds to the changing situation and adjustments to demand and supply.

Why should I pay any attention to spot container freight rates?

Over the past two years, the container shipping industry has faced several challenges, many of which were felt on the Far East to US West Coast (USWC) route. This route has taken the biggest direct hit from the trade war that started in 2018 and which, despite the signing of the Phase One Agreement between the US and China, is not over yet. Adding to the trade war headaches were higher fuel costs due to the IMO 2020 Sulphur regulation that came into effect on 1 January 2020, and now, the coronavirus is causing volumes to drop.

Despite lower volumes being fixed in the spot market, it is key to tracking developments in the container shipping market, as it quickly responds to the changing situation and adjustments to demand and supply. On the other hand, the longer-term contract rates are key to understanding where profits in the liner

industry are being generated.

“The long-term contract rates generate the most money for carriers, but their stability hides the volatility that the market is facing. The trends in the spot market are a much better reflection of the market conditions globally, as well as on individual trade lanes, and can therefore offer important input into the decision making processes,” says Peter Sand, BIMCO’s Chief Shipping Analyst.

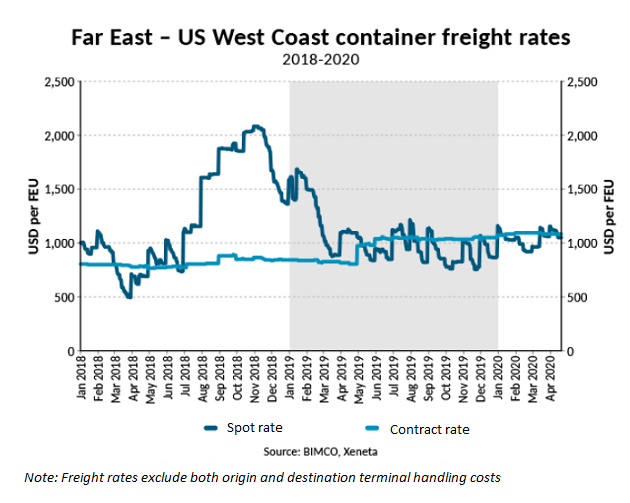

The volatile spot market; a better indicator than the more stable long-term contracts

The long-term contract rates have been very stable since the start of 2018 when they stood at USD 802 per forty-foot equivalent unit (FEU). They remained around that level until May 2019 when they rose to USD 974 per FEU and have since then been slowly creeping upwards to USD 1,083 per FEU on 21 April 2020 (source: Xeneta).

In the same period, the spot rates have given a better indication of what the container shipping market experienced. Here, the effects of frontloading towards the end of 2019, ahead of a tariff hike on US imports of goods from China, are clearly visible with rates quickly rising from USD 735 per FEU at the end of June 2018 to USD 2,066 per FEU in mid-November. As usual in the in the gap between the calendar new year and the Lunar New Year, spot rates remained elevated until the first quarter of 2019, after which volumes and rates fell as the stockpiling rush ended.

IMO 2020 did little to lift freight rates

The much talked about IMO2020-adjusted Bunker Adjustment Factors (BAFs) did little to lift freight rates on the Far East to US West Coast route as bunker prices rose in response to the 1 January 2020 implementation of the IMO Global Sulphur Cap. Carriers that managed to implement BAFs mainly did so by lowering the basic freight rate.

It is particularly clear on long term rates that the total cost of sending a container from the Far East to the USWC did not increase in response to the new environmental regulation. Short term freight rates experienced a small hike as we entered the new year: going from USD 870 per FEU on 31 December 2019 to USD 1,159 per FEU on 1 January 2020.

However, this was not enough to cover the additional fuel costs at that time, and in fact represents (mostly) normal seasonality with rates rising at the start of the new year, as more goods are shipped ahead of the lull in production in the far-eastern manufacturing hubs over the Lunar New Year.

“The overcapacity that is rife in the market limits carrier’s ability to pass on their additional fuel costs linked to compliance with the Sulphur Cap. Although the bunker fuel price spread, between high- and low-sulphur marine fuels, has narrowed considerably since the start of the year, this power imbalance between carriers and shippers continues to hinder higher rates,” Sand says.

