-

Home

-

Maritimes NEWS

-

Ports

- maritimes

maritimes

Cyprus Shipping is here: more Competitive, more Extrovert, more Adaptable, more Sustainable than ever

«Cyprus has a proud maritime history and is committed to ensuring this continues into the long-term future. Since its establishment, the Cyprus Shipping Deputy Ministry has achieved significant growth and has always taken a proactive approach to maritime policies which support a sustainable shipping industry.

From green incentives to reward shipowners achieving reduced emissions, to a progressive approach to creating new programs enabling safe crew changes, Cyprus has always taken a practical approach to finding solutions.

Shipping is facing some of the most challenging years in its history. Understanding and complying with multiple new regulations, uncertainty as to the road to decarbonization, and navigating the ongoing impacts of COVID-19 are all placing enormous pressure on the industry. Cyprus continues its ongoing support through leadership and action - proactively driving progress on both a regional and international level to create a sustainable future for shipping».

United States Coast Guard Annual Performance Report

Ballast water management: Why electro-chlorination?

Compliance, operability and reducing OPEX are at the forefront of all shipowners' minds.

There is an array of Ballast Water Treatment Systems (BWTS) on the market, but effectiveness in real-world conditions can vary wildly.

The most popular systems include: Full-flow electro-chlorination technology, ultra-violet technologies, side-stream ballast water systems and filterless systems. But according to Clarksons Research (August 2020), 46% of the market has installed electro-chlorination BWTS.

ERMA FIRST believes a full-flow electro-chlorination proposition is the best all-round offering, both in terms of effectiveness and reducing OPEX.

A two-pronged attack

The ERMA FIRST FIT BWTS comprises of a filter stage, followed by full flow electro-chlorination. Sea water is used in the disinfection stage to generate the requisite amount of disinfectant through the electrolysis of the filtered ballast water.

It also employs special electrodes that allow a broad environmental envelope of operation, while offering flexible solutions for both safe area and hazardous zone installation.

Water salinity and clarity can seriously affect the ability of a BWMS to work to its full potential. However, a full-flow electro-chlorination system - which is supported by filtration - can manage large volumes quickly with low power consumption. Turbidity and low ultraviolet transmissivity do not present the same challenges to an electro-chlorination system as they ordinarily would to a UV system.

"Not only does the ERMA FIRST FIT BWTS need minimal power requirements, it also doesn't take up valuable cargo space," said Konstantinos Stampedakis, managing director at ERMA FIRST. "It's designed to be installed quickly and includes intelligent controls and artificial intelligence for real-time remote monitoring.”

The system is designed to deliver compliance for ships trading globally and has been uniquely tested and certified with three different 40µm basket filters. Each filter’s performance has been proven in conjunction with the specially designed electro-chlorination cells. The achieved bio-efficacy meets and exceeds the dis-charge standards as defined by the IMO and US Coast Guard.

Focusing on OPEX

BWMS contributes to ship operational expenditure either directly or indirectly. BWMS power consumption is a direct OPEX. A stay in port due to BWMS flow restrictions in challenging water conditions would be regarded as an indirect cost.

Reduced UV intensity due to ageing UV lamps and quartz sleeves is an important example because it impacts UV dose, where flow reduction and/or power ramp up are resultant countermeasures. Operational modes designed to deal with specific operational challenges, in addition to system design limitations (SDL), provide a reasonable indication of factors that contribute to BWMS OPEX.

"With UV and electro-chlorination BWMS, there are significant OPEX differences between these two types of systems," said ERMA FIRST chief technology officer Stelios Kyriacou.

"For a BWMS operating in seawater conditions with low water turbidity, a filter-UV system will be operating at the lower level of power as UV transmittance is high (>70%). An equivalent filter-EC system will also operate at low power levels due to favourable salinity conditions. However, the key difference is electro-chlorination system operates only on ballasting, a UV system is also used at de-ballasting hence the power related costs are significantly higher."

tradewindsnews.com

Brexit’s Impact on UK Trade – what is really happening?

While the UK formally left the EU and the European Common Market Area in January 2020, the Transition Period which was in place until 31st December 2020 allowed for the trade relationships between the UK and the EU to continue essentially unchanged. Now that Brexit has officially come into force, we can examine the impact it has had on bilateral trade between the UK and its trading partners. VesselsValue’s AIS and GIS derived trade flow data offers a unique perspective from which to assess trade impacts, tracking imports and exports in real-time. This provides up-to-date views of trade patterns ahead of most official statistics.

The Context – Brexit and Covid-19

The year 2020 was truly a year of challenge and change as the enormous interruptions to economies worldwide due to the Covid-19 pandemic had significant impact on trade patterns, globally as well as in the UK. With Brexit having occurred while the wider economy was still affected by the pandemic, any changes in trade volumes could be attributable to:

- The impact of higher tariffs / non-tariff costs of doing trade after Brexit.

- The impact of the pandemic on wider economic activity and demand levels.

- Traders’ behaviour in attempting to alleviate some of Brexit’s anticipated effects.

Within this context of overlapping and interlinked influences, the detailed and real-time data based on VesselsValue’s tracking of the global maritime fleet allows us to begin to disentangle the impacts of Brexit on trade over time and across different sectors.

Brexit – the impact on trade volumes

While aggregate trade statistics are an important indicator and commonly cited, any policy or regulatory change is likely to affect different economic sectors differently.

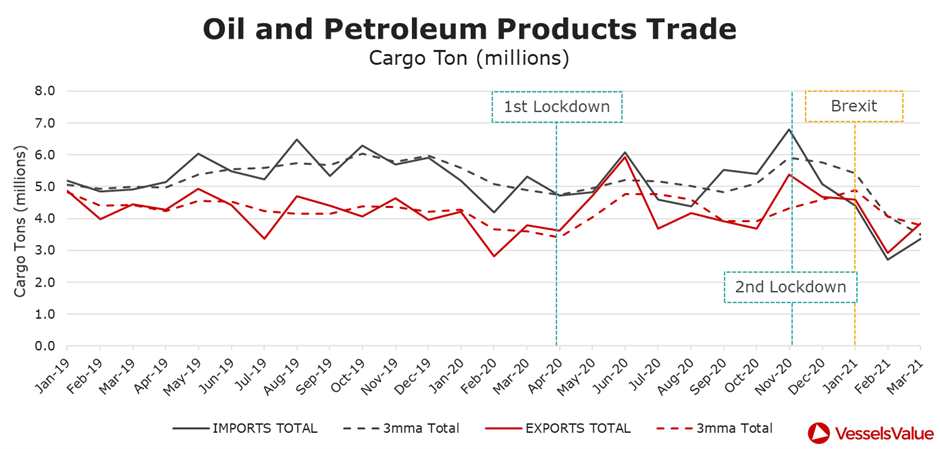

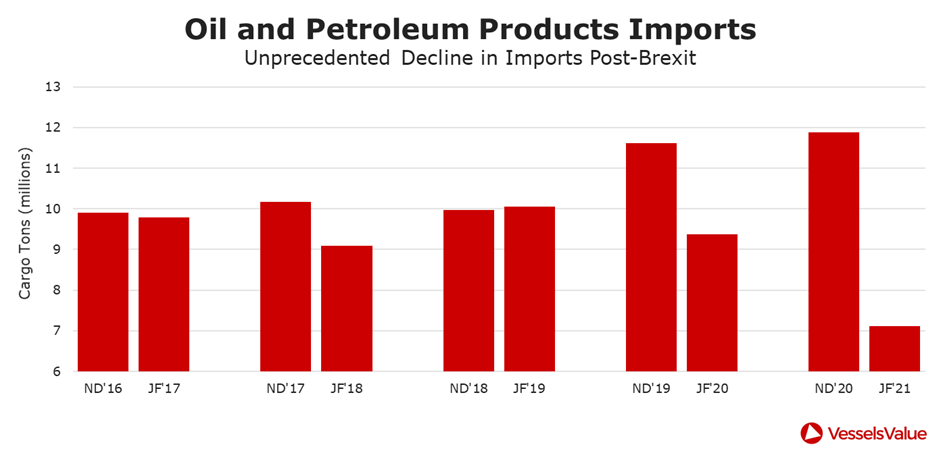

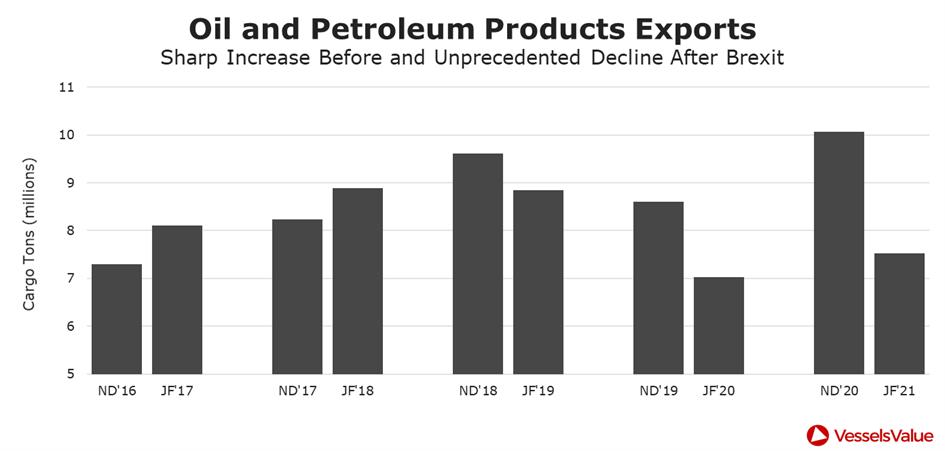

Oil and petroleum products – imports and exports fall to their lowest in recent history

For Oil and petroleum products, while trade rebounded sharply after the initial lockdowns, activity settled at a broadly reduced level for the summer months. Towards the end of the year, November registered the largest volume of imports going back to at least 2015 at 6.79mt. This burst of activity was short-lived, however, and was followed by a sharp drop to a February low of 2.7mt (the lowest since 2015 by some margin). While we saw a slight recovery in March, imports remain extremely weak. Exports from the UK, while somewhat less volatile than imports, followed the same pattern.

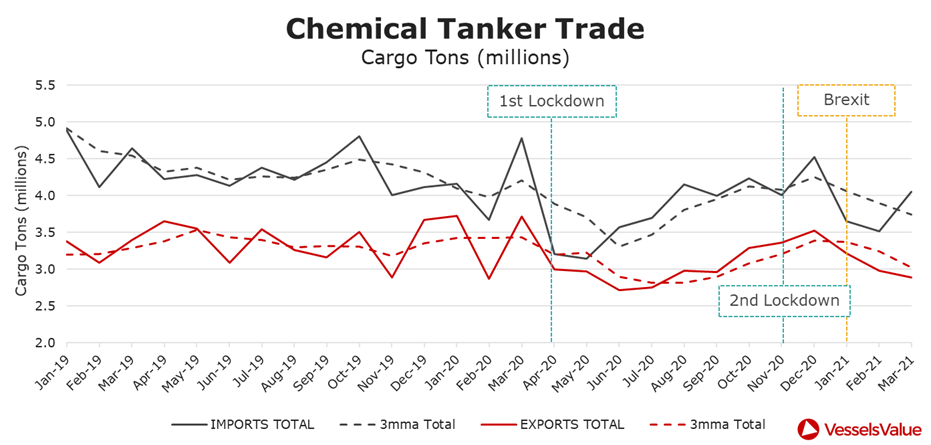

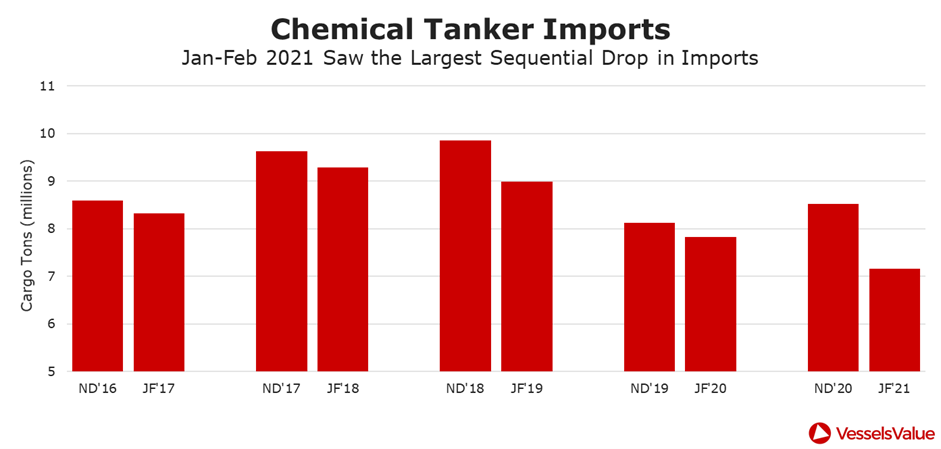

Chemical products – sharp decline post Brexit

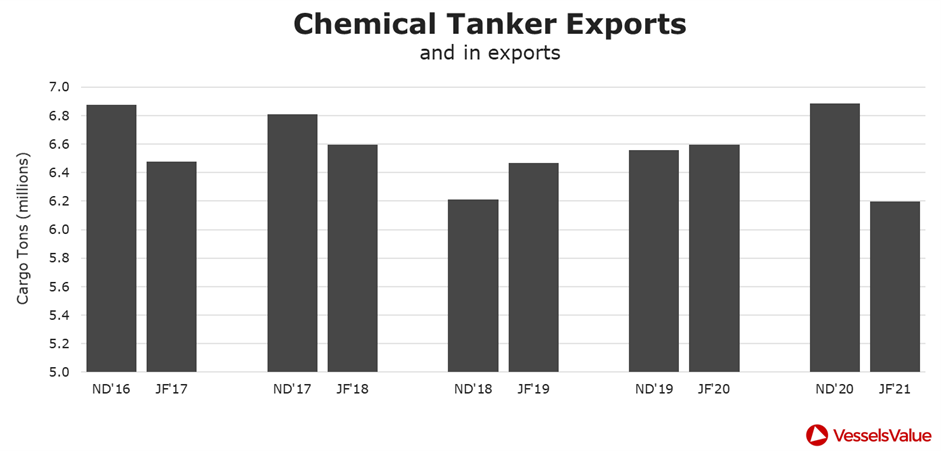

Chemical products show a similar pattern to Oil and petroleum products, with substantial weakness in both imports and exports after the first lockdowns in early 2020. Following a ramp-up in activity towards the end of the year, “real Brexit” brought renewed declines in trade in early 2021. Unlike the Oil sector, the UK’s Chemical product exports continued to decline into March.

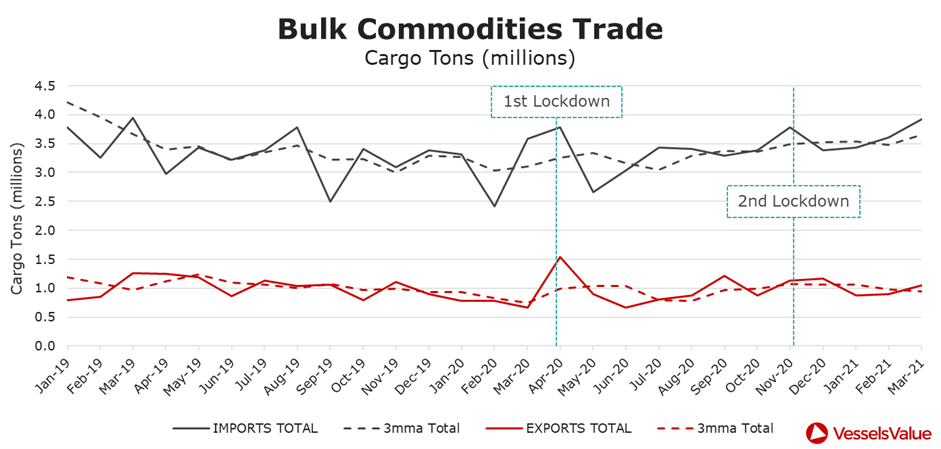

Dry Bulk Commodities trade – “steady as she goes”

Dry Bulk Commodities are seeing volatile trade, but very different patterns of impact to Oil or Chemicals. Activity has been far more resilient, with imports in particular picking up strength into 2021.

Brexit – the evidence for pre-Brexit stockpiling

While Brexit itself has clearly impacted trade, there could be impacts driven by the expectation of Brexit and what would happen after it took place. For example, if a UK importer expects an increase in either tariff or non-tariff costs of trading, they may choose to build up inventories in the UK ahead of the Brexit date and increase their imports. Similarly, if a UK importer expects GBP weakening after Brexit, they too will have an incentive to build up inventories ahead of Brexit. Similar considerations apply to overseas-based importers, who will have incentives to build up inventories of UK-sourced products ahead of Brexit if they expect trade costs to increase or GBP appreciation.

Using detailed VesselsValue AIS and GIS derived trade flow data, we can examine whether the UK’s imports or exports reveal a certain amount of precautionary inventory building ahead of Brexit itself. To analyse this, we have considered the volume of trade in the two months following Brexit (Jan-Feb ’21) relative to the two months immediately before Brexit (Nov-Dec ’20) and compared those volumes to recent history.

Oil and petroleum products – significant apparent build-up of inventories

UK-based importers of Oil and petroleum products appear to have engaged in a significant amount of precautionary inventory building just before Brexit. Considering the volume of imports in the 2 months preceding Brexit, we have seen the highest level of imports in recent history and 2% higher than in 2019 despite a smaller economy than in the previous year. This was immediately followed by a 40% drop in imports in the first 2 months following Brexit.

Considering the behaviour of importers of UK-origin Oil and petroleum products, we again see a substantial increase in purchasing immediately before Brexit (17% higher year-on-year), which is then followed by a 25% decline into January-February.

Chemical products

While not as drastic as Oil and petroleum products, we have strong evidence of precautionary purchasing in Chemical product markets as well – both by UK importers and by overseas importers of UK products. For example, while UK imports were 5% higher in November-December than in the previous year, they declined by 16% during January and February.

Similarly, UK exports of Chemical products showed a significant increase just before Brexit (+5% year-on-year), which was then followed by a very significant drop immediately after Brexit of -10%.

Dry Bulk Commodities

When considering whether UK-based or overseas-based traders undertook any stockpiling of dry bulk commodities ahead of Brexit, in the expectation of increased costs or adverse currency moves following Brexit, the sector again shows a very different pattern to either the Oil or the Chemicals sectors. Specifically, there is no evidence of inventory building in dry bulk commodities, either by UK-based importers or by overseas importers of UK-origin products.

Brexit – the impact on trade partnerships

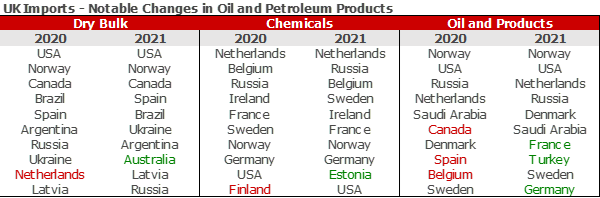

In addition to the volume of trade over time and across sectors, VesselsValue detailed shipping data allows us to examine how Brexit is impacting the UK’s trading relationships.

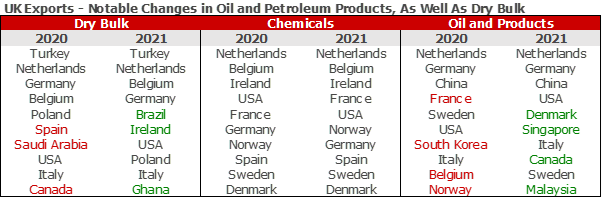

Considering the top 10 trading partners for UK importers in each sector, there has been very little change in where the UK sources imports from between 2020 and the first 3 months of 2021. In Dry Bulk commodities, The Netherlands has been replaced by Australia. While the UK’s relative share in the global Dry Bulk trade is small, shifts like this, if prolonged and widened further, could prove supportive for Dry Bulk shipping markets.

Regarding UK exports, there is no change in the top 10 trading partners for Chemicals, but there have been notable changes in both Dry Bulk and Oil and petroleum products. While the changes in Dry Bulk are relatively less impactful due to the UK’s relatively small scale in this market, in Oil and petroleum products the UK has replaced three short-sea destinations (France, Belgium, Norway) with three much more distant trading partners (Singapore, Canada, Malaysia). This analysis is based on three months of data since the affective Brexit took place. However, if that shift in who the UK trades with is sustained or expanded further going forward, it could have more significant implications for demand and supply in the Tanker shipping markets.

Summary

VesselsValue’s rich and real-time trade data allows us to analyse in detail, and ahead of the release of official statistics, the UK’s emerging trade patterns as we move into the “post Brexit” phase. There is clear evidence for significant declines in Oil, petroleum product and Chemical product trades immediately after Brexit. Apart from a general slowdown of economic activity associated with the effects of Covid-19 and increased costs of doing business post-Brexit, there is strong evidence to suggest that at least part of the decline in trade sector-wide in early 2021 has been driven by precautionary building up of inventories in the final months of 2020. This suggests that much of the decline in trade we have witnessed may reverse as those inventories begin to draw down.

We will continue to monitor the trade situation and report on any further developments.

Trade Data from VesselsValue as of May 2021.

Disclaimer: The purpose of this blog is to provide general information and not to provide advice or guidance in relation to particular circumstances. Readers should not make decisions in reliance on any statement or opinion contained in this blog.

EuroDry Ltd. Reports Results for the Quarter Ended March 31, 2021 and Announces Agreement to Acquire M/V Blessed Luck, a 2004-Japanese Built Panamax Bulker

Maroussi, Athens, Greece – May 20, 2021– EuroDry Ltd. (NASDAQ: EDRY, the “Company” or “EuroDry”), an owner and operator of drybulk vessels and provider of seaborne transportation for drybulk cargoes, announced today its results for the three-month period ended March 31, 2021 and an agreement to acquire M/V Blessed Luck, a 76,704 dwt drybulk vessel built in Japan.

First Quarter 2021 Highlights:

• Total net revenues of $8.6 million; net income of $0.9 million; net income attributable to common shareholders (after a $0.3 million dividend on Series B Preferred Shares and a $0.1 million preferred deemed dividend arising out of the net redemption of approximately $3 million of Series B Preferred Shares in the first quarter of 2021) of $0.4 million or $0.19 earnings per share basic and diluted. Adjusted net income attributable to common shareholders1 for the period was $1.3 million or $0.55 earnings per share basic and diluted.

• Adjusted EBITDA1 was $4.0 million.

• An average of 7.0 vessels were owned and operated during the first quarter of 2021 earning an average time charter equivalent rate of $14,924 per day.

• The Company declared a dividend of $0.3 million on its Series B Preferred Shares. The dividend will be paid in cash.

M/V Blessed Luck Acquisition

The Company also announced that it has agreed to acquire M/V Blessed Luck, a 76,704 dwt drybulk vessel built in 2004 in Japan, for $12.12 million. The vessel is majority owned by a third party and has been managed by Eurobulk Ltd., also the manager of three of the Company’s vessels. The vessel is expected to be delivered to the Company within May 2021.

he acquisition will be financed partly by a short term sellers’ credit of $5 million and an one year bridge loan of $6 million provided by an entity affiliated with the Company’s Chief Executive Officer with the remaining funds coming from the Company; both the sellers’ credit and short term loan carry an annual interest of 8%. In parallel, the Company is in the process of arranging 1Adjusted EBITDA, Adjusted net income/(loss) and Adjusted earnings/(loss) per share are not recognized measurements under US GAAP (GAAP) and should not be used in isolation or as a substitute for EuroDry’s financial results presented in accordance with GAAP. Refer to a subsequent section of the Press Release for the definitions and reconciliation of these measurements to the most directly comparable financial measures calculated and presented in accordance with GAAP.

2 a bank loan with the acquired vessel as collateral, expected to be finalized within approximately three months, which will provide sufficient funds to repay the sellers’ credit and, possibly, part of the bridge loan. At the same time, the Company entered into a charter agreement for the vessel for a period between a minimum of 11 months and a maximum of 13 months at a rate of $19,500/day which will commence upon delivery of the vessel and contribute about $4 million of EBITDA during the minimum period of the charter.

Aristides Pittas, Chairman and CEO of EuroDry commented:

“In stark contrast to a year ago, it has been a very positive 2021 so far with drybulk rates rebounding significantly as a result of solid trade growth and limited supply growth. The latter, especially, is constrained by short and medium term factors: in the short term, by inefficiencies in the vessel-port transportation system that resulted from COVID-19 effects and required protocols and, in the medium term, by the lowest orderbook in the last 20+ years. We believe that the market is likely to remain strong for the next couple of years provided that demand for transportation of drybulk cargoes -which is generally linked to economic activity- will maintain at least a historically average growth rate; it is noteworthy that the IMF, amongst others, predicts that economic activity will rebound above historical average levels as the world recovers from the COVID-19 pandemic.

In such a positive environment, our main strategy is to try to expand our fleet in a risk efficient way despite our limited funds available for investment. Thus, we acquired M/V Blessed Luck, a 2004-built vessel, with a combination of seller and affiliate bridge loans to complement our cluster of medium age Japanese-built Panamax-size vessels alongside our cluster of own-built newbuildings. The acquisition of M/V Blessed Luck will increase our fleet to eight units and is expected to contribute to a proportional increase in our EBITDA. At the present market rate levels, we are to accumulate funds that will provide us with several investment or expansion options or shareholder reward models. We, further, believe that the strong drybulk markets enhance the value of our public listing as a consolidation platform and we continuously investigate opportunities to take advantage of it.”

Tasos Aslidis, Chief Financial Officer of EuroDry commented:

“Our net revenues for the first quarter of 2021 were higher by 69.3% as compared to the first quarter of 2020. This was the result of higher average charter rates by 89.3% earned during the quarter as compared to the first quarter of 2020 and 38.7% higher when compared to the fourth quarter of 2020.

Total daily vessel operating expenses, including management fees, general and administrative expenses, but excluding drydocking costs, increased by approximately 8.5% during the first quarter of 2021 compared to the same quarter of last year. This increase is mainly due to increased crewing costs in 2021 compared to 2020, resulting from difficulties in crew rotation due to COVID-19 related restrictions.

Adjusted EBITDA during the first quarter of 2021 was $4.0 million compared to $0.6 million achieved for the first quarter of last year. As of March 31, 2021, our outstanding debt (excluding the unamortized loan fees) was $56.0 million versus restricted and unrestricted cash of approximately $6.2 million.”

CLIA welcomes the restart of cruise tourism in Greece

Athens, 20 May 2021. CLIA welcomes the restart of cruise tourism in Greece as of May 14th, in line with the timeline presented months ago by the Greek government. Since last year, cruise resumption has been the result of extensive and fruitful collaboration between the cruise industry, the Greek Government, health authorities, and ports.

More than 20 cruise lines are currently scheduled to set sail on cruises around Greece this year, with calls at 45 ports in total, demonstrating the dynamics of the industry as well as the dynamics of Greece as a top cruise destination. At least 15 of these cruise lines will home port in Greece. Remarkably, cruise operations started from day one of the reopening with 4 cruise lines already expected to operate during May. In total almost 40 cruise ships are projected to sail in Greece this year.

“We are extremely happy with the restart of cruise travel in Greece. The restart marks the culmination of the excellent collaboration our industry has with the Greek government. In particular, Minister of Tourism Theocharis and Minister of Maritime Affairs & Insular Policy Plakiotakis, with their structured and focused work on the restart timeline and the ports’ preparedness, helped to make cruise travel possible again, on time” says Maria Deligianni, National Director Eastern Mediterranean, CLIA.

“We are extremely happy with the restart of cruise travel in Greece. The restart marks the culmination of the excellent collaboration our industry has with the Greek government. In particular, Minister of Tourism Theocharis and Minister of Maritime Affairs & Insular Policy Plakiotakis, with their structured and focused work on the restart timeline and the ports’ preparedness, helped to make cruise travel possible again, on time” says Maria Deligianni, National Director Eastern Mediterranean, CLIA.

The health and safety of passengers, crew and destinations are an operational imperative and priority for CLIA members as cruise lines resume operations responsibly. Our industry-leading protocols, which were developed in collaboration with EU Healthy Gateways, national governments, public health authorities and ports, go beyond those found in nearly any other setting, giving the government, passengers, and crew confidence that the latest science and medical advice has been included in the industry’s planning.

CLIA members account for 95% of global ocean-going cruise passenger capacity, and the CLIA Member Policy for Mitigation of COVID-19 applies to all CLIA ocean-going cruise lines worldwide carrying 100+ persons travelling on itineraries to international waters. The focus is on strict embarkation procedures and on universal (100%) testing of passengers and crew, together with new sanitation procedures on board, strong monitoring mechanisms and strict rules for shore excursions.

This great momentum for cruise tourism in Greece will be highlighted in the coming Posidonia Sea Tourism Forum 2021, the bi-annual international Conference & Exhibition dedicated to cruising and sea tourism, taking place on May 25th, where all major industry players and stakeholders will exchange ideas and share initiatives for post-pandemic cruising. Pierfrancesco Vago, CLIA Global Chairman and Executive Chairman, MSC Cruises, Ukko Metsola, Director General, CLIA Europe, and Maria Deligianni, National Director Eastern Mediterranean, CLIA, will address the Forum, discussing the latest challenges for the industry as well as the importance of Greece as a cruise destination.

The return of cruise in Greece is a welcome boost to the cruise communities and the people employed in the Greek cruise sector, which generates almost 1 billion euro to the Greek economy, as well as those whose livelihoods depend upon the industry, including travel agencies, tour guides, port operators and many other service providers across the country. With more than 5 million passenger visits per year, Greece continues to be one of the most popular cruise destination countries globally.

About the Cruise Lines International Association (CLIA)

CLIA is the world’s largest cruise industry trade association, providing a unified voice and leading authority of the global cruise community. On behalf of the industry, together with its members and partners, the organization supports policies and practices that foster a secure, healthy and sustainable cruise ship environment, as well as promote positive travel experiences for the more than 30 million passengers who cruise annually. The CLIA community includes the world’s most prestigious ocean, river and specialty cruise lines; a highly trained and certified travel agent community; and cruise line suppliers and partners, including ports and destinations, ship development, suppliers and business services. The organization's global headquarters are located in Washington, DC, with regional offices located in North and South America, Europe, Asia and Australasia. For more information please visit the website www.cruising.org or follow CLIA in Facebook, in Twitter and LinkedIn.

Snam, RINA and the GIVA Group: the world’s first test with a 30% natural gas/hydrogen blend in steel forging

The mix was used to power furnaces at the Rho plant of Forgiatura A. Vienna (GIVA Group)

The world’s first test of a 30% natural gas/hydrogen blend in the forging processes used in industrial steelmaking was held in Rho (province of Milan), at the Forgiatura A. Vienna plant.

The trial involved the use of the hydrogen/gas mix to heat the furnaces of the Forgiatura A. Vienna plant and was successfully carried out on site after a series of studies and laboratory tests lasting about a year. The companies involved in the initiative were: Snam, one of the world’s leading energy infrastructure companies and developer and promoter of the project; RINA, a multinational inspection, certification and engineering consultancy, which handled the engineering analyses and laboratory phase; and GIVA Group, a global leader in steelmaking, which made Forgiatura Vienna available for the field test. The blend of methane and hydrogen was supplied by Sapio, an Italian company specialising in the production and marketing of industrial and medical gases.

Marco Alverà CEO of Snam commented: “In the medium to long term, hydrogen is in a position to become the solution for decarbonising steelmaking as well as all hard-to-abate industrial sectors that have a fundamental role in our economy. This trial is a preparatory step to the gradual introduction of zero-emission hydrogen, initially blended with natural gas and then in pure form, in certain steelmaking production processes. Snam intends to make its infrastructure, research and expertise available to contribute to the creation of a national hydrogen supply chain and to the achievement of domestic and European climate targets”.

Ugo Salerno, Chairman and CEO of Rina added: “This test is the concrete proof that Italy’s hydrogen production chain can significantly contribute to decarbonising complex and energy-intensive industries such as steelmaking. At Rina we are proud to play an active role in the ongoing energy transition, more specifically in such events where we can share our energy and industrial know-how”.

Jacopo Longhi Vienna, from the Giva Group said: “Hydrogen can be a great ally to our Group. On one side, increasingly stringent measures on CO2 emissions coupled with our willingness to reduce the environmental impact from our production processes, move us towards finding a solution. On the other, the use of hydrogen could create a driving market for valves and actuators produced by Group’s subsidiaries. This project only marks the beginning of a path we will be involved in for years to come”.

The use of the hydrogen and natural gas blend did not require any plant modifications and had no impact either on the equipment used (industrial burners) or on the characteristics of the final heat-treated product.

The project’s potential in terms of environmental sustainability and economic competitiveness is significant. It is estimated that the permanent use of a 30% green hydrogen blend, fuelled by renewables, on the total gas consumed by the three GIVA Group’s steel forging plants for its industrial processes would lead to a significant reduction in CO2 emissions in the order of 15,000 tonnes per year, equivalent to 7,500 cars. It would consequently result into CO2 emissions savings amounting to approx. 800,000 euros per year (calculated on the current purchase of certificates) while ensuring the value and integrity of the steel forging manufacturing process and its long-term environmental sustainability.

Steel is also the material through which pipelines are made; these pipes will play a fundamental role in transporting hydrogen whereby supplying final customers.

The use of hydrogen in hard-to-abate industrial applications such as steelmaking will play a key role in achieving domestic and EU climate neutrality targets by 2050. Looking ahead, green hydrogen is the ideal solution for CO2-free steelmaking and processing.

Snam is committed to having its infrastructure hydrogen-ready for transporting increasing amounts of hydrogen and to promoting its use in high-potential industrial sectors, including the iron and steel industry.

China's transport investment reaches 3.48 trln yuan in 2020

BEIJING, May 19 (Xinhua) -- China's fixed-asset investment in the transport sector maintained steady growth last year, official data showed.

The total fixed-asset investment increased 7.1 percent year on year to nearly 3.48 trillion yuan (about 541.6 billion U.S. dollars) in 2020, according to the Ministry of Transport.

The growth rate was the highest in the last three years, said the ministry.

By the end of 2020, the operating mileage of China's railway network reached 146,000 km. The country had a total of 5.2 million km of highways, of which expressways represented 161,000 km.

There were 2,592 berths of 10,000-tonne-class or above and 241 certified civil airports throughout the country by the end of last year. ■

East China offshore wind farm connects to grid

HANGZHOU, May 17 (Xinhua) -- An offshore wind farm near the Zhoushan Islands, east China's Zhejiang Province, was commissioned and connected to the grid on Sunday.

The Daishan No. 4 wind farm has 54 wind turbines, with a total installed capacity of 234 megawatts. It is currently able to supply 618 million kilowatt-hours of electricity to the power grid a year, equivalent to the power created by burning 170,000 tonnes of coal, cutting emissions by 470,000 tonnes.

The wind farm is owned by the China General Nuclear Power Corporation, which will add two further wind farms near the Zhoushan Islands in the future, bringing its total wind power generation in the area to 1.44 billion kilowatt-hours once fully operational.

The green power is aimed at supporting the development of the oil and gas businesses in Zhoushan.

The Zhejiang Pilot Free Trade Zone in Zhoushan has been seeking cooperation with global oil and gas enterprises since its establishment in April 2017. ■

U.S., West need to know three realities about China: expert

The relationship between the United States and China in the coming years will greatly influence "the fate of the world," the expert said.

BEIJING, May 18 (Xinhua) -- "The United States and the West more broadly need to recognise three realities about China," Paul Sheard, research fellow at Harvard Kennedy Schools wrote in a recent article in the South China Morning Post.

The first reality is that China, "a giant economy," will only get bigger and more technologically advanced, wrote the former chief economist at S&P Global.

The second is that China's political, economic and social system that is different from the United States and the West has "unleashed its economic development potential in the past four decades and helped to lift many of its citizens out of poverty."

The third is that China views many issues differently from the United States, which reflects China's history, culture and values.

The relationship between the United States and China in the coming years will greatly influence "the fate of the world," he said.

"The proper path for the United States and China will require both countries to find ways to work closely together, and with others, to bolster and refashion the institutions that contribute to global security and prosperity and to solve myriad common global problems," Sheard wrote. ■

![]()

Powered by ![]() © Μaritimes 2019

© Μaritimes 2019