What is driving the summer rally of LNG spot charter rates?

No Fukushima like disasters, demolitions have only been a handful and deliveries have remained strong, yet, LNG spot charter rates have touched the highest mark since the summer of 2012. In this piece, we investigate what is driving the rally of the LNG spot charter market this summer.

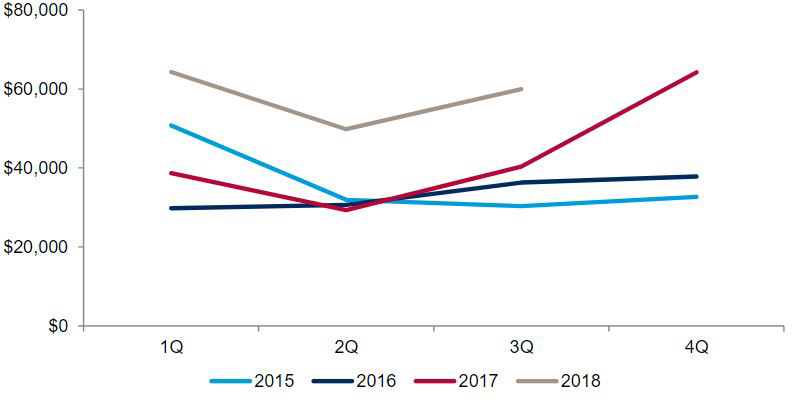

Despite growing availability of LNG carriers and traditionally low seasonal demand, LNG charter rates have remained firm throughout the summer of 2018. Spot charter rates strengthened throughout the second quarter of 2018 and are at their peak since 2012.

Shipowners with modern DFDE vessels chartered out their vessels at $60,000pd in 2Q18, which is about 50\% higher than the rates seen in the third quarter of 2017. At the end of June 2018, some vessels were reportedly fixed at $85,000pd – the level usually seen in the peak of winter, when LNG vessels are in high demand.

DFDE vessels spot rates ($ pd)

One of the major factors behind the recent rise in charter rates is the declining employability of older LNG carriers because of poor fuel efficiency, higher operating costs, less cargo-carrying capacity and high boil-off rates. Combined, these factors have effectively rendered a number of LNG carriers unemployable, hence squeezing the actual supply of vessels in the spot market.

With regard to fuel efficiency, bunker costs play a major role in decision-making. An old (30 year plus) steam turbine vessel can use as much as 215 tonnes of bunker fuel per day, while the average consumption of more modern steam turbine vessels is around 170 tonnes per day. On the other hand, modern DFDE LNG vessels burn only 140 tonnes of bunker, reducing the cost of bunker substantially. For instance, at current IFO bunker prices, a steam turbine vessel will burn $13,000pd of additional bunkers, compared with a modern DFDE ship.

Another issue, which makes modern DFDE vessels more attractive to charterers, is their ability to reinject the boil-off back into cargo tanks. This is a critical factor, especially on long-haul trades, where a substantial chunk of the cargo is either used as fuel, or simply flared on older ships.

Additionally, there are other issues relating to the maintenance, off-hire days, operational flexibility and modern navigation and signalling systems, which are superior on modern vessels. Older vessels also run the risk of frequent breakdowns, which charterers are not willing to take when they have options available.

Even at a time when charter rates are quite strong, there are at least 24 laid-up steam turbine vessels, which is about 11\% of the total steam turbine fleet. About 92\% of these vessels are younger than the average demolition age of LNG carriers over the last five years.

The current state of LNG vessel employability is challenging the conventional wisdom about the average economic life of LNG carriers, which used to be 35-40 years. If the current trends continue, ship financiers will start taking a more conservative view while financing second-hand assets in the LNG market.

To corroborate the popularity of modern ships, the chart below presents the spot market chartering trends in 2018 for LNG carriers. Year-to-date, 190 spot fixtures were reported; out of those only 59 were for steam turbine vessels – about 30\%.

Monthly spot fixtures and vessels employed

Our view

Drewry believes the current rally in charter rates will continue to sustain through to 2019. With increasing availability of modern vessels, owing to new deliveries and strong orderbook, the road ahead for older tonnage will be difficult. The traditional steam turbine ships will face tough competition from modern DFDE/TFDE carriers, and their future looks uncertain. The reason why shipowners are still holding onto these assets is that they foresee an acute shortage of vessels in 2019, when new liquefaction capacities start operating. That will be their last throw of the dice. If it does not work for them, then the only option for them will be to scrap those vessels.