Coronavirus has had little effect on freight rates, hiding the real story

Both long- and short-term rates have remained stable even as the coronavirus pandemic has forced large parts of the global economy to shut down and thereby lower demand for container shipping. Freight rates have been largely unaffected due to the many sailings that carriers have blanked, resulting in large scale capacity reductions on many of the world’s major container trades.

Carriers have chosen a range of measures to lower capacity, including the idling of ships, and blanking of sailings, which has driven the idle containership fleet to record highs in the past few months. On top of this, some carriers have chosen to slow down their ships or avoid expensive canal tolls. A few containerships have chosen the longer route around the Cape of Good Hope in South Africa, rather than the shorter and more expensive route through the Suez Canal. The falling oil price has resulted in lower bunker fuel prices, lowering the cost of sailing the longer distance to below that of the Canal tolls.

These measures also reduce the available capacity and artificially hold up freight rates.

“While the cost of freight per container has remained stable, the lower volumes and fewer sailings mean that although carriers can reduce some losses by blanking sailings, the disastrous effect that the coronavirus is having on their bottom lines is masked by the stable freight rates for the time being,” says Sand.

For more information about the container shipping market, BIMCO members can access Xeneta’s monthly container market report here, on the member’s only market reports page.

For more insight on the container shipping market, join Xeneta’s “Coronavirus crises and the trade war – port-pandemic world”.

bimco.org

Three hours with Dr. Martin Stopford

A Webinar on “Coronavirus, Climate Change & Smart Shipping – Three Maritime Scenarios 2020 – 2050”

New York, April 30, 2020. Over 1,000 worldwide participants had the chance to share into the wisdom and insight of one of the industry’s best known and most respected personalities.

Hosted by Capital Link on April 28, Dr. Martin Stopford, Non-Executive Chairman of Clarkson Research, presented his recently published White Paper “Coronavirus, Climate Change & Smart Shipping – Three Maritime Scenarios 2020 – 2050 – Preparing for Changes that are 'On the Cards'."

The webinar was scheduled to last an hour. However, after the introductory 40-minute slide presentation, Dr. Stopford responded to an avalanche of questions, that went on for another 2.5 hours. As the event drew to a close, Dr. Stopford stated this was his longest presentation ever!

THE WEBINAR

The shipping industry’s preparedness to meet the challenges of climate change and the digital revolution has been patchy and disjointed. The Covid-19 pandemic, with all its disruption, may be the catalyst for the radical changes needed to shift the status quo.

This was the first public presentation elaborating on Dr. Martin Stopford’s recently published White Paper. He outlined three scenarios that could come to define the evolution of the industry in the period 2020-2050 when the industry must rebuild its cargo fleet. The scenarios cover Sea Trade, Shipbuilding Requirements and Ship Technology.

As Dr. Stopford mentioned “We know we cannot predict the future. But we can try to prepare for changes that are clearly “on the cards”. Not preparing can be riskier and more expensive than the “safe” option of doing nothing.”

The White Paper and presentation can help the industry assess alternative strategies and prepare for the way ahead.

A replay of the webinar, together with the White Paper and the slide presentation are available at http://webinars.capitallink.com/2020/stopford/. Registration and download of the materials is complimentary.

CAPITAL LINK TRANSFORMS SHIPPING FORUMS GOING DIGITAL

Complementing its Investor Relations practice, Capital Link is also known for the organization of large-scale forums in key industry centers around the world. Annually, Capital Link holds over 15 forums in New York, London, Athens, Limassol, Singapore, Shanghai, Tokyo and Hong Kong, featuring industry leaders, addressing critical industry topics and attracting top level delegates.

Hinging on the extensive experience of organizing events and webinars and adapting to the challenges of this unprecedented environment, Capital Link is now pioneering in the transformation of select shipping forums into digital events.

On March 30-31, 2020, Capital Link turned its 14th Annual International Shipping Forum, originally scheduled to take place in New York, into the first digital large-scale Shipping Forum. Organized in partnership with Citi, it attracted over 3,000 delegates and featured a Who-Is-Who of the industry, with 96 speakers, including top executives from 35 listed shipping companies. The two-day forum featured 22 sessions, virtual networking opportunities and 142 investor meetings.

