-

Home

-

Maritimes NEWS

-

Ports

- maritimes

maritimes

China-EU investment pact mutually beneficial, says spokesperson

BEIJING, May 19 (Xinhua) -- China on Wednesday reiterated its position on relations with the European Union (EU), noting that the China-EU Investment Agreement is a balanced, mutually beneficial and win-win deal and not a gift from one side to the other.

Chinese Foreign Ministry spokesperson Zhao Lijian made the remarks at a daily press briefing saying that it is in the interests of both China and the EU to ratify the agreement at an early date and both sides should make active efforts in this regard.

China's sanctions against relevant personnel from the EU side for maliciously disseminating lies and disinformation involving Xinjiang and damaging China's sovereignty and interests were imperative to safeguarding China's own interests, as well as a legitimate and just response to the EU sanctions, Zhao said. "It is clear who acted first with unreasonable provocation and who responded in defense."

The spokesperson added that China has the right to develop its relations with Europe and will firmly safeguard its sovereignty, security and development interests.

Stressing that sanctions and confrontations will not help solve problems and dialogue and cooperation are the right approaches to forge ahead, Zhao said it is hoped that the European side will do some introspections, immediately stop interfering in China's internal affairs, enhance mutual understanding, properly manage differences and promote the healthy and stable development of China-EU relations through dialogue and communication. Enditem

Source: Xinhua

Dry Bulk Correction Underway. Where Is The Bottom?

The beauty of shipping investments is their cyclical nature embedded in the industry and although there are always explanations and reasons for each leg of the cycle, usually ex post, the plain reality is that shipping rates go up and down because this is just the natural behavior of the shipping market balance: Sometimes demand exceeds supply and sometimes the opposite is true. Such a balancing act happens all the time in short-term cycles but the market is also always subject to a broader industry-wide cycle, one that is mainly driven by the balance between global economic growth, and thus demand for commodity transportation, and the number of available ships to perform such a service.

We believe we are currently in such a long-term upswing which will last several years and is driven by major economic forces on both the demand and the supply side of the equation, but that does not mean prices won’t fluctuate, sometimes violently, during that period. Looking at the current state of the market, it seems we have now peaked near-term and we are in the midst of a correction, albeit a mild one in our view.

Once again, predicting peaks and troughs is a risky game, but for investors and market participants alike, the exact turning points should be less relevant as long as they are able to identify the majority of the moves on each direction.

History might be a useful first step in measuring the magnitude of the drawdowns. Looking at the freight rates during the past several years, there have been quite volatile periods so identifying the absolute top/bottom in each instance requires some qualitative judgment on top of quantifying the size of each rate decline. Moving averages of the respective indices might also be useful, while freight futures (given the embedded averaging in prices) is also a time series to consider in such exercise.

For the core Capesize sector, volatility has been much higher that the rest of the dry bulk sub-sectors. The spot nature of Capesize chartering combined with the much higher leverage that the economies of scale due to size provide, are the main reasons for such volatile performance. As a result, both rallies and drawdowns have been materially larger than the rest of the sector (i.e. Panamax and Supramax rates).

Below are some of the most important drawdowns in terms of % change as well as point drops on the Capesize Index over the past 20 years:

Percentage drop and point drop from most recent significant highs, Baltic Capesize Index

Note: shaded area excluded from the average calculation as absolute rates were much higher during that period

For comparison purposes, a 67% drawdown from he recent high means an index in the mid-teens while a ~18,000 drop places the index in the md/high 20,000 level. Currently the spot Capesize index stands at about 33,000 (although might soon drop below 30k, in our opinion).

However, it is very important to remember that the current dry bulk rally is NOT Capesize driven. Over the past decade, it was Capesizes that would lead the way and have the most important influence on the rest of the dry bulk sub-sectors. The current dry bulk rally is mainly driven by smaller, sub-cape vessels. In fact, Capesize fundamentals have not changed materially from last year in terms of cargo flow and vessel supply.