Source: Drewry

Clean Arctic Alliance challenges Maersk on Arctic Shipping Fuel

“The Clean Arctic Alliance challenges Maersk to come clean on what fuel the Venta Maersk will use when crossing Arctic waters - and for Maersk, its customers, and its competitors to commit to never using the world’s dirtiest fuel - heavy fuel oil (HFO) - to power ships in the Arctic.”

“With this week’s news that the Arctic’s strongest sea ice has broken up twice this year, for the first time on record, using heavy fuel oil to power shipping in the Arctic not only increases the risk of oil spills, but also generates emissions of black carbon, which exacerbate the melting of both sea and glacier ice in the Arctic region. By taking the lead in the Arctic, Maersk could lead a vanguard of companies shipping commercial goods that move towards clean and renewable forms of propulsion for shipping worldwide.”

In April 2018, the International Maritime Organization’s Marine Environment Protection Committee agreed to move forward on consideration of a Arctic ban on heavy fuel oil. The meeting directed a sub-committee (PPR6) - which will meet in early 2019 - to develop a ban on heavy fuel oil use and carriage for use by ships in the Arctic, “on the basis of an assessment of the impacts” and “on an appropriate timescale”.

“It is time for international shipping companies to clean up their act by moving to cleaner fuels, while operating in sensitive and vulnerable regions of the world - for the sake of the Arctic, its people, its wildlife and indeed, for the whole planet.” concluded Prior.

Source: Clean Arctic Alliance

George Tsimis calls time at the American Club

George leaves SCB with the sincere thanks of his colleagues, and of the Club’s Board, for his notable contribution to the Club’s affairs over his years of service both in the United States and in Greece. Your Managers’ best wishes follow him as he moves to the next chapter of his career in the maritime world.

Donald R. Moore will succeed George as Global Claims Director. An average adjuster by training, with seagoing experience, Don is a well-known figure within both the Club’s membership and the shipping community at large.

He has a peerless background in the handling of marine insurance claims, having commanded a wide brief of P & I and related matters during his 25 years at SCB. Don will be supported in his new role by his fellow professionals within the management team, who will continue to dedicate themselves to the provision of unsurpassed Member service from the Managers’ offices across the world.

Once again, your Managers extend their very best wishes to George as he enters his new sphere of enterprise, and to Don for every success in discharging his new responsibilities.

Hellenic Marine Equipment Manufacturers & Exporters will participate at SMM Hamburg 2018

HEMEXPO Pavilion.

HEMEXPO will participate at SMM through the National Pavilion of Greece where Greek leading marine equipment manufacturers will present Smart Ship Solutions tailored to meet the needs of Shipowners and Shipyards.

Do not miss the opportunity to meet companies that have been equipping vessels for decades by investing in innovation, consistency, cost efficiency and of course top quality.

Hellenic Marine Equipment Manufacturers & Exporters will be more than happy to welcome you in Greek Pavilion.

Copenhagen Shipping Summit open for applications

|

The Interview: Ian Beveridge

IAN Beveridge has his hands full in one of the more complex jobs — or combination of two jobs — in shipping. But if there is any strain he seems to handle it lightly.

The longstanding chief executive of Bernhard Schulte, owner or co-owner of a fleet of about 90 ships across virtually all market sectors, Mr. Beveridge has also taken on the role of chief executive of Bernhard Schulte Shipmanagement since the start of 2018.

The move seems to acknowledge that this is an era of increasing competition and challenge in the third party shipmanagement business. But it also makes internal sense as the group seeks to reduce reliance on ship ownership.

“At Schulte Group level we want to put more effort and resources into the services business,” Mr. Beveridge tells Lloyd’s List. “Shipmanagement is a major part of that but we are also looking into other opportunities in the maritime sector.”

He began his career with the Hamburg-based group in 1991 as chief accountant for Eurasia Shipmanagement in Hong Kong and spent two years there before moving to Hamburg and switching to the shipowning side, becoming chief executive in 2001.

Eurasia was one of six separate group shipmanagers that were united in 2008 under the single brand of BSM. Today the company operates from 10 different locations around the world, the latest office being added in Mexico, but the number of sites is quadrupled if crewing and training centres are added.

Shipmanagement is suffering from “fierce competition”, says Mr. Beveridge. But he also believes that it is a moment of opportunity for those that will survive.

“For the third-party management sector there should be positive developments as quality demands and regulations increase, especially on emissions. More owners should say it makes sense to outsource to cope.” That includes an increasing number of end-users that are becoming interested in owning fleets.

