Unlocking the value of applying blockchain technology to maritime.

Earlier this week LR announced the launch of its prototype blockchain-enabled Class register – the first demonstrator that can register ships into Class using blockchain technology. Luis Benito, LR Innovation & Co-creation Director Marine & Offshore commented: “We have subsequently identified that the value this could deliver could be extended to benefit all stakeholders, starting with the shipbuilder.”

He continued, “We are delighted that HHI is joining us on this innovation journey. We see this as a potential new way to manage the entire multi-stakeholder chain related to shipbuilding, in a way that it will become more effective and efficient for all involved, setting a new best practice standard in our industry.”

Hong-Ryeul Ryu, Vice President at HHI commented: “We are glad to explore blockchain technology with LR to find out the value for new building. We expect blockchain project enables us to ensure that our project planning and initial designing work are more efficient. All relevant information is traceable, demonstrable, transparent, recorded in a way therefore all parties can trust that activities happened in the prescribed way and the outcome of such activity conforms to requirements of the contract.”

lr.org

GoodBulk entered into a new credit facility with ING Bank

On 4 September 2018 the Company took delivery of the M/V Aquasalwador, a 2012 built Capesize vessel of 180,012 dwt built by Daehan, KR. The Company entered into an agreement to purchase the vessel on 27 July 2018 for consideration of $34.7 million which was financed by a combination of cash on hand and $24.5 million of availability under the ING Bank credit facility. Consistent with Company policy, the LIBOR rate was fixed at 2.935\% for the duration of the loan.

On 5 September the Board of Directors declared a dividend of $0.06 per common share to shareholders of record as of 19 September 2018 and payable on 3 October 2018.

On 5 September 2018 GoodBulk entered into an investment agreement pursuant to which the Company will issue 572,738 new common shares to an unaffiliated investor at a subscription price of $17.46 per new common share, raising gross proceeds of approximately $10.0 million in total. The share issuance is expected to be completed by 7 September 2018. Following the issuance of the new common shares, GoodBulk will have 30,116,458 common shares outstanding.

Following completion of the announced vessels acquisitions and dispositions the Company’s net debt to gross asset value is expected to remain below the targeted 30\%.

About GoodBulk Ltd.

GoodBulk, incorporated in Bermuda and headquartered in Monaco, is an owner and operator of dry bulk vessels formed in October 2016 for the purpose of owning high quality second hand dry bulk vessels between 50,000–210,000 DWT. Upon completion of the announced acquisitions and dispositions, GoodBulk will control a fleet of twenty-six dry bulk vessels, including twenty-four Capesize vessels, one Panamax vessel, and one Supramax vessel. Designed to provide an efficient company for investors to access the dry bulk market, all vessels are externally managed by C Transport Maritime S.A.M. a leading third-party manager of dry bulk vessels. GoodBulk is listed on the Norwegian OTC market under the symbol “BULK.”

goodbulk.com

Setting the standards for the future of shipping: DNV GL releases autonomous and remotely operated ship guideline

|

| The first commercial autonomous vessels are due to launch in the next several years. |

“A new set of sensor, connectivity, analysis, and control functions in maritime technologies is laying the foundation for remote and autonomous operations in shipping,” says Knut Ørbeck-Nilssen, CEO of DNV GL – Maritime. “Increased automation, whether in the form of decision support, remote operation, or autonomy, has the potential to improve the safety, efficiency and environmental performance of shipping. To reach this potential, the industry needs a robust set of standards that enables new systems to reach the market and ensure that these technologies are safely implemented.”

The guideline covers new operational concepts that do not fit within existing regulations, and technologies that control functions that would normally be performed by humans. In terms of new operational concepts, the guideline helps those who would like to implement new concepts with a process towards obtaining approval under the alternative design requirements by the flag state. For novel technologies, suppliers can use the guideline to obtain an approval in principle.

The guideline covers navigation, vessel engineering, remote control centres, and communications. Particular emphasis is given in two key areas that emerge from the reliance of autonomous and remote concepts on software and communications systems: cyber-security and software testing. Both the concept qualification process and the technology qualification process include cyber security aspects in the risk analysis. Not only the systems themselves, but the associated infrastructure and network components, servers, operator stations, and other endpoints should all take cyber security into account, incorporating multiple layers of defence where possible. In terms of software, quality assurance of software-based systems is essential, and well established development processes and a multifaceted end-product testing strategy should be used to ensure safe operation.

“This is a first step in the process to fully realise these technologies,” says Knut Ørbeck-Nilssen. “But we continue to develop experience from several projects currently underway. In some areas, such as navigation systems and engineering functions we can already offer technical guidance based on our current class rules and as we progress new guides and rules will follow.”

DNV GL media hub for SMM: www.dnvgl.com/press18

About DNV GL:

DNV GL is a global quality assurance and risk management company. Driven by our purpose of safeguarding life, property and the environment, we enable our customers to advance the safety and sustainability of their business. Operating in more than 100 countries, our professionals are dedicated to helping customers in the maritime, oil & gas, power and renewables and other industries to make the world safer, smarter and greener

About DNV GL – Maritime

DNV GL is the world’s leading classification society and a recognized advisor for the maritime industry. We enhance safety, quality, energy efficiency and environmental performance of the global shipping industry – across all vessel types and offshore structures. We invest heavily in research and development to find solutions, together with the industry, that address strategic, operational or regulatory challenges. For more information visit www.dnvgl.com/maritime

Transocean Ltd. Announces Agreement to Acquire Ocean Rig

- Adds nine high-specification ultra-deepwater drillships, two harsh environment semisubmersibles, and two high-specification ultra-deepwater drillships currently under construction;

- Results in a combined fleet of 57 floaters, with 17 of the top 50 and 31 of the top 100 ultra-deepwater drillships in the industry(1);

- Enhances Transocean’s exposure to, and ability to capitalize on, the ultra-deepwater market recovery;

- Increases Transocean’s industry-leading contract backlog by $743 million for a combined total of $12.5 billion, at an average dayrate of $413,000;

- Expected annual cost synergies of approximately $70 million;

- The transaction has been unanimously approved by the board of directors of each company; and

- The top four Ocean Rig shareholders (representing approximately 48\% of Ocean Rig’s outstanding shares), all of Ocean Rig’s directors that own shares of Ocean Rig, and Transocean’s third largest shareholder, Perestroika (Cyprus) Ltd., controlled by current Transocean board member, have executed voting and support agreements.

|

The transaction consideration is comprised of 1.6128 newly issued shares of Transocean plus $12.75 in cash for each share of Ocean Rig’s common stock, for a total implied value of $32.28 per Ocean Rig share, based on the closing price on August 31, 2018. This represents a 20.4\% premium to Ocean Rig’s ten-day volume weighted average share price. The transaction has been unanimously approved by the board of directors of each company.

Transocean intends to fund the cash portion of the transaction consideration through a combination of cash on hand and fully committed financing provided by Citi. The merger is not subject to any financing condition.

Upon completion of the merger, Transocean’s and Ocean Rig’s shareholders will own approximately 79\% and approximately 21\%, respectively, of the combined company.

Ocean Rig’s fleet is comprised of nine high-specification ultra-deepwater drillships and two harsh environment semisubmersibles. Additionally, its fleet includes two high-specification ultra-deepwater drillships currently under construction at Samsung Heavy Industries with favorable shipyard financing terms. These two newbuilds are expected to be delivered in the third quarter of 2019 and the third quarter of 2020, respectively.

“The proposed acquisition of Ocean Rig provides us with a unique opportunity to continue enhancing our fleet of ultra-deepwater and harsh environment floaters, without compromising our liquidity or overall balance sheet flexibility,” said Transocean’s President and Chief Executive Officer, Jeremy Thigpen. “The combination of constructive and stable oil prices over the last several quarters, stream-lined offshore project costs, and undeniable reserve replacement challenges has driven a material increase in offshore contracting activity. As such, adding Ocean Rig’s premium assets to our industry-leading fleet provides us with an increased number of the modern and highly efficient ultra-deepwater drillships preferred by our customers, and better positions us to capitalize on what, we believe, is an imminent recovery in the ultra-deepwater market.”