Such a setup makes it particularly tricky when it comes to the magnitude of the drawdown if indeed we are in the middle of a correction. For example, if Capesize rates drop significantly, charterers that might otherwise choose to use a Panamax vessel for a certain cargo might opt out for a Capesize one that has double the capacity and thus save on freight costs. Such a “substitution” factor makes it difficult to see Capesize rates below Panamax rates for a sustainable period of time. Although Panamax rates are also currently retreading, the relationship between different sizes of dry bulk vessels will play a very important role this time around in terms of the magnitude of the drawdown.

Baltic Dry Index

x

BDI .jpg

Our suspicion is that the drawdown will be shallower versus history, as the past decade had been particularly harsh in terms of the smaller size ships, and thus the “substitution” support has always been so much lower leading to deeper drawdowns for Capesize ships.

We believe we are close to halfway through the recent correction. Once again, it is impossible to identify bottoms or tops in such a volatile industry like shipping. History is a guide, but rarely it is an accurate predictor of the future. Freight futures also having a hard time identifying the bottom, and thus will continue to trade at the direction of spot, with the necessary risk premium or discount embedded. For now, the Capesize curve is in slight backwardation, but this is to be expected, given the fact that the index is still dropping.

Furthermore, looking deeper into seasonality, we expect another peak up in demand in late June. Although this year might play out quite different versus what the market is used to in terms of seasonal strength (see how strong the “seasonally weak” first half of the year already has been) it is interesting to us how market views have changed over time relating to seasonality. A few years back market participants would look forward to the second half of each year when dry bulk freight rates were expected to perform the best. Demand was high as China would restock commodities ahead of the winter while supply especially for iron ore out of Brazil would peak in the fourth quarter, thus aiding freight rates.

Currently we sense the opposite. Market participants see increasing risk of lower demand as the year progresses, reflecting China’s policy changes aiming at reducing pollution and controlling carbon emissions, combined with potential softening in economic activity as the stimulus boost gradually fizzles out.

All of the above are very valid concerns. Record-high commodity prices are taking a toll on China’s growth, inflation is becoming a mainstream subject while geopolitical conflicts (see Australia-China) are only intensifying. It is extremely difficult to handicap such major issues that would directly affect dry bulk rates.

Yet, here we are in May with Capesizes in the low-30,000s level, Panamaxes above 20,000 and smaller size vessels at their best in a decade. Vessel supply growth is slowing down, owners confidence is high, and the industry has already been through a decade of consolidating returns and sub-normal levels and is currently recovering.

More importantly, it is not only dry bulk that is pushing higher. Most major commodities, especially the ones that are linked to infrastructure (steel, iron ore, copper, lumber, cement and glass to name a few) are close to or above record highs. This is not a dry bulk rally. This is a infrastructure demand rally that is also affecting dry bulk.

Longer term, the significant focus on reducing carbon emissions in global shipping is also a bullish change, in our view, although that should play out over several years into the future. Major disruptions in technology and operations can only mean stronger pricing, at least in the early stages of such core changes. Slower steaming, limited new ordering and increased scrapping of older highly polluting vessels are all positive factors for the supply side of the shipping balance. Demand might fluctuate, but at least shipping has the supply side under control this time around (at least for now).

The current fundamentally-driven upcycle remains intact, in our view, and it is only the natural volatility of the industry that is scary sometimes but provides such attractive trading opportunities especially for the investors that choose to ignore the day to day fluctuations but focus more in the medium term turning points. We will find the bottom once again soon, and rates will turn up and another upcycle will develop, hopefully leading to a higher highs for the year.

Ammonia to power 45% of shipping in 2050 net-zero scenario: IEA

Ammonia and hydrogen will be the main marine fuels if the world reaches net-zero in 2050, accounting for about 60% of the market together and with ammonia occupying the largest share, the International Energy Agency said May 18.

Outlining its first road map for how the global energy sector can achieve net-zero emissions, the IEA said in such a scenario ammonia will account for 45% of energy demand from shipping.