Potential also stems from the fact that third party managers still have only “a relatively small part of the overall shipping pie” — estimates vary from about 13\% to 20\% at most.

Mr. Beveridge notes that shipowners vary widely in terms of their management models and that BSM has some major shipowners as clients, as well as prospective clients.

“But I would say that our growth is really more from smaller operators who do not have the resources to operate the vessels themselves,” he says.

“The strongest growth will probably be in Asia. At the moment that is where we are seeing quickest growth. In Asia small and mid-sized companies find it is a big investment for them to maintain people and systems suitable for international trading. It makes sense to outsource to someone like us who can do it at a cheaper price.”

Digitalisation, in many minds now closely allied to operational performance and energy efficiency in particular, is an area that can present particular challenges to smaller companies. As such it may often feature among a company’s reasons for outsourcing. BSM believes it is ahead of competitors in this area yet Mr. Beveridge is refreshingly down-to-earth about how far the company and the industry at large have come in this regard.

“Every second medium-sized shipping company is talking about the same thing, but it is still pretty rudimentary in the industry,” he says. “One of the issues in shipping is that there are so many people working on the same thing. Efforts are very fragmented and so we are trying to introduce more partners to work with us on some of these projects.”

A BSM-managed LNG carrier - ‘Getting LNG carriers is prestigious, but we need to grow in all segments’, says Ian Beveridge

BSM had collected “a lot of data” over the years. Mr. Beveridge admits that the company had “not done a lot” with it. But now the group is advancing much faster and has a stronger base for this than most in the business.

“We are maybe unique in having the capability on the software side and having a dedicated fleet performance division,” he says.

The strong focus on digitalisation can be traced back a decade to the merger of the separate shipmanagement companies, prior to which each independently had its own choice of software provider. BSM established a joint venture with a legacy software provider and later exercised an option to buy out the partner.

Sankar Ragavan, a former colleague at Eurasia, was brought back into the Schulte fold as chief executive of the software company. It was soon rebranded MariApps Marine Solutions and has become increasingly visible as a provider of integrated, innovative web-based and mobile-friendly solutions for shipmanagers and owners.

Initially MariApps was tasked with designing software for BSM’s proprietary use, but since then its focus has widened to offer its products competitively to third parties.

“There was a question whether, if this was a competitive advantage for us, did we really want to give it to customers and competitors? But we decided to do it to be able to further fund development and it has been exciting for the team to succeed in selling its software to other big names in the industry. It underlines that theirs is some of the best shipping software in the world,” says Mr. Beveridge.

MariApps already employs about 350 people and further indication of the importance of the software provider to BSM is that new premises for up to 1,500 people are under construction in Cochin, India as a step to ‘future-proof’ the company. A recent addition to the group’s shipmanagement activities was the launch of the Athens-based BSM Fleet Performance Centre as a centre of excellence aiming to maximise energy and operational efficiency for the benefit of vessels that BSM manages on behalf of owners all over the world. The choice of location was influenced by a move back to Athens by a Greek naval architect who had previously worked in the company’s Hamburg office. But, says Mr. Beveridge, Greece offered “good availability of personnel and shipping is in the DNA”.

Even though the centre is a recent initiative, BSM already looks on it as something to develop as a competitive advantage.

The company’s belief in developing specialised expertise extends to segments of the shipping markets. The most obvious is liquefied natural gas carriers, where BSM is a recognised leader ahead of other third-party managers. Earlier this year, it strengthened its presence in the sector by taking over Pronav, a specialised Hamburg-based LNG carrier manager. It has also entered the fledgling LNG bunkering sphere with one of the first LNG bunkering vessels being built under a strategic alliance with Babcock International.

However, the company also considers itself strong in managing very large bulk carriers, with more than half the worldwide valemax fleet of ore carriers under its stewardship, according to Mr. Beveridge. It has recently targeted the cruise business with the formation of Bernhard Schulte Cruise Services, with three cruiseships currently under management.

It also has its eye on becoming more active in managing offshore support and production vessels, although there the strategy might involve acquisition of a specialised firm to help give it more scale in that market segment.

Despite the emphasis on specialisation in areas where entry barriers tend to limit the competition, Mr. Beveridge says that BSM is not shirking ‘bread and butter’ shipmanagement. “It is a volume business,” he says.

“Shipmanagers constantly see vessels leaving the fleet. For BSM it is rare to lose customers on the basis of performance but there will always be a degree of structural churn, so we need to grow to cover the natural turnover in the fleet.

“It is nice to get LNG vessels. It is prestigious. But it does not feed a lot of mouths. We need to grow in all segments,” he says, identifying tankers as a likely source of relatively strong growth as charterers have more stringent standards and a top shipmanager will enhance a vessel’s chances of gaining approval.”

He foresees further consolidation in the shipmanagement sector, saying that smaller management outfits will struggle to remain viable. That said, he differentiates BSM’s position from that of some leading managers.

“The Schulte family has provided a very stable shareholding for generations. So, we are not forced to grow for the sake of growth, but if something interesting comes along we will look at it,” he says.

BSM has shown it is willing to acquire services companies in areas that it deems strategically important, but mega shipmanagement mergers are considered differently. “Integrating an acquisition is a resources-intensive exercise,” says Mr. Beveridge. “We are pretty wary about larger acquisitions.”

Original article below.

Interview by Lloyd's List Maritime Intelligence, August 2018

'Crazy' pricing and strong results put StealthGas back on screen for investors

|

| Harry Vafias |

by Andy Pierce

Published in GAS

A surprisingly strong second quarter result is set to put StealthGas on the map for new investors at a time when its market capitalization is almost $1bn below the value of its fleet.

Chief executive Harry Vafias believes shares in the Nasdaq-listed company are potentially the cheapest in the sector and today’s forecast-topping results should boost investor interest.

“The value of the company’s ships is $1.1bn and the market cap is $150m,” Vafias told TradeWinds in an interview today.

“If you think about it it's completely crazy. The people that do understand the maths and the strategy of the company can pick up some really cheap shares right now.”

StealthGas has a long-standing following from around five established institutional investors and counts Michael Dell among its major backers.

However, with the bad LPG market and a period of disappointing results, interest in the stock has fallen during the past few years.

“We are by far the cheapest company out there by any financial metric,” Vafias said.

“For those people who want to invest in LPG and US listed companies, we are probably the cheapest one out there and the one with the least risk because of the valuation and the low leverage.

“From now on, from these second quarter results that caught many people by surprise, I think we are going to get calls from newcomers who believe in gas and believe in green energy and want to get in while the share is so cheap,” Vafias said.

|

“We have been in a nice conjunction where earnings are going up and costs are going down, which created this very nice result,” Vafias said.

StealthGas saw second quarter revenue climb by 10\% to $43.4m. It has also been active in the sale and purchase market with the disposal of seven ships for close to $30m in cash this year.

The company has taken delivery of all 26 vessels from a vast newbuilding programme while keeping debt levels below 40\%.

“We took them at a time the market was really bad and the financing market was really bad,” Vafias said.

“We took them in without any hiccups and problems. That showed the strength of the company’s reputation and the balance sheet.”

Perceiving “Beaching” method in Ship Recycling by Dr.Anand Hiremath & Michail Matthaiakis , GMS

|

The decision makers in the European Union has became apprehensive with the word “beaching” due to the lobbying of some specific groups in the past twelve years .

Beaching :

It is just a process of bringing a vessel near the shore (i.e. near the recycling yard) using the vessel’s own powerwhile taking advantage of the tide. It is widely known that beaching takes place in India and landing takes place in Turkey.

The question which arises is how the Landing method employed in Turkey is different from the method used in India? Practically, both are the same. One will be surprised to know that landing takes place even in the United States (Texas).That means,the process itself is not a problem. The actual problem starts on how the vessel is cut at a yard, after the beaching(or landing, or floating) of the vessel.

But what is the reason so many yard owners in Alang decided to make these significant investments in infrastructure and working standards?

In 2009, the adaptation of theHong Kong International Convention for the safe and environmentally sound recycling of ships, which was then the only International Convention on ship recycling, was the driving force for all the significant upgrades that took place in the ship recycling yards in India.In addition, the Classification Societies started to show interest in auditing yards against the HKC standards.

On top of the above, few ship owners started visiting several recycling yards in South Asiato witness if thehigh recycling standards were in accordance with the HKC. As a result, in the end of 2015, the first 4recycling yards in India were certified by ClassNK with a Statement of Compliance(SOC) with the HKC. Soon, more yards joined this virtuous circle with the result that now the majority of Alang works in line with the Hong Kong Convention.

On the other hand, though, while Turkey is claimed to be a green recycling destination, it will be surprizing to mention that only 8 yards out of 22 in total, received a SOC with the HKC from the Classification Societies.

As stated earlier, In India, 70 yards have been certified by various Classification Societies with Statements of Compliance (SOC) with the requirements of the HKC out of the total 120 working yards. The capacity of these 70 yards is around 65\% of the total LDT capacity of Alang, and as that is nearly 4.5 M ton per year, the SOC certified yards have the capacity to handle nearly 3 M LDT per year.

The above,clearly shows the amount of time, effort and money that has been invested by a significant proportion of the yard owners in Alang, to meet the International recycling standards.

It should be noted that the yards both in Turkey and India are certified by the Classification Societies against the same HKC standards. But even with these high recycling standards in India, currently, only 15 yards are recycling vessels which demand a SOC with the HKC out of the 70 yards in total, which hold a SOC with the HKC.

Yard Owners disgruntled

Although, these yards offer quality recycling services, the majority of owners so far are not interested in quality/green recycling. There have been questions in international conferences recently on when will 100\% of the recycling yards in Alang be HKC certified. However the more pressing question that yard owners are asking now in Alang is “Why do we have to achieve 100\% certification when the existing SOC yards are not getting enough vessels requiring and paying for HKC standards for recycling?”

What is important to underline is that even though the situation is tough, most of the owners of SOC yards are continuing to invest to further to upgrade their yards to meet the EU Ship Recycling Regulation (EUSRR) standards, in an effort to be included in the list of the EU-approved yards. Though, only 9 yards (with cumulative recycling capacity of 0.6 M LDT) applied two years ago for inclusion in the EU-List, the approval of these 9 applications from India, will certainly boost the confidence of yard owners and the bar of recycling standards will go further high.

Those Indian yards should be included in the EU-approved list as they hold a certificate from an Independent Verifier in accordance with the requirements of the European Union’s Ship Recycling Regulation (EUSRR) 1257/2013. Upon the inclusion, the other yards in India will wish to do the same by upgrading their facilities and as a result, Alang will be completely transformed.

Similarly, Bangladesh and Pakistan will be significantly improved as Alang will become the force of change for these recycling locations as well. In case that the yards that have applied for inclusion to the EU list are not approved by the European Commission, then, all the investments in quality recycling will dry up, making those who believed in the green future of ship recycling in the sub-continent, look foolish.

It should be recalled that the objective behind the EUSRR was also to catalyze the early ratification of the HKC. The decision makers should take a pragmatic approach to fullfil the objective than hindering the growth of quality recycling in South Asian Countries – which recyle more than 85\% of the total end-of-life vessels per year.

www.steel-360.com

RMI Establishes Worldwide Gas Team

This new group is a response to the recent growth, both in number and vessel type, in the transportation and processing of liquified gases.

Due to the technological developments taking place in gas shipping, new international regulations have been put in place regarding the design and construction of gas ships and equipment in order to ensure the safety of the vessel, crew, and the marine environment. In any marine sector, new regulatory requirements can be complex and expensive for owners to adhere to. This can be especially true in a space like gas shipping, where new technological developments create an environment that is constantly evolving, and owners must be prepared to respond to these changes with costly updates to their vessels.

The Team is a comprehensive group, made up of experts chosen for their ability to provide guidance from inspection and registration to technical issues and regulatory challenges, and is located worldwide. The Team is headed by Eric Linsner, IRI’s LNG/LPG Specialist who has extensive experience in LNG design and operations. Other key members of the Team include:

- Jason Clifton-Samuel, Safety & Technical Manager, London

- Jasbir Jaspal, Senior Maritime Advisor, Reston

- Kevin Cook, Maritime Consultant, Reston

- Warren Kedenburg, LNG Advisor, Kobe

- Steven Garcia, Flag State Specialist, Houston

- J. Person, Flag State Inspector, London

- Joseph McKeown, Vice President, Technical & Marine Safety

This level of expertise in the gas carrier sector is unique to the RMI Registry and demonstrates its dedication to providing the resources that owners and operators require. The RMI Registry is committed to leading the way as a technologically capable and qualified registry and is excited to grow with its owners and operators in this expanding field.

30 July 2018News category: Industry Insight, Regulatory

Greek tanker feared hijacked in Gulf of Guinea

|

Product tanker PANTELENA, IMO 9321469, dwt 10726, built 2006, flag Panama, manager LOTUS SHIPPING CO. LTD, Greece.

maritimebulletin.net

![]()

Powered by ![]() © Μaritimes 2019

© Μaritimes 2019