The library of content is available upon demand with free registration at http://forums.capitallink.com/shipping/2020newyork/

OPERATIONAL EXCELLENCE IN SHIPPING – JUNE 16-17,2020

On June 16-17, 2020, Capital Link will host its second full scale digital forum “Operational Excellence in Shipping.” In its 10th year running, traditionally taking place in London and Athens, this Forum showcases Operational Excellence in the Maritime Sector and explores Best Industry Practices across all major areas such as fleet management, technological innovation, crewing, energy efficiency and the environment, safety and security. This year special attention will be paid to the operational challenges from the Covid-19 reality, to sustainability and ESG considerations and new challenges in ship safety, security and human resources.

Mr. Kitack Lim, The Secretary General of the International Maritime Organization is the Keynote Speaker. The forum will also feature roundtable discussions with the heads of the major industry associations, classification societies, and shipmanagment firms, as well as CEOs and COOs from major shipping companies around the world. The event will run on London Time. Attendance is complimentary. More information can be found at http://forums.capitallink.com/csr/2020athens/

ABOUT DR. MARTIN STOPFORD

Martin Stopford is a graduate of Oxford University and has a PhD in International Economics from London University. During his 41 years in the Maritime Industry he has held positions as Director of Business Development at British Shipbuilders; Global Shipping Economist with Chase Manhattan Bank N.A.; Chief Executive of Lloyds Maritime Information Services and executive director of Clarksons PLC. He retired from Clarksons in May 2012 and is currently non executive President of Clarkson Research Services Limited (CRSL).

Martin is also a visiting Professor at Cass Business School in London, Dalian Maritime University in China, Newcastle University and Copenhagen Business School. He has an Honorary Doctorate from The Solent University; a lifetime achievement award at the 2010 Lloyds List Global Shipping Awards; and in 2013 was Seatrade Personality of the Year.

His publications include "Maritime Economics" 3rd Ed, the widely used shipping text book published in January 2009, and many papers on shipping economics and ship finance.

Martin's children Ben and Elizabeth both live in London. His main hobby, apart for shipping, is gardening and he runs a small organic hill farm in Staffordshire Moorelands.

ABOUT CAPITAL LINK, INC.

Founded in 1995, Capital Link is a New York based Advisory and Investor Relations firm with strategic focus on the maritime, commodities and energy sectors, MLPs, as well as Closed-End Funds and ETFs. In addition, Capital Link organizes 15+ conferences a year in the United States, Europe and Asia, all of which are known for combining rich educational and informational content with unique marketing and networking opportunities. Capital Link is a member of the Baltic Exchange. The webinars, podcasts and interviews are for informational and educational purposes and should not be relied upon. They do not constitute an offer to buy or sell securities or investment advice or advice of any kind. The views expressed are not those of Capital Link which bears no responsibility for them. For additional information please visit: www.capitallink.com, www.capitallinkwebinars.com, www.capitallinkpodcasts.com

ESPO proposes a two-step approach on the new EU Transport Strategy

The current global health crisis will require more than a “business as usual” update of Europe’s Transport Strategy

Since 2011, Europe has been facing numerous new challenges and has defined new policy ambitions. However, the health crisis the world is facing today risks to radically overturn current realities, assumptions and strategies. Our economy and life is affected in almost all its aspects and while we can hope for a quick recovery it is clear that we will not be returning to business as usual.

Since the start of the COVID-19 crisis, Europe’s ports have been doing everything possible to ensure the continuity of their operations and thus the security of supply. European ports have activated contingency plans to ensure that ports remain fully operational during this crisis. More than ever, European ports have been demonstrating their role as essential and critical infrastructures, playing a crucial role in the supply of necessary goods.

While ports are ready to embrace and adapt to a changed reality, it is at this moment still unclear how long the current major disruption of Europe’s economy and society will last, how severe the impacts will be, or what efforts will be needed to come to a “new normal” scenario. Although many ports are already feeling the impact of the slowdown of the global economy, the real, tangible impact for the entire port sector will only become clear as from the second quarter of this year.

ESPO therefore believes that in the absence of any insight on the duration and impact of the current crisis, it is, at this moment, impossible to set the ground for a long-term EU Transport Strategy.

ESPO proposes a two-step approach:

European ports believe that Europe’s first priority must now be to develop a restart and recovery plan which helps to overcome this crisis. It should develop the measures and instruments for Europe’s recovery to put the European economy and society back on track as soon as possible, while guaranteeing this happens in a safe way.

In the absence of a vaccine or treatment, an essential part of the short-term recovery measures has to be focused on re-starting economic activities, including transport, and societal behaviour, based on co-existence with the COVID-19 virus. Measures will be necessary to limit the risks of spreading the virus, among others by developing the necessary plans for enabling a 1.5 meter economy and society.

Moreover it will be important that existing policies and financial instruments for infrastructure projects in ports, in particular CEF, can be further strengthened to ensure that resilient sectors such as the port sector can rebound quickly after the crisis and pursue already planned investments. Advancing planned CEF calls could in that sense be a way of boosting investments in ports and allowing ports to further play their role as engines of growth.

During this first phase, the impact of the crisis and the recovery measures on both the European and national budgets must be evaluated in order to have a realistic picture of the available budget for implementing new ambitions and strategies.

In a second phase, as soon as the crisis situation stabilises, and the “new normal” sets in, the discussion should start on a new Transport Strategy, which will set the long-term goals, ambitions and initiatives for the European transport sector. The Strategy should integrate the consequences of and lessons learned from this crisis and should build on the new post-crisis reality.

While successful and proven policies, such as Europe’s Transport Infrastructure policy, should not be radically put into question because of this crisis and while ambitions addressing important challenges such as climate change should remain untouched, it is clear that the current COVID-19 crisis will require answers to new challenges and questions:

Is the critical role of transport, ports and strategic supply chains sufficiently ensured in Europe’s transport policy?

Will social distancing in transport be a short-term measure or part of the “new normal”?

Which of the current urgency measures enabling contactless transport and using digital solutions should be further developed and become part of a long-term transport strategy?

Is the security of digitalisation processes sufficiently ensured if home and smart working is further developed?

Are new supply chain patterns emerging, are reshoring and diversification of suppliers part of the “new normal”?

Will health checks and border controls be part of the long-term transport strategy or remain just a crisis response measure?

What is the impact of the new health and economic strategies on port infrastructure and investment projects?

ESPO and its members are happy to start the reflection with all stakeholders and EU decision makers in view of formulating clear answers to all these questions and setting the ground for a truly forward looking sustainable, connected, efficient and resilient transport system.

espo.be

Greek economy to shrink by 4.7 pct in 2020 due to the pandemic; strong growth in 2021

The Greek economy will contract by 4.7 pct this year due to the crisis of the pandemic, but it will return to positive growth rate next year with a 5.1 pct growth, unemployment is expected to reach 20 pct in 2020, while due to the lockdown private consumption, investments, imports and exports are expected to drop significantly, the Greek Finance ministry said in a reform program sent to the European Commission in the framewor of the European Semester

According to the ministry, the Greek economy suffers a triple shock: one temporary but very strong shock in supply. A lockdown reduces production of goods and services, along with incomes of producers and labour force, a very strong shock in demand as a lockdown reduces consumption and third a very strong shock of uncertainty since both the duration and intensity of the phenomenon were unknown.

1. The reform program envisages a 4.7 pct economic recession this year based on the assumption that a healthcare crisis will gradually recede after the first half of 2020, with the economic impact expected to be visible in the second quarter of the year. The economy is projected to recover with a 5.1 pct growth rate in 2021.

2. The unemployment rate is projected to rise from 17.3 pct in 2019 to 19.9 pct in 2020 and to fall to 16.4 pct in 2021.

3. Private consumption is expected to fall by 4.1 pct this year reflecting losses of income and a suspension of consumption spending due to measures to restrict social contacts. Consumption is expected to grow by 4.2 pct in 2021. On the other hand, public consumption is expected to grow by 1.0 pct due to increased state spending.

4. The inflation rate is expected to return to 2019 levels (harmonized consumer price index) to -0.3 pct in 2020, rebounding to 0.6 pct in 2021.

5. Private investments (gross fixed capital formation) are expected to fall by 4.6 pct and to jump by 15.3 pct in 2021.

6. The state budget's primary surplus is expected to significantly fall short of the 3.5 pct of GDP aim for 2020.

7. Exports of goods and services are expected to drop by 19.2 pct this year, while imports are projected to fall by 14.2 pct. Both exports and imports are expected to grow by 19.2 pct and 15.6 pct, respectively in 2021.

https://www.amna.gr/

![]()

Powered by ![]() © Μaritimes 2019

© Μaritimes 2019