Cost will be an issue. Small ammonia plants are expected to emerge worldwide beginning 2025, to produce green ammonia at $650-$850/mt ($34.95-$45.70/Gj), the Korean Register of Shipping, a not-for-profit ship classification society, said in a recent report.

After that, the cost is expected to drop to $400-$600/mt as larger plants are constructed in 2030 and then to further drop to $275-$450/mt in 2040, as consumption increases, favoring its use, it said.

By comparison, S&P Global Platts assessed delivered 0.5% fuel oil at Rotterdam at $484/mt May 17, equivalent to $11.10/Gj. Platts assessed methanol T2 FOB Rotterdam at $17.35/Gj.

Role of major ports

In any case, the supply of ammonia could be centered on major bunker ports, potentially at the expense of smaller ports.

“The 20 largest ports in the world account for more than half of global cargo [in the net-zero emissions scenario]; they could become industrial hubs to produce hydrogen and ammonia for use in both chemical and refining industries, as well as for refueling ships,” the IEA said.

Internal combustion engines

Ammonia can be burnt in an internal combustion engine — one of its advantages — and such engines for ammonia‐fueled vessels are being developed by two of the largest manufacturers of maritime engines. They are expected to become available on the market by 2024, the agency said.

Pure hydrogen is unlikely to play a major role in any large-scale marine international transportation because of its lower energy density, S&P Global Platts Analytics said February in its Future Energy Outlooks: Annual Guidebook 2021.

Ammonia does better on the energy density front but still compares unfavorably to diesel, although newly built vessels might be able to accommodate this, Platts Analytics said.

Biofuels and electricity

Sustainable biofuels will provide almost 20% of total shipping energy needs in net-zero 2050, the IEA said.

Electricity would occupy only a very minor share as the relatively low energy density of batteries compared with liquid fuels makes it suitable only for short-sea routes of up to 200 km (124 miles). Even with an 85% increase in battery energy density as solid state batteries become commercially available, only short‐distance shipping routes could be electrified, the IEA said.

Net-zero in 2050 will be a tall order. The global rate of energy efficiency improvement also needs to ramp up to 4% per year through 2030 — about three times the average over the last two decades, the IEA said.

Meeting the net-zero target requires total annual energy investment of $5 trillion by 2030, adding an extra 0.4 percentage point a year to global GDP growth, the agency said.

Source: Platts

Genco Shipping & Trading Limited to Acquire Two Modern, Fuel-Efficient Ultramax Vessels

Fixed Two Additional Vessels on Period Time Charters, Securing Cash Flows at Attractive Levels

NEW YORK, May 19, 2021 (GLOBE NEWSWIRE) -- Genco Shipping & Trading Limited (NYSE:GNK) (“Genco”) today announced that it has entered into agreements to acquire two 2022-built 61,000 dwt Ultramax vessels to be constructed at Dalian Cosco KHI Ship Engineering Co. Ltd. (DACKS). The vessels are expected to be delivered to Genco in January 2022.

The purchases mark the fifth and sixth high specification, fuel-efficient Ultramax vessels that Genco has agreed to acquire since December 2020, doubling its core Ultramax presence over that time. Genco intends to fund the acquisition from cash on the balance sheet on a low leverage basis.

Genco also announced that it has capitalized on the strong market to fix two additional vessels on period time charters to secure cash flows as part of its portfolio approach to fixture activity:

Baltic Bear (2010-built Capesize) fixed at $32,000 per day for 10 to 14 months

Genco Vigilant (2015-built Ultramax) fixed at $17,750 per day for 11 to 13 months beginning in October 2021

John C. Wobensmith, Chief Executive Officer, commented, “This latest acquisition continues the expansion of our fleet at an attractive point in the drybulk cycle as asset values continue to trail the strong freight rate environment leading to attractive returns on capital. Built at a first-class shipyard, we expect these two Ultramaxes will seamlessly integrate into our in-house commercial platform while reducing our carbon footprint as they replace older, less fuel-efficient vessels. These vessels continue our growth trajectory within the key Ultramax sector while improving the age profile of our asset base. Furthermore, acquiring these vessels on a low leverage basis enables us to continue to drive down our financial leverage and cash flow breakeven rate while augmenting our operating leverage. Growth together with deleveraging serve as primary components of our comprehensive value strategy as we continue to progress towards full execution in the months ahead.”

About Genco Shipping & Trading Limited

Genco Shipping & Trading Limited transports iron ore, coal, grain, steel products and other drybulk cargoes along worldwide shipping routes. Capesize vessels represent our major bulk vessel category and the other vessel classes, including Ultramax and Supramax vessels, represent our minor bulk vessel category. Our major bulk vessels are primarily used to transport iron ore and coal, while our minor bulk vessels are primarily used to transport grains, steel products and other drybulk cargoes such as cement, scrap, fertilizer, bauxite, nickel ore, salt and sugar. This approach of owning ships that transport both major and minor bulk commodities provide us with exposure to a wide range of drybulk trade flows. As of May 19, 2021, Genco Shipping & Trading Limited’s fleet consists of 17 Capesize, nine Ultramax and 14 Supramax vessels with an aggregate capacity of approximately 4,368,000 dwt and an average age of 10.4 years.

IMO’s Maritime Safety Committee adopts recommended actions to prioritize seafarers in national COVID-19 vaccination programmes.

The Maritime Safety Committee (MSC) of the international Maritime Organization (IMO) has highlighted the need for seafarers to be given priority access to COVD-19 vaccines, recognizing the unique and essential work of seafarers for international shipping and for the world.

The MSC adopted a resolution on “Recommended action to prioritize COVID-19 vaccination of seafarers”. The resolution recommends that Member States and relevant national authorities prioritize their seafarers, as far as practicable, in their national COVID-19 vaccination programmes (taking into account the WHO SAGE Roadmap). Proper consideration of extending COVID-19 vaccines to seafarers of other nationalities is also recommended, taking into account their national vaccines supply.

Member States are also recommended to consider exempting seafarers from any national policy requiring proof of COVID-19 vaccination as a condition for entry, taking into account that seafarers should be designated as ʺkey workersʺ, as they travel across borders frequently.

They should also develop appropriate plans, where feasible, to provide necessary infrastructure and facilities to support COVID-19 vaccination of seafarers. Given the limited period of time ships are in port, single dose COVID-19 vaccines for seafarers would be preferable.

The resolution recognizes the need to protect seafarers through vaccination, as soon as possible, to facilitate their safe movement across borders; while also noting the limited and highly uneven access to COVID-19 vaccines around the world, and highlights the importance of cooperation among the countries. The resolution also invites Member States, international organizations, shipping companies and other stakeholders to inform seafarers about the safety and possible benefits of the COVID-19 vaccination, bearing in mind that taking the vaccination is a decision made on an individual basis.

The resolution was adopted by the Maritime Safety Committee, meeting for its 103rd session from 5 to 14 May in remote session. ( Download the full resolution here: Recommended action to prioritize COVID-19 vaccination of seafarers Resolution.pdf)

Earlier this week, IMO Secretary-General Kitack Lim issued his personal call for IMO Member States to support a fair global distribution of COVID-19 vaccines, beyond fulfilling their national needs, to ensure seafarers can access vaccines. (Press briefing).

IMO COVID-19 resources page:

https://www.imo.org/en/MediaCentre/HotTopics/Pages/Coronavirus.aspx

17 Years of Quality Operations - Republic of the Marshall Islands Achieves QUALSHIP 21 Milestone

The Republic of the Marshall Islands (RMI) is pleased to be recognized for an unparalleled 17 consecutive years on the United States Coast Guard’s (USCG’s) QUALSHIP 21 roster. The RMI is the only one of the world’s three largest registries to attain QUALSHIP 21 status, while the two other flags in the “Big Three” did not make the grade and have been targeted now for two consecutive years. As reported in the recently published Port State Control in the United States 2020 Annual Report, the RMI remains a top performer for 2020, even in the face of extraordinary challenges.

More than 1,100 RMI flagged vessels were enrolled in QUALSHIP 21 in 2020, with an additional 78 having enrolled thus far in 2021. This means approximately one third of the QUALSHIP 21 certified vessels are flying the RMI flag, which illustrates the Registry’s dedication to high-quality standards fleetwide.

“We are exceptionally proud of our fleet and this unprecedented achievement which reflects our owners’ long-term commitment to high-quality and safe vessel operations,” said Bill Gallagher, President of International Registries, Inc. and its affiliates (IRI), which provide administrative and technical support to the RMI Registry. “Our owners, operators, and fleet operations teams work closely together to ensure high levels of compliance while also implementing new technologies to create a sustainable future for our industry,” he continued.

“This year was extraordinarily challenging for all industry stakeholders, specifically ships’ crews, and yet the RMI flag’s three year rolling average detention ratio stands at 0.74%, below the 1.02% USCG threshold for QUALSHIP21,” said Brian Poskaitis, IRI’s Senior Vice President, Fleet Operations. “The annual report is a real benchmark for us and reflects the coordination, professionalism, and focus our vessels and their crews have placed on compliance,” he continued.

In 2020, the RMI Registry issued Marine Safety Advisory 13-20, which allowed for remote inspections where a physical inspection was not advisable or permissible due to local restrictions. To date, 1,098 remote inspections have been conducted, with the ability to perform physical inspections constantly fluctuating due to the pandemic.

“Our close relationships and effective communication with our vessels and port State control authorities have enabled our teams to remain active with inspecting and identifying potential areas of concern,” said Brian Poskaitis. “Without the cooperation of the ships’ crews and owners/operators we could not have maintained this level of compliance and safe operations; we commend them for their tireless commitment,” he concluded.

The recognition comes on the back of the 2020 Tokyo Memorandum of Understanding report, released in April 2020, in which the RMI retained its preeminent whitelist status.

International Registries, Inc. and its affiliates (IRI), with more than 70 years of experience as a maritime and corporate registry service provider, has a network of offices in Baltimore/Annapolis, Busan, Dalian, Dubai, Ft. Lauderdale, Geneva, Hamburg, Hong Kong (Harbour Road and Gloucester Road), Houston, Imabari, Istanbul, Long Beach, London, Manila, Mumbai, New York (midtown and downtown), Piraeus, Rio de Janeiro, Roosendaal, Seoul, Shanghai, Singapore, Taipei, Tokyo, Washington, DC/Reston, and Zurich, that have the ability to register a vessel or yacht, including those under construction, record a mortgage or financing charter, incorporate a company, issue seafarer documentation, and service clientele. In order to meet higher expectations, IRI has expanded its worldwide coverage to include representation in Chile, Limassol, and Oslo. IRI concentrates solely on providing administrative and technical support to the Republic of the Marshall Islands flag and provides a broad spectrum of registry related services for the shipping and financial services industries.

www.register-iri.com

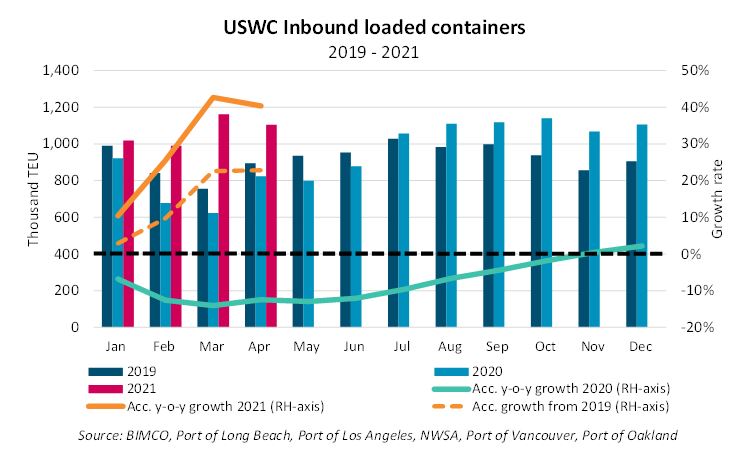

US West Coast imports exceed 1m TEU in nine out of ten past months

The surge in US container imports continued in April when West Coast loaded imports amounted to 1.10m TEU. Imports had never exceeded this level until August 2020, and developments in the past nine months mean that April imports are only the sixth highest on record. In the first four months of the year volumes are up by 40.3%, representing an increase of 1.2m TEU from the same period in 2020. Compared to 2019 volumes are still up by an impressive 22.8% (+793,500 TEU).

Imports decreased in April compared to March when volumes were record high at 1.16m TEU. The record high US West Coast imports helped make March the busiest month ever for global container shipping with 15.5m TEU being exported globally (source: CTS).

Retail sales also down from record high March

The slight decrease in loaded imports between March and April, matches the development in US retail sales, which after a record-breaking March (USD 629.9 billion) fell to USD 616.7 billion; still the second highest level on record. Before March, US retail sales had never exceeded USD 600 billion. Retail sales in both months were pushed up by the arrival of the USD 1,400 cheque, part of the latest stimulus round in the US, in late March and the first part of April, boosting US consumers’ spending on imported goods.

“The big question is how long these records will stand for? In terms of retail sales, with the March round of checks presumably the last, retail sales are unlikely to increase further in May,” says Peter Sand, BIMCO’s Chief Shipping Analyst.

“This does not necessarily mean that US West Coast imports have peaked with volumes remaining strong into May. High volumes, combined with continued congestion, has supported the continued strength of the transpacific freight market,” Sand says.

The high retail sales in March and April mean inventories need restocking, and the stop and start nature of the supply chain over the past year may be incentivising importers to get ahead on their usual schedules to avoid shortages further down the line. This would mean higher imports now, and in the next few months, potentially dampening some of the higher demand in the usual Q3 peak season.”

Diana Shipping Inc. Announces Signing of a Sustainability Linked Loan with ABN AMRO Bank to Refinance Four Separate Existing Loans

ATHENS, GREECE, May 18, 2021 – Diana Shipping Inc. (NYSE: DSX), (the “Company”), a global shipping company specializing in the ownership of dry bulk vessels, today announced that on May 14, 2021, it signed a sustainability linked loan facility with ABN AMRO Bank N.V., through six wholly-owned subsidiaries (the “Borrowers”), in the amount of US$91 million. The purpose of the senior secured term loan facility was the refinancing of existing indebtedness on the Borrowers' vessels, m/v Medusa, m/v New Orleans, m/v Los Angeles, m/v Philadelphia, m/v Santa Barbara and m/v Artemis, and for general corporate purposes.

Commenting on this transaction, the Company’s Chief Executive Officer, Ms. Semiramis Paliou, stated:

“We are pleased to have signed this loan agreement with ABN AMRO Bank N.V., which is in accordance with our policy of managing our cash flow and loan maturities proactively for the benefit of our shareholders. The added sustainability aspect is essential not only for the potential additional cost savings, but more importantly because it is in line with the Company’s commitment towards its long-term sustainability goals.”

Upon completion of the previously announced sale of one Panamax dry bulk vessel, the m/v Naias, Diana Shipping Inc.’s fleet will consist of 36 dry bulk vessels (4 Newcastlemax, 12 Capesize, 5 Post-Panamax, 5 Kamsarmax and 10 Panamax). As of today, the combined carrying capacity of the Company’s fleet, including the m/v Naias, is approximately 4.7 million dwt with a weighted average age of 10.24 years. A table describing the current Diana Shipping Inc. fleet can be found on the Company’s website, www.dianashippinginc.com. Information contained on the Company’s website does not constitute a part of this press release.

About the Company

Diana Shipping Inc. is a global provider of shipping transportation services through its ownership of dry bulk vessels. The Company’s vessels are employed primarily on medium to long-term time charters and transport a range of dry bulk cargoes, including such commodities as iron ore, coal, grain and other materials along worldwide shipping routes.

Signal's forecasting algorithm receives US patent

Signal Group's artificial-intelligence (AI) driven forecasting algorithm, Carrier Path Prediction Based On Dynamic Input Data, has been awarded a US patent.

The Athens & London-based business has drawn on its rich mix of shipping, computing and scientific expertise to develop an advanced prediction model for the maritime community.

Ioannis Martinos, Chief Executive Officer at the Signal Group, said:

"Receiving our first US patent is a tremendous milestone for the Signal Group. The patent powers our sophisticated voyage forecasting capabilities. I am really proud of our team which is demonstrating that the Greek tech ecosystem can offer cutting edge solutions for global industries!”

Signal, with offices in Athens and London, is developing AI software for the maritime transport and commodities trading sectors, combining a deep understanding of the shipping industry with a passion for applied science.

For the last three years, Signal’s services have been adopted at an increasing rate by international oil majors and traders, as well as shipping operators and brokers. Signal customers currently control more than 50% of the world's crude oil shipments.

The algorithm, which has drawn inspiration from the field of self-driving cars, uses graph theory and allows Signal to achieve reliable predictions in a space of high uncertainty. Its mathematical generality helps in the progressive integration of new input parameters and facilitates the expansion of the offered solutions to all types of merchant ships, such as tanker, dry bulk, LNG and LPG vessels.

Established in 2014 The Signal Group is a diversified shipping services group with offices in London and Athens. The Signal Group offers commercial ship management services to a pool of Aframax class oil tankers. In addition, The Signal Group develops and invests in next generation shipping related software technologies. It is led by an executive team who has more than 65 years of collective experience in ship management at the highest level. The leadership team is supported by a world-class mix of commercial shipping professionals, finance professionals, strategists, energy market analysts, data scientists and developers.

www.thesignalgroup.com

ECSA welcomes the communication on a new approach for a sustainable blue economy in the EU

The European Commission published yesterday its communication on a new approach for a sustainable blue economy in the EU. This communication highlights the important role of all the sectors related to oceans, including shipping, to boost the green and digital transition of the blue economy.

ECSA welcomes the publication of the communication on a new approach for a sustainable blue economy in the EU. The communication highlights the importance of the contribution of the blue economy to achieve carbon neutrality, by developing offshore renewable energy and by greening maritime transport and ports.

Furthermore, the Commission aims at promoting the use of EU funds to green maritime transport by increasing the uptake of short-sea shipping instead of using more polluting modes, as well as renovating the EU’s maritime fleet, such as passenger ships and supply vessels for offshore installations, to improve their energy efficiency.

In addition, the communication underlines the importance of Maritime Spatial Planning to reach a more sustainable blue economy. ECSA think that ensuring a fair and responsible co-existence between the sea users, including shipping, is essential. ECSA thus welcomes the Commission’s announced objective to prepare proposals to facilitate cross-border cooperation and encourage Member States to integrate offshore renewable energy development in their national spatial plans.

“The communication rightly highlights the crucial role of shipping in the sustainable blue economy, in particular the role of short sea shipping and of the offshore segment,” said Martin Dorsman - ECSA Secretary-General. As highlighted in ECSA’s position paper on the EU “Strategy to harness the potential of offshore renewable energy for a climate neutral future” European shipowners play a constructive role in advancing the ocean energy source in Europe and around the world. A sustainable blue economy needs to be built on a strong maritime spatial planning, to ensure that the highest level of safety is guaranteed for all the sea users, including shipping.

However, ECSA is deeply concerned that the Commission seems to be determined to extend the scope of the Ship Recycling Regulation before a proper evaluation of the existing legislation and an impact assessment takes place. Such an announcement does not seem to be evidence based, goes against the Commission’s better regulation principle, and creates uncertainty for operators.

ecsa.org

![]()

Powered by ![]() © Μaritimes 2019

© Μaritimes 2019