Thigpen continued, “This combination with Ocean Rig further strengthens our relationships with strategic customers, while expanding our presence in the key markets of Brazil, West Africa and Norway. It also enables us to reduce our cost per active rig, as we believe that we can efficiently merge the Ocean Rig operations into our existing structure with limited incremental shore-based expense. Further, we are confident that we can realize meaningful synergies through our OEM agreements, our overall approach to maintenance and our fleet-wide insurance coverage, among other opportunities.”

Thigpen concluded, “Including the five rigs under construction, and considering the two additional rigs that we have recently decided to recycle, Transocean’s pro forma fleet will be comprised of 57 floaters, including many of the most technically capable ultra-deepwater floaters, and harsh environment semisubmersibles in the industry. With this unparalleled fleet, the offshore drilling industry’s largest and most profitable backlog totaling $12.5 billion, and approximately $3.7 billion in liquidity, we are well-equipped for the market recovery.”

Pankaj Khanna, President and Chief Executive Officer of Ocean Rig UDW Inc. commented: "This strategic combination of Ocean Rig and Transocean creates a world-class fleet perfectly positioned for the market recovery while reducing fragmentation that currently exists in offshore drilling. By adding our high-specification floaters to Transocean's industry-leading fleet, the combined company will have the offshore industry’s largest and most technically capable fleet of ultra-deepwater and harsh environment floaters. Upon consummation, this transaction will be of significant benefit to the stakeholders of both companies."

No changes to Transocean’s board of directors, executive management team, or corporate structure are anticipated as a result of the acquisition. The Company will remain headquartered in Steinhausen, Switzerland, with significant operating presence in Houston, Texas, Aberdeen, Scotland and Stavanger, Norway.

The transaction, which is expected to be completed during the first quarter of 2019, is subject to the approval of both Transocean and Ocean Rig shareholders and the satisfaction of customary closing conditions, including applicable regulatory approvals. The merger is not subject to any financing condition.

Also, consistent with the Company’s strategy of recycling less competitive rigs, Transocean will retire two of its floaters, the ultra-deepwater drillship C.R. Luigs and the midwater floater Songa Delta. The rigs will be classified as held for sale and will be recycled in an environmentally responsible manner. Both floaters are currently stacked. Transocean anticipates re-ranking the combined fleet, which may result in additional rigs being recycled.

- Per Transocean’s internal rig ranking model

Advisors

Citi is acting as exclusive financial advisor to Transocean, and King & Spalding LLP is acting as legal advisor to Transocean with respect to U.S. law.

Credit Suisse Securities (USA) LLC is acting as financial advisor to Ocean Rig. Seward & Kissel LLP is acting as legal advisor to Ocean Rig with respect to U.S. law.

Conference Call Information

Transocean will conduct a teleconference call to discuss this transaction at 8:30 a.m. EDT, 2:30 p.m. CEST, on Tuesday, September 4, 2018. To participate, dial +1 323-794-2597 and refer to confirmation code 2404736 approximately five to 10 minutes prior to the scheduled start time of the call.

The teleconference will be simulcast in a listen-only mode over the internet and can be accessed at: www.deepwater.com, by selecting Investors, News, and Webcasts. Supplemental materials that may be referenced during the teleconference will be posted to Transocean’s website and can be found on the Investor Relations home page.

A replay of the conference call will be available after 11:30am EDT, 5:30 p.m. CEST, on September 4, 2018. The replay, which will be archived for approximately 30 days, can be accessed at +1 719-457-0820 passcode 2404736 and PIN 1152. The replay will also be available on the company’s website.

About Transocean

Transocean is a leading international provider of offshore contract drilling services for oil and gas wells. The company specializes in technically demanding sectors of the global offshore drilling business with a particular focus on ultra-deepwater and harsh environment drilling services, and believes that it operates one of the most versatile offshore drilling fleets in the world.

Transocean owns or has partial ownership interests in, and operates a fleet of 41 mobile offshore drilling units consisting of 23 ultra-deepwater floaters, 12 harsh environment floaters, two deepwater floaters and four midwater floaters. In addition, Transocean is constructing two ultra-deepwater drillships; and one harsh environment semisubmersible in which the company has a 33 percent interest. The company also operates one high-specification jackup that was under a drilling contract when the rig was sold, and the company will continue to operate the jackup until completion or novation of the drilling contract.

For more information about Transocean, please visit: www.deepwater.com.

About Ocean Rig

Ocean Rig is an international offshore drilling contractor providing oilfield services for offshore oil and gas exploration, development and production drilling, and specializing in the ultra-deepwater and harsh environment segment of the offshore drilling industry.

Ocean Rig’s common stock is listed on the NASDAQ Global Select Market where it trades under the symbol “ORIG.”

For more information about Ocean Rig, please visit: www.ocean-rig.com.

Resolve completes the heaviest salvage lift in the Americas

|

| db1 wreck remova gulf lifted on submersable barge heavy lift |

From the outset, a one-piece lift of the DB1 represented the most environmentally friendly removal method compared with other proposals to section the vessel in pieces but implementing such a plan was extremely challenging and required Resolve’s specialized equipment and expertise to complete safely.

The 350 ft x 100 ft derrick barge DB1 sank 30 miles offshore in the Gulf of Mexico on October 22nd, 2017, when adverse weather caused it to drag anchors and contact the offshore platform that the DB1 was engaged in removing. Multiple compartments were breached and the DB1 came to rest on the sea floor and on top of the platform jacket structure.

For the removal project, assets were mobilized from Resolve’s salvage bases around the world including from Singapore, Ft Lauderdale, and Mobile. Key project assets included Resolve’s patented heave-compensated chain puller lift system, deployed from the Resolve CONQUEST MB1 1400 ton derrick barge and RMG 302 crane barge.

Resolve mobilized a 40-person team of salvage experts and divers to support the 24/7 operation and engaged numerous support vessels and resources from the region.

After extensive preparations including the installation of heavy rigging under the DB1, the lifting gear was connected and the DB1 was steadily raised to the surface between the MB1 and RMG 302 with 6000 tons of lift force – an industry first! Resolve then mobilized the BOABARGE 29, a semi-submersible barge to the offshore site to receive the DB1.

On arrival, the BOABARGE 29 submerged to the seafloor and the DB1 was winched over the top with inches of margin. The submersible barge was then raised with the DB1 safely aboard and then towed to Brownsville, Texas, for DB1’s dismantling and recycling.

“Raising the DB1 was an extraordinary engineering and operations challenge and I am extremely proud of the entire project team.” stated Andy Butts, Resolve’s Salvage Master.

“Special recognition is extended to our key support partners including Conquest Offshore, BOA Barges, Offshore Towing, Offshore Marine Contractors, Smith Maritime, Tradewinds Towing, and Oceaneering. We also thank the owner team of Turnkey Offshore Project Solutions, QBE Insurance and London Offshore Consultants for choosing Resolve and for facilitating a smooth operation.”

ResolveMarine.com

A new perspective on alternative fuels: DNV GL launches Alternative Fuels Insight (AFI) platform

|

| DNV GL’s new AFI platform offers a comprehensive and continually updated overview of alternative fuel projects, bunkering infrastructure, suppliers, and technologies. |

The AFI platform builds on DNV GL’s well received LNGi portal, but with an expanded focus that covers LNG, LPG and methanol, as well as emission reducing technologies such as scrubbers and batteries. The platform consolidates a wealth of detailed technical information on these fuels and technologies, including their bunkering infrastructure, and examines their capabilities and limitations, as well as giving practical insights into their implementation and operation. With much of the information free to access, the AFI platform is a valuable resource for owners and operators needing to research and keep up to date in this rapidly moving sector. In addition, through the Fuel Finder tool shipowners and charterers can submit requests for bunkering, specifying fuel type, location, volume and from which date they would like to bunker. DNV GL validates these requests and then makes them available to suppliers.

“The Fuel Finder tool makes it easy for owners and charterers to see how their decision to move to an alternative fuel could work out in practice,” says Martin Wold, head of the AFI platform at DNV GL – Maritime. “With one request, they can see how the operational profile of their projects match the capability of multiple suppliers. We have also been working with several leading suppliers and equipment makers who have signed on as supporters of AFI and we have opened the platform to user contributions, so that we continually expand the platform by adding bunkering and infrastructure projects.”

With interactive maps and data visualizations, it is easy for users to see where infrastructure already exists or will shortly be developed, alongside the growing alternative fuelled fleet. And new tools let users dig deeper into the data to analyse trends and screen the feasibility of their alternative fuel projects based on based on CAPEX, OPEX, and fuel prices.

You can find out more about the AFI platform and sign up at www.dnvgl.com/afi

DNV GL media hub for SMM: www.dnvgl.com/press18

About DNV GL:

DNV GL is a global quality assurance and risk management company. Driven by our purpose of safeguarding life, property and the environment, we enable our customers to advance the safety and sustainability of their business. Operating in more than 100 countries, our professionals are dedicated to helping customers in the maritime, oil & gas, power and renewables and other industries to make the world safer, smarter and greener

About DNV GL – Maritime

DNV GL is the world’s leading classification society and a recognized advisor for the maritime industry. We enhance safety, quality, energy efficiency and environmental performance of the global shipping industry – across all vessel types and offshore structures. We invest heavily in research and development to find solutions, together with the industry, that address strategic, operational or regulatory challenges. For more information visit www.dnvgl.com/maritime

DNV GL at SMM 2018: DNV GL and Huangpu Wenchong: 200 ships and still going strong

|

| The contract signing at the SMM Trade Fair in Hamburg. Left: Mr Li Xi, Vice President of CSSC Huangpu Wenchong Shipbuilding Company Ltd. Right: Norbert Kray, Senior Vice President and Regional Manager for Greater China at DNV GL - Maritime. |

“The close relationship and comfortable communication between the two companies has enhanced HPWS’s position in shipbuilding. Building high quality vessels that are more efficient and greener is at the core of our strategy, and DNV GL’s industry expertise, technical support and services have proven a great match. This milestone underscores the mutual benefit of our partnership, and gives us encouragement to further strengthen our relationship,” says Chairman Chen Zhongqian of Huangpu Wenchong Shipyard.

“DNV GL’s cooperation with HPWS has been long and fruitful, and the 200th ship milestone is proof of this,” says Norbert Kray, Senior Vice President and Regional Manager for Greater China in DNV GL. “We have been through many developments together, and we have maintained our trusting relationship through the good and the tough times.”

DNV GL has also assisted HPWS in their progress toward building new and more sophisticated ship types. “DNV GL’s technological expertise and broad experience has been invaluable to HPWS when building more advanced vessels,” says HPWS Chairman Chen Zhongqian. “There are many challenges and new technologies to be considered when moving into different vessel types, and we have shortened development time considerably by leveraging DNV GL’s technology.”

HWPS and DNV GL will also sign a strategic cooperation agreement at SMM 2018. According to the agreement, both parties will work to further strengthen their collaboration on ship design and shipbuilding. DNV GL and HWPS aim to contribute to the future development of shipbuilding technology and markets, and agree that a comprehensive cooperation mechanism will help to strengthen communication and cooperation from both companies at all levels.

While feeder container ships will continue to be HPWS’s key product, the shipyard plans to explore other markets and increase investment in research and development to expand their strategic ship types, including 3,000 and 3,500 TEU feeder container ships, LNG/diesel dual fuel feeder container ships, more intelligent and electric powered ships, dredgers, multi-purpose heavy lift ships, and fishing vessels.

“Our relationship to HPWS has grown and developed over more than 20 years,” sums up Norbert Kray. “Now we look forward to helping them branch out into new ship types in the future.”

DNV GL media hub for SMM: www.dnvgl.com/press18

Ship number 200

The 200th DNV GL classed vessel from Huangpu-Wenchong, a 2,750 TEU container feeder, features many of the most modern technologies for efficiency and emissions reduction, including:

- DNV GL ECO-Insight vessel performance monitoring system to ensure efficient operation and monitoring

- ECO Hull design optimized for class-leading fuel efficiency

- Innovative bow design and ESD fittings to improve energy

- Breakbulk capacity integrated into container ship design

- Navigation systems with network ability will allow remote monitoring of the vessel’s navigation and machinery operations in real time in the future

- Enthalpy Wheel Heat Recovery HVAC system

- VFD Controlled Main Cooling Sea water system

- Exhaust Gas heat recovery from Auxiliary Engines

- LED lighting throughout the vessel

About DNV GL:

DNV GL is a global quality assurance and risk management company. Driven by our purpose of safeguarding life, property and the environment, we enable our customers to advance the safety and sustainability of their business. Operating in more than 100 countries, our professionals are dedicated to helping customers in the maritime, oil & gas, power and renewables and other industries to make the world safer, smarter and greener

About DNV GL – Maritime

DNV GL is the world’s leading classification society and a recognized advisor for the maritime industry. We enhance safety, quality, energy efficiency and environmental performance of the global shipping industry – across all vessel types and offshore structures. We invest heavily in research and development to find solutions, together with the industry, that address strategic, operational or regulatory challenges. For more information visit www.dnvgl.com/maritime

Container Market: Premium of spot rates to agreed US annual contract box rates has risen

Peak season to date has not been as bullish as some market participants expected. There have been box rate increases throughout August and this is expected to continue into September. However, there are some fundamental issues causing uncertainty within the container industry. The first one is the new larger TEU vessels deliveries continue to create surplus capacity for carriers, especially within the North Europe market. The knock-on effect is that this has put the carriers in a weaker negotiating position for spot box rates. A freight forwarder said that “logistics providers will often book a few carriers for the same container cargoes and fail all but one at the last moment, a thing only possible when carriers are in a weak position. So, they have to pick up the bills for empty space on vessels.”

Another issue is that the premium of spot rates to agreed US annual contract box rates has risen to levels that are making end- users question the reasoning behind them. “Customers are looking at the yearly contracts which have numbers that are twice lower than on spot and it’s hard to understand for them why they pay so much. And explaining that capacity is full and it’s a peak month and that’s where the spot market is now may be complicated,” a carrier said. Some carriers have made first-half losses so they need to recoup these during the peak season otherwise the end of year results could be disastrous.

The US trade war is still causing uncertainty on box rates after October 1. Carriers are especially concerned that the end-users have front-loaded their supply-chain programs to avoid any additional items being added to the banned lists. Finishing on a positive note for carriers, they are expecting to see increases of $100-$300 per FEU on September 1 box rates on the majority of the main head-haul routes, unless something unexpected happens.

NORTH AMERICAN MARKET FOCUS

On August 1, there was a 25\% increase on the PCR13, North Asia to West Coast North America, route to $2,000/FEU, carriers then managed another price hike to $2,200/FEU, August 8 before slowly reducing to $2,100/FEU, August 20 where it has remained as of August 24. Similar box rate increases occurred on the East Coast on August 1 and 8 to $3,000/FEU and $3,200/FEU respectively. The East Coast box rates remain between $3,050/FEU and $3,300/FEU but on August 16 PCR5 fell to $3,150/FEU. September 1 carriers are hoping they can achieve a modest increase of $100-$200/FEU. September cargo allocation percentages looking supported but this is being offset by the October end of the peak season looming on the horizon.

North American Platts Bunker Charge

August 1 PBC13, North Asia to West Coast North America closed at $329.55/FEU before steadily decreasing to $322.22/FEU on August 15 before rebounding to $331.88/FEU on August 23. The North Asia to East Coast North America bunker charge, PBC5, followed a similar trend except more starkly. PBC5 went to $532.56/FEU on August 23, from $533.05/FEU, August 1 the bottom of the trough was $17 less on August 15 at $514.46/FEU.

UK AND NORTH CONTINENT MARKET FOCUS

Since July 1 rates have fluctuated between $1,450/FEU and $1,550/FEU as of August 24. This is in part due to the extra capacity issue. On the one hand it is positive that the box rates are more stable for carriers but the North Europe head-haul routes have not seen the $400 to $600 per FEU increases that occurred across the Atlantic. September 1 is thought to bring box rates into the realms of $1,700/FEU and $1,800/ FEU. One freight forwarder said “Would expect as September gets going rates to drop back down to $1,500/FEU level.” The main reason for this is the peak season is drawing to an end.

North Continent Platts Bunker Charge

August bunker charges have been more stable this month fluctuating between $295.04 on August 1 and $292.86 on August 23. On August 16 PBC1 was at its lowest, $285.23. Bunker charges seem to be continuing its upward trajectory with carriers still negotiating new terms with their customers.

BUNKER TRENDS

In August the biggest story hitting the marine fuels industry was the ongoing fallout from the contaminated bunker fuel first spotted in Houston earlier this year and since exported across the world. More than 100 vessels are now thought to have been damaged by the phenolic compound contamination, and the problem has had consequences for bunker import flows as far away as Singapore.

Further developments have been announced in shipping companies’ moves to comply with the International Maritime Organization’s lower bunker sulfur limit in 2020. Hapag-Lloyd said it is preparing to test emissions-cleaning scrubber equipment on two of its vessels, and is converting a third to run on LNG. And Maersk has announced a joint initiative with storage operator Vopak to launch a 0.5\% sulfur bunker facility in Rotterdam, and told S&P Global Platts it may produce its own blend of 0.5\% sulfur fuel there rather than buying finished product from the refiners. Meanwhile Shell’s marine fuels unit has said it now has test samples of its 0.5\% sulfur fuel blend ready for shipowners to try out in Rotterdam, Singapore and New Orleans.

Finally, bunker supplier Aegean Marine Petroleum has announced energy and commodity group Mercuria has become its sole lender under its US and global revolving credit facilities. Mercuria agreed to provide Aegean a $1 billion trade finance facility in July intended to support its existing credit facilities, after Aegean earlier in the year failed to meet a deadline to file its 2017 annual report to US regulators.

Source: S&P Global Platts (Senior Editor, Andrew Scorer)

Top Performing German Owners Since SMM 2017

By comparing the every German owners' fleet value on the first day of SMM 2017 against today's fleet value, we can see the German fleets which have grown the most in value and in total number of owned vessels.

|

Oldendorff Carriers tops the list by growing their fleet by 22 vessels and increasing their total value by 716 million USD. Today their total fleet comprises 109 vessels worth 2.6 billion USD.

In second place is MPC Containships, adding 52 vessels to their owned fleet in 12 months. An impressive addition, considering during SMM 2017 MPC fleet owned 14 vessels worth 95.8 million USD. Today MPC Containerships own 66 vessels worth 631 million USD.

Source: VesselsValue

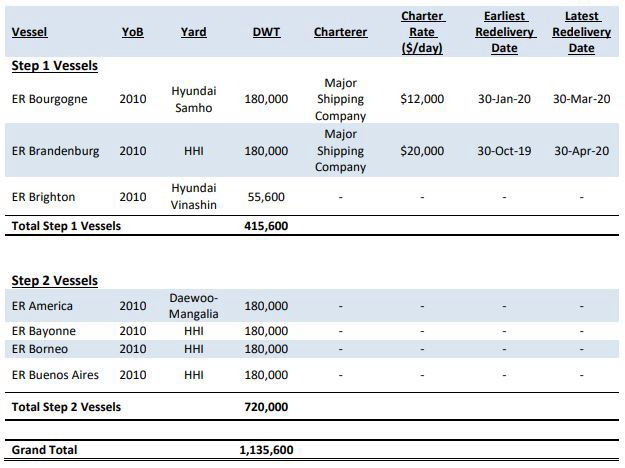

Star Bulk agrees to acquire up to seven dry bulk vessels from E.R. Capital Holding

that it has entered into an en bloc definitive agreement with entities affiliated with E.R. Capital Holding GmbH & Cie. KG (“E.R.” or “Sellers” ), pursuant to which the Company will acquire three (3) firm operating dry bulk vessels (the “Step 1 Vessels”) within 2018 ( the “Step 1 Acquisition”), and four (4) optional operating dry bulk vessels (the “Step 2 Vessels”) in 2019 (the “Step 2 Acquisition”), and ogether the “Vessels”. Subject to agreeing a three party novation agreement with charterers and E.R., any charterparties existing at the time of the deliveries of each of the Vessels shall be novated to Star Bulk.

The Step 1 Vessels will be acquired for an aggregate of approximately 1.34 million common shares of Star Bulk (the “Step 1 Consideration Shares”) and $41.70 million in cash. The number of Step 1 Consideration Shares to be issued is subject to adjustments for the Company’s cash, debt and remaining capital expenditures as of one business day prior to the delivery date of each of the Step 1 Vessels. The cash portion of the consideration for Step 1 Vessels will be financed through proceeds of a new five-year term loan of $41.0 million from a major European commercial bank. Following the consummation of the Step 1 Acquisition, E.R. will own approximately 1.45\% of SBLK common shares.

In relation to the Step 2 Vessels, the Sellers have granted four call options to the Company for an aggregate exercise price of $115.39 million or $28.85 million per Step 2 Vessel (the “Call Options”), exercisable on April 1st 2019. Concurrently, the Company has granted four put options to E.R. with an aggregate exercise price of $105.39 million or $26.35 million per Step 2 Vessel (the “Put Options”) exercisable by E.R. from April 2, 2019 to April 4, 2019 (inclusive), in the event that the Company does not exercise the Call Options. The aggregate exercise price of the Call and Put Options is payable in either, 2/3 cash and 1/3 common shares of Star Bulk (the “Step 2 Consideration Shares”), or 100\% cash, at the option of the Company. The number of Step 2 Consideration Shares to be issued to E.R. (if any), will be determined by the net asset value of the Company, which will be based on the average vessel valuations by independent vessel appraisers as of March 31, 2019 and will be subject to adjustments for the Company’s cash, debt and remaining capital expenditures as of one business day prior to the delivery date of each of the Step 2 Vessels.

Below are the details of the Vessels to be acquired from E.R and charter contracts expected to be novated at the time of deliveries:

|

The deliveries of Step 1 and Step 2 Vessels (subject to the exercise of the Call or Put Option) remain also subject to customary closing conditions, including the novation of any existing charter parties of the Vessels. The Company expects to take delivery of Step 1 Vessels in Q4 2018, while Step 2 Vessels deliveries, subject to the exercise of the Call or Put Option, are expected to take place between early April and mid July 2019.

After giving effect to Step 1 Acquisition and Step 2 Acquisition, Star Bulk will have a fleet of 115 vessels on a fully delivered basis, aggregate cargo-carrying capacity of approximately 13.39 million deadweight tons and vessels with an average age of 7.5 years.

Petros Pappas, Chief Executive Officer of Star Bulk, commented: “I am very pleased that Star Bulk is acquiring a high quality, modern fleet from E.R. in a structured transaction that combines attractive prices with flexibility for the Company. We are excited to expand our footprint in the Capesize segment, especially in a period that the dry bulk market is tightening. It is also with great pleasure to welcome a prominent ship owner, Mr. Erck Rickmers, to our shareholder base and believe that this transaction validates once again Star Bulk’s ability to use our shares as currency in accretive acquisitions for our shareholders.“

About Star Bulk

Star Bulk is a global shipping company providing worldwide seaborne transportation solutions in the dry bulk sector. Star Bulk’s vessels transport major bulks, which include iron ore, coal and grain, and minor bulks, which include bauxite, fertilizers and steel products. Star Bulk was incorporated in the Marshall Islands on December 13, 2006 and maintains executive offices in Athens, Greece. Its common stock trades on the Nasdaq Global Select Market under the symbol “SBLK” and on the Oslo Stock Exchange under the ticker “SBLK R”. On a fully delivered basis, Star Bulk will have a fleet of 111 vessels, with an aggregate capacity of 12.67 million dwt, consisting of 17 Newcastlemax, 20 Capesize, 2 Mini Capesize, 7 Post Panamax, 35 Kamsarmax, 2 Panamax, 16 Ultramax and 12 Supramax vessels with carrying capacities between 52,055 dwt and 209,537 dwt. The Company holds call options and has sold respective put options on 4 Capesize vessels, with exercise dates in early April 2019.

![]()

Powered by ![]() © Μaritimes 2019

© Μaritimes 2019