Why 2017 looks positive for the dry bulk market

As part of the program I held a presentation on the key drivers for dry bulk freight in 2016 and 2017, which was followed by a panel debate moderated by John Kearsey (SSY) and with Aristides Pittas (Euroseas), Jeremy Palin (Arrow) and myself as panelists.

Last year’s presentation focused on hope. In the sense that the emerging trend we saw at that time was 1) an improving Chinese real estate sector, 2) cuts in Chinese coal production and that 3) growing coal imports into Emerging Asia would continue into 2016. These factors have been positive drivers for dry bulk freight in 2016, however we had to wait until the last quarter of the year before we could tell whether those trends would lead to any meaningful recovery in dry bulk freight.

Key trends in this year’s presentation were an improving growth rate in global industrial production and global steel production, a positive trend in the global coal trade and grain trade creates a solid platform for raw material demand in 2017.

On the supply side we will see low fleet growth in 2017 and 2018 as the order book is very limited. In our base case we expect a fleet growth of 1.7\% in 2017 and 0.7\% in 2018. How low the fleet growth gets will to a large extent be a function of the freight market. We argue that scrapping, slippage and cancellations will be elastic to the demand growth. Effective supply growth will also depend on the speed of the fleet.

Take the example from the Panamax fleet which according to our monitoring has been running at around 11.4 knots lately. If freight increase enough to incentivize a speed increase (which also will be a function of bunker prices) then there is a latent supply increase through speed increase of about 16-17\% if the fleet speed increases to e.g. 13.75 knots (assuming that 80\% of the voyage days are at sea). Hence, if we experience some unforeseen demand shock then the potential of speed increases will slow down the pace of improvement in freight rates. So while we do expect the demand growth to outstrip fleet growth in 2017 we can forget about the freight rates seen in the hay days prior to 2011.

In the subsequent panel two of the key issues discussed were:

1) Will new ballast water and bunker fuel regulations have a material impact on scrapping in the next couple of years?

The consensus answer to this was no. An investment cost of 4-500,000$ related to ballast water treatment systems will not be a decisive factor for whether or not you scrap a relatively young vessel of e.g. 15 years. Bunker fuel regulations will not impact scrapping in the next couple of years but may have an impact in 2019 if the implementation date of 2020 is maintained.

It will also depend on whether refineries are able to produce enough low Sulphur fuel, in which case most of the cost will be transferred to the end user of the transported products. If scrubber technology is widely adopted, then the majority of the cost will be carried by the owners. If this is the outcome and the cost of scrubbers remain high than this can lead to higher scrapping, but only in a low freight market.

2) What will it take to revive dry bulk carrier ordering?

The panel argued that with the current spread between new build and second hand prices it is very unlikely that we will see a substantial tick up in newbuilding ordering any time soon. I also argued that while the coal outlook in the next 3-5 years looks ok, the outlook is far more challenging on a 15-20 years’ horizon. Such an uncertainty should make potential investors think twice before ordering new vessels, or at least use a high discount factor on future earnings to reflect the risk when they make their investment decisions.

Source: Torvald Klaveness

Seagull Maritime responds to social media awareness

MTI Network is the world’s leading incident response network dedicated to serving the shipping, energy, offshore and transportation industries. It offers a variety of social media services such as training, guidelines, strategy and more. The new e-learning and video module from Seagull Maritime explores the impact a seemingly innocent social media post can have when it involves a safety or security incident onboard.

|

“Social media has infiltrated every aspect of both our personal and professional lives,” says Roger Ringstad, Managing Director Seagull Maritime. “People have gone from being consumers to also being producers of media. Social media reaches millions of people globally. Analysing your online presence, addressing potentially damaging coverage and establishing how it might be improved have become integral aspects of risk management.”

"Through social media crews can inadvertently become on-scene-reporters when a safety or security incident is taking place onboard. Crew are often unaware of the reach of their pictures and status updates, and don’t consider the consequences they might have if taken out of context. It's important that we provide education and guidelines as to what is and is not appropriate to post online .", says Mr Martin Baxendale, Managing Director - MTI Network.

The aim of the new e-learning module is to raise awareness of correct social media practice among both shore based personnel and seafaring staff. Mr Ringstad emphasises the importance of fully understanding how social media should be used during a crisis and properly grasping the potential reputational and/or commercial risks ‘innocent’ posts can pose to a company.

“When posting, be sensible; don’t press send on anything you wouldn’t be comfortable appearing in your bosses’ inbox, or on the front page of a national paper. If in doubt, don’t post,” Mr Ringstad concludes.

PRODUCT INFORMATION

This email address is being protected from spambots. You need JavaScript enabled to view it.

Nakilat bags two awards at Lloyd’s List Awards 2016

|

The awards come in recognition of the company’s outstanding contribution towards reducing its environmental footprint through implementation of green technologies onboard its LNG vessels, as well as its successful fleet expansion amidst challenging market conditions and ability to deliver value to its shareholders through prudent long-term strategies and agreements.

Held annually, the Lloyd’s List Middle East & Indian Subcontinent Awards is one of the most prestigious awards in the shipping industry, recognizing companies and individuals that have demonstrated outstanding achievements over the past year.

Nakilat Managing Director Eng. Abdullah Fadhalah Al Sulaiti said: “As a leading company transporting LNG, we have a responsibility not only to ensure the safe working environment for our staff but also to the environment we operate in, which is in line with our corporate responsibility derived from Qatar National Vision 2030. This achievement today serves as a great motivation for us as we embark on consolidating a fully-fledged ship operation for our wholly-owned vessels. We are honoured to be in receipt of these two prestigious awards and be recognized for the hard work, dedication and effort put in by our team, as well as the excellent co-operation and support by our partners. This is testament that the organization is moving in the right direction of achieving our vision to be a global leader and provider of choice for energy transportation and maritime services.”

Taking a holistic and proactive approach towards sustainable development, Nakilat has successfully carried out the world’s first MEGI (Main Engine Gas Injection) conversion and BWTS (Ballast Water Treatment System) installation onboard its LNG carriers. In addition, a large majority of vessels in Nakilat’s fleet have been certified with the Green Award as a testament to their clean and safe operating systems. The company has consistently delivered value to its shareholders despite challenging market conditions, and upheld excellent safety standards across its fleet to high customer satisfaction.

Oil Traders May Abandon Ship After OPEC Cuts Profits at Sea

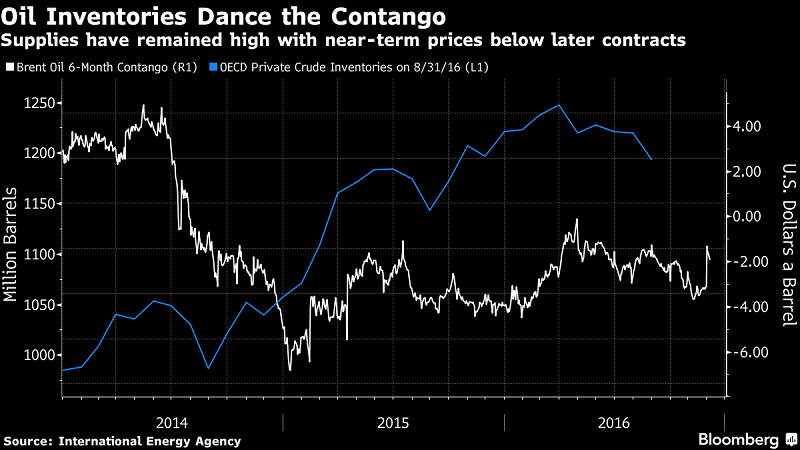

The group’s pledge to cut output and ease a global glut has weakened a market structure known as contango that benefited traders who stocked crude on ships to be sold at a potential profit in the future. The planned reductions have boosted the value of earlier-loading oil relative to cargoes for later, meaning returns from stored supplies aren’t going to be enough to offset the cost of chartering a tanker for months.

In one of the unintended consequences of the decision by the Organization of Petroleum Exporting Countries, millions of barrels that were in floating storage could potentially flood back into the market and limit the price jump from OPEC’s supply curbs. That adds to concerns that higher U.S. production next year may offset the group’s first output cuts in eight years, and hamper a sustained recovery in prices that are still more than 50 percent below 2014 levels.

“The contango trade is not going to be nearly as profitable next year as it was this year,” said Amrita Sen, chief oil analyst for industry consultant Energy Aspects Ltd. “If OPEC follows through with its cuts, you’re going to see global stocks of crude start to draw.”

The premium for later supplies of Brent, the benchmark for more than half of the world’s oil, shrunk to as little as $1.77 per barrel on Dec. 1, the day after OPEC agreed to curtail output by 1.2 million barrels per day. That’s not enough to make a profit after leasing a giant oil tanker for half a year at a cost equivalent of $3.15 to $3.38 per barrel, according to data from a shipbroker and charterer.

As recently as last month, that 6-month contango was at about $4.50 a barrel, which was a large enough gap to make it potentially viable for traders to profitably store crude for that long. The spread was at $2.62 a barrel as of 11:14 a.m. London time on Thursday.

Swiftly Narrowing

More than 100 million barrels of oil are being hoarded on vessels at sea, but with the contango “swiftly narrowing,” that figure will probably shrink in the future, according to Matt Smith, director of commodity research at ClipperData LLC, a firm that analyzes and tracks crude and fuel flows globally.

“One consequence of the OPEC decision was a sharp decline in contango for crude oil futures,” leading to the viability of storing oil on vessels to “reverse sharply,” JPMorgan Chase & Co. said in a note dated Dec. 5. “This meant that floating storage economics, which were modestly positive for several weeks, went decidedly negative.”

And it’s not just oil stored on supertankers that could seep into the market. The narrower contango probably means that crude held in onshore storage complexes such as South Africa’s Saldanha Bay “will likely start to get drawn down and compete with spot barrels,” Citigroup Inc. said in a research note dated Dec. 6.

|

A persistent contango since the oil market began crashing in mid-2014 has driven a record amount of oil into storage. Global industrial stockpiles in developed nations peaked at 1.23 billion barrels in March this year, with inventories still 17 percent above the five-year seasonal average in August, based on estimates by the International Energy Agency.

That inventory overhang is what OPEC says it’s targeting with its production cuts. The focus is now on which non-OPEC producers will join Russia in reducing output. OPEC is hoping they will cut another 300,000 barrels a day beyond the 300,000 barrels already promised by Russia.

“Much of the oil that has gone into landed and floated storage since the price slump began in mid-2014 has done so simply because it had nowhere else to go,” said Vandana Hari, principal at energy consultancy firm Vanda Insights. “Higher prompt prices could certainly spur oil to move out of storage -- possibly dulling the impact of OPEC’s restraint in the initial period once their agreement takes effect.”

source:www.bloomberg.com

Coscol changes name to Cosco Shipping Specialised Carriers

|

Shanghai-listed Cosco Shipping Specialised Carriers currently operates more than 150 ships ranging from heavy lifts, semi-submersibles, ro-ros and ice-class vessels.

The new name follows the merger of the two state-owned shipping conglomerates, China Cosco Group and China Shipping Group, to form China Cosco Shipping Corporation Limited (Cosco Shipping).

Since the official launch of Cosco Shipping in February and a rebranding in September, the group’s various subsidiaries have gone through organisational restructures, including changing of company names to reflect their respective business strategy going forward.

© Copyright 2016 Seatrade

ECSATwitter 6.12.2016 European Shipping Week 2017 welcomes keynote speakers and panelists

Moderated by Julian Bray, Editor-in-Chief of Tradewinds, the flagship conference will attract up to 400 top industry shipowners and regulatory personnel who will hear from industry specialists on key issues under the overarching theme of: European Shipping Policy: Delivering Global Competitiveness, Quality and Sustainability.

It will begin with delegates being welcomed by the Chairman of ESW2017 and ECSA’s Secretary General, Patrick Verhoeven, who will then hand over to Julian who will introduce Violeta Bulc, European Commissioner for Transport; Michael Cramer, Chairman of the TRAN Committee at the European Parliament; and also Joe Mizzi, Minister of Transport and Infrastructure in Malta, who will start the Conference by touching on the institutional keynotes.

The Global trends affecting shipping session will include presentations by Märtha Rehnberg, Associate Partner, Dare Disrupt Trade and Alexander Stubb, Former Prime Minister of Finland, Member of Parliament of Finland. They will then be followed by Jos Delbeke, Director-General DG Climate Action in the European Commission. After a Q&A session, Kyriakos Anastassiadis, CEO, Celestyal Cruises; Marialaura Dell'Abate, Amoretti Armatori Group; Mark Dickinson, General Secretary, Nautilus International; Trond Hodne, Business Director, DNV GL Maritime; Henriette Thygessen, CEO, Svitzer and Melina Travlou, CEO, Neptune Lines will contribute to the presentations.

The conference will also allow time to network for regulators and shipowners to discuss the themes covering industry standards, safety levels, environmental concerns and training. The delegates will have the ideal platform for both industry and regulators to come together to debate and agree a pathway on these and other issues moving forward.

European Shipping Policy’s state of play will also come under the spotlight within the business climate by the panellists Claus Frelle-Petersen, Senior Manager at Deloitte Nord and Sophie Moonen, Head of Unit State Aid Transport for DG Comp. Decarbornisation will be discussed within the industry and talk turning to how to take those steps forward.

Additional speakers include: Thomas Abrahamson, European Transport Workers’ Federation (ETF); Merja Kyllönen, Member of the European Parliament; Ivan Sammut, Registrar General, Malta Flag Administration; Niels Smedegaard, President, ECSA and Wim Van de Camp, Member of the European Parliament. The afternoon panel will also include Magda Kopczynska, Director of Maritime Transport at DG Move.

The flagship conference will then finish with a closing keynote by Henrik Hololei, Director-General DG Move at the European Commission.

More information about the European Shipping Week and advice on how to books seats at the Conference and Gala Dinner is available at:

https://www.europeanshippingweek.com

The complete list of speakers include:

Patrick Verhoeven, Chairman, European Shipping Week Steering Group and ECSA’s Secretary General

Julian Bray, Editor-in-Chief, TradeWinds

Michael Cramer, Chairman of the TRAN Committee, European Parliament

Joe Mizzi, Minister of Transport & Infrastructure, Malta

Violeta Bulc, Commissioner for Transport, European Commission

Märtha Rehnberg, Associate Partner, Dare Disrupt

Alexander Stubb, Member of Parliament, Finland

Jos Delbeke, Director-General DG Climate Action in the European Commission

Kyriakos Anastassiadis, CEO, Celestyal Cruises

Marialaura Dell’Abate, Adviser, Amoretti Armatori Group

Mark Dickinson, General Secretary, Nautilus International

Trond Hodne, Business Director, DNV GL Maritime

Henriette Thygessen, CEO, Svitzer

Melina Travlou, CEO, Neptune Lines

Elvira Deleu, 3rd Officer, Exmar Shipmanagement

Claus Frelle-Petersen, Senior Manager, Deloitte Nord

Sophie Moonen, Head of Unite State Aid Transport, DG Comp

Markku Mylly, Executive Director, EMSA

Thomas Abrahamson, European Transport Workers’ Federation (ETF)

Merja Kyllönen, Member of the European Parliament

Ivan Sammut, Registrar General, Malta Flag Administration

Niels Smedegaard, President, ECSA

Wim Van de Camp, Member of the European Parliament

Magda Kopczynska, Director Maritime Transport in DG Move will join the afternoon panel

Henrik Hololei, Director-General, DG Move, European Commission

Notes to Editors:

European Shipping Week, which was started in 2015 by the European Community Shipowners’ Associations (ECSA), is run by a Steering Group made up of Europe’s main shipping organisations as well as the European Commission and Shipping Innovation. The shipping organisations involved on the Steering Group include: ECSA; Cruise Lines International Association (CLIA) Europe; European Community Association of Ship Brokers and Agents (ECASBA); Interferry; the European Dredging Association (EuDA); the World Shipping Council (WSC), the European Transport Workers’ Federation (ETF), the European Tugowners’ Association (ETA) as well as the European Maritime Pilots Association (EMPA). Other European shipping associations may also be invited to support the initiative and hold relevant events during the week.

European Shipping Week will be held in Brussels during the week of February 27th – March 3, 2017 when shipping industry leaders from Europe and around the world will descend on Brussels to meet and network with top legislators from the European Commission, European Parliament and the Council of Ministers.

The week‐long series of high level events will bring together the major players in the shipping industry. ESW is organised by Shipping Innovation – the driving force behind the highly successful London International Shipping Week (LISW).

RINA Sets New Standards for Crew Competence

|

Cpt. Nicolo Terrei, Managing Director of RINA Academy Philippines and his team looked at the methods and tools within this innovative system, which has taken over a decade to develop. He presented the platform developed by his team that collects all records related to the identification of competence gaps, training paths, post assessment, and KPI’s, and also provided the audience with the very first illustrative results and statistics from the implementation of the CMS.

The new system will be benefitted from the recent expansion of RINA Academy to a new worldwide organization in maritime training which is now offering in addition to traditional maritime courses, new specific and focused training courses covering all technical courses and non-technical (behavioural) courses relating to crew competence.

RINA was represented at the Conference by Mr. Alessandro Mura, RINA Academy, Manager of Crew Training, Mr. Stefanos Chatzinikolaou, Research & Innovation/RINA Academy Hellas Manager and Mr. Leander Aarons, Area Manager, Hong Kong and Vietnam.

Chatzinikolaou of RINA Hellas emphasised that RINA’s commitment to training and competence assessment needs to become well-known in the maritime industry, especially since the industry has recently been under pressure to bring forward new standards for crew competence. He also stated that the RINA Academy Hellas will be dedicated to introducing this system to the Greek maritime community.

Competence, the ability of an individual to do a job appropriately, is different to a qualification. A qualified individual holds just a license to perform a job. For shipping companies, qualified personnel are simply not enough; competent personnel are a necessity given the multitude of tasks - often involving high risk levels - that are demanded on-board ships and ashore, keeping pace with technological advancements, the change and introduction of new legislation and the expected high standards in safety, security and environmental awareness.

These ideas have driven RINA to introduce the Competence Management System as a tool for shipping companies to establish robust criteria for the selection and recruitment, training and career development of their on-board personnel and an advanced human resources programme that constantly targets higher levels of skill and excellence.

RINA Services S.p.A. is the RINA company active in classification, certification, inspection and testing services.

RINA is a multi-national Group which delivers verification, certification, conformity assessment, marine classification, environmental enhancement, product testing, site supervision & vendor inspection, training and engineering consultancy across a wide range of industries and services. RINA operates through a network of companies covering Energy, Marine, Infrastructure & Construction, Transport & Logistics, Food & Agriculture, Environment & Sustainability, Finance & Public Institutions and Business Governance. With a turnover of over 378 million Euros in 2015, over 3,000 employees, and 163 offices in 60 countries worldwide, RINA is recognised as an authoritative member of key international organizations and an important contributor to the development of new legislative standards.

THE Alliance enhances its Mediterranean-North America East Coast product with additional cooperation

The port rotation of the AL 6 service will be streamlined and the Spanish ports of Barcelona, Tarragona, Valencia and Algeciras will be served through a new cooperation with ZIM Line on the latter’s existing Mediterranean-North America loop. This additional service will be branded as the AL 7. The Italian ports of Salerno, Livorno, La Spezia, Genoa as well as FOS in France will remain part of the AL 6 service as previously announced.

By differentiating the port coverage within the Mediterranean the members of THE Alliance will offer their customer’s superior transit times between the two important regions US/Canada and Mediterranean

The new port rotation of the AL 6 service will be:

Salerno – Livorno – La Spezia – Genoa – FOS – Halifax – New York – Norfolk – Savannah – Salerno

The port coverage of THE Alliance in the AL 7 will be as follows:

Barcelona – Tarragona – Valencia – Algeciras – Halifax – New York – Norfolk – Savannah – Valencia – Tarragona – Barcelona

Both services will be launched at the beginning of April 2017 along with the implementation of the entire THE Alliance product (subject to completion of all relevant regulatory requirements).

The members of THE Alliance are Hapag-Lloyd, “K”Line, Mitsui O.S.K. Lines, Nippon Yusen Kaisha and Yang Ming. The partners plan to deploy a fleet of more than 240 modern ships in the Asia/Europe, North Atlantic and Trans-Pacific trade lanes including the Middle East and the Arabian Gulf/Red Sea. The service network is expected to cover more than 24 ports in Asia including ten Chinese and five Japanese ports with direct calls as well as 20 ports in the US and Canada, six North European and 13 Mediterranean ports, six ports in the Middle East and six ports in Central America/Caribbean. The final and precise port rotations of all 32 services of THE Alliance will be announced soon.

Source: Hapag-Lloyd

Challenges of IMO’s 0.5\% Global Bunker Sulfur Cap

Alternative measurements like scrubbers are also accepted to reduce the ships emission.

The number of 0.5\% had already been unanimously adopted in 2008 during a meeting of the MARPOL Annex VI review group, and was ratified by 53 countries (81.88\% of tonnage). The date of implementation depended on the outcome of a study which the IMO conducted and presented this August (study carried out by CE Delft).

The study aimed to determine if sufficient production and therefore availability of low sulfur fuel oil (LSFO) would be likely. A positive outcome would set the date at 2020, whereas a negative prospect would allow another five years before the new regulation became effective. Bloomberg estimated that the global cap would add 250 million metric tons of LSFO to global demand.

The IMO study concluded that there are no bottlenecks of low sulfur fuel to expect, whereas another published study by EnSys (Energy & Systems Inc.) claimed the opposite. It is worth noting that EnSys made an unsuccessful bid to carry out the official IMO study. The EnSys study was supported by BIMCO and IPIESA, an oil and gas industry association.

However, the International Chamber of Shipping pointed out in its Annual Review 2016 out that the IMO might place itself under political pressure if it set the date at 2025:

“In reality the decision taken by the IMO is likely to be a political one. […] Even if the supply of compliant fuel is projected to be tight, IMO Member States might nevertheless conclude that it is politically unacceptable to postpone implementation.” ICS Annual Review 2016, p. 18

This may have its roots in the fact that the European Union has already agreed that the sulfur cap will be effective for all 200-mile deep EU Member coastlines by 2020. The coastline reaches partly into the Indian and Pacific Ocean as some states have territories overseas. Setting the date to 2025 would make the North African Coast corridors where 3.5\% sulfur is still allowed, too close to many European States for the liking of the EU regulators.

Does the Sulfur Cap Make Sense?

It might in fact be a case of too little too late. Not only does the European Union take over action regarding environmental regulations and leaves the IMO behind in the political field, in addition the IMO regulations are too weak and the cap agreed on is too forgiving, from an environmental point of view.

The IMO wasted 10 years following Kyoto which tasked the organization with regulating greenhouse gas emissions. This was stated by Bill Hemmings, Director of Aviation and Shipping of the NGO European Federation for Transport and Environment, which is counseling the UNO on environmental issues. Shipping companies and ship managers may cringe because of the ever-rising costs of remaining compliant by using better fuels like marine diesel or expensive technologies like scrubber. Conversely, NGOs and scientists cringe because even 0.5\% of sulfur is still five hundred times higher than sulfur limits in diesel for cars, where its capped at 0.001\%.

It has long been known that vessels pollute the environment much more than all cars combined, and that they cause tens of thousands of premature deaths alone in Europe. So, does it makes sense to further reduce sulfur? Yes it does, but many companies will be affected negatively.

However, there are other points to consider when judging the environmental impact. The high sulfur exhaust of vessels helps to counter the CO2 greenhouse effect. This is because the sulfur dioxide reduces the amount of solar energy reaching the surface, hence it cools down the planet. This man-made influence is dwarfed by natural sulfur oxide exhaust of algae, which produce a compound called DMSP (dimethylsulfoniopropionate).

This compound is released slowly over time from algae close to the surface and act as a sun screen. When other phytoplankton start eating the algae DMSP is released in big quantities into the water from the digested algae. Bacteria in the water start processing the chemical, creating dimethylsulfide (DMS), a gas which leads to the formation of clouds (cloud condensation nuclei). Close to the coastline we recognize this as the so typical “ocean smell”. Clouds are most important for maintaining the climate as they reflect solar energy back into space, just as SOx (sulfur oxide) does.

This process is threatened by an effect called ocean acidification. The ocean basically acts as a CO2 sink by binding CO2 from the atmosphere. This makes the ocean more and more sour, because the carbon dioxide reacts with water and forms H2CO3 (carbonic acid). Ocean acidification is a major cause of dying coral reefs and the destruction of phytoplankton, which we need to produce DMS for cloud building. Since the beginning of the industrial revolution the so-called ocean acidification has stored roughly a third of all man-made emissions.

It might look far-fetched, but refining an additional 250 million metric tonnes of fuel has a very negative impact on CO2 emissions. Firstly, the additional production steps demand additional energy and it is likely that this will be covered by burning non-renewable resources, secondly the refining itself sets free CO2 emissions. Therefore, capping sulfur will accelerate global warming to some degree.

Cost and Challenges of Sulfur Reduction

Vessel owners basically can decide between different strategies to meet the requirements, all have advantages and disadvantages.

- They can install scrubber systems

- They can buy more expensive low sulfur fuel oils like MGO/MDO or new ECA fuels, e.g. Exxon’s HDM50. In total, there are more than 20 new blends.

- They can refit the vessel to LNG

Despite investment and operational costs there are additional less obvious expenses. One is the loss of cargo room when fitting a scrubber into the vessel. The German ferry company TT Lines carried out a pilot project, fitting four scrubbers as hybrid systems (open and closed loop) into its ferry ROBIN HOOD (6300 tdw, 180 m length). Last year, at the ISF Conference at the University of Flensburg in Germany, the company presented the results of the project.

The ROBIN HOOD scrubbers were fitted into its port and starboard funnels, whereas the two container sized engine compartments had to be fitted below deck, blocking approximately one sixth of its deck cargo space. In total 17,500 meters of electric cable, 700 meters of GRE pipes and 2,000 pieces of components had to be installed.

New equipment comes with new administrational effort and additional maintenance jobs. Few ranks are familiar with the new systems, leading to higher costs in the beginning. Due to the new maintenance jobs time is taken out of the tight schedule.

Vessels which are switching permanently from HFO to low sulfur fuels instead of using scrubbers, may run into similar problems as today when entering SECAs. Dr. Reinhard Krapp of the VDR (an industry association of German shipping companies) published in 2014 a paper named “Industry Guidance on Compliance with the Sulphur ECA Requirements” and pointed out a number of problems when switching fuels.

One of the main aspects are operational problems using engines optimized for HFO on MGO/MDO when running for longer durations. It is assumed that this is due to a lower injection temperature (approx. 100° C lower), which causes stress on the surrounding materials and seals. Another factor might be that MGO/MDO have higher homogeneity leading to a faster rise in pressure when combusted. This might change the vibrations and force transmission says Dr. Krapp. As a result, fuel could leak into lubricants.

He also pointed out that the energy density of current HFO is approximately 8\% higher than that of distillates. In return, distillates have a 2\% higher net calorific value, with a net loss of approximately 6\%.

There are many more concerns when using low sulfur fuels for HFO-designed machinery. Most of them are well understood as the subject has been researched well since the introduction of SECA regulations:

- Lower acidity: Part of the sulfur is converted into sulfuric acid (H2SO4) during the combustion process. Using common cylinder oil with a high alkali base number will lead to wear, as the amount of sulfuric acid is now lower.

- The use of ultra-low sulfur fuels requires special consideration. Their properties vary depending on the supplier and there may be incompatibilities when mixed with HFO, MDO or other ULSFs

- The much lower viscosity and reduced lubrication can cause abnormal wear.

Monitoring the Cap

Enforcing the sulfur cap in international waters might be challenging. The questions are, who is monitoring it and who pays for it? If the regulation is to be taken seriously then enforcement and control must occur, otherwise thee will be no incentive to carry out the regulation. The most likely solution will be the introduction of some technological recording and measurement of emissions.

At least the surveillance close to the outside borders of SECA zones will be less troublesome, because technological measurements inside the zones already exist for the purpose of supervising them. Authorities corporate within the areas, e.g. the joint surveillance Bonn Agreement (North Sea) to detect oil spillages and harmful chemicals, and similar agreements between HELCOM members (Baltic Sea) are in place. A number of tools like airborne surveillance are used to determine vessel emission (NOx, CO2, SO2) and could be applied further outside of current zones.

These airplanes use antennas to “sniff” emissions from nearby vessels giving hints to Port State Control officers about which vessel to enter. The advantage over optical systems like differential optical absorption spectroscopy (DOAS) is that the system can be deployed at night or on cloudy days.

The PSCs of Paris MoU and Tokyo MoU have already been announced this November to increase their focus on sulfur limit regulation and to plan a major campaign for 2018. The concentrate campaign indicates that embarked officers will thoroughly examine the vessel to determine whether it has remained compliant. However, realistic long-term surveillance options for international waters have not been revealed yet. So far PSC has no power outside its own waters and could only inform the flag state about sulfur limit exceedance.

The idea to obtain emission data by multiplying fuel emission factors by vessel journey data is interesting. This is much more an organizational than technological challenge. Bunker agents would need to deliver precise data about the ship they have sold and the type of bunker, requiring in turn an additional monitoring system.

Vessel journey could be calculated by combining available positioning data, e.g. from HELCOMs Automatic Identification Systems (AIS), with other available data sources like Lloyd’s Fairplay database of vessel machinery, and operational data from the ship. Monitoring and storing the data of wash water discharge and emission exhaust from scrubbers within the voyage data recorder, would allow a meaningful combination with GPS data, thus, creating a system which could be used to determine when, where and how much SO2 a vessel emits.

The only possible way to make absolutely certain that vessels are not switching back to HFO would be to disallow bunkering of HFO if a vessel does not possess a cleaning system. However, until a functioning control system is up and running many will try to exploit loopholes. As often reported the MARPOL Annex VI states that the vessel “shall not be required to deviate from its intended voyage or to delay unduly the voyage in order to achieve compliance” (Regulation 18, 2.2). Thus, the concerns are that vessels will bunker on purpose in these harbors where only HFO is available.

Less widely reported is the fact that this phrase applies only if the ship can present a record of actions taken to achieve compliance and evidence provided “…that it attempted to purchase compliant fuel oil in accordance with its voyage plan and, if it was not made available where planned, that attempts were made to locate alternative sources” (Regulation 18, 2.1.1 and 2.1.2). Furthermore, the vessel needs to notify the competent authority that a compliant bunker was not available (pro-active). These measurements minimize possible abuse of the exemption.

Production Challenges

Despite monitoring the cap, the distribution of suitable fuels is the main challenge. It appears that many ports will not be able to deliver LSFO in satisfactory amounts by 2020.

The International Bunker Industry Association (IBIA) warned that many ports and countries will not be able to replace the current supply level of HFO with LSFO in time. These ports would then need to import bunker fuel from distant refineries. In return this would lead to a higher non-competitive bunker price and additional environmental pollution, due to transport, creating winners and losers on the bunker market, where the winners are those who are able to satisfy demand for a good price.

Especially jeopardized are those ports which relay exclusively on local refineries. If there were to be regional imbalances the bunker market might shift towards the regions that can provide compliant fuels.

But why are the refiners unable to satisfy demand despite the fact that four years remain, and considering that the sulfur limit level has been known since 2008? We do not know why they are moving so late. IBIA for example pointed out that before the due date few vessels will be using the more expensive refined fuels. Most vessels will only switch when necessary. This is dangerous as it could lead to a situation where the “world fleet” tries to switch overnight; such a spike in demand could not be handled. Similarly, refiners will try to add capacity as late as possible.

Today refiners are especially concerned about who will buy high sulfur fuel after 2020 and how to expand the production of LSFO. Demands could be met by blending bunkers with distillates to create HFO with S ≤ 0.5\% or by processing away sulfur (hydroconversion / hydrodesulfurization). The last option requires additional production steps and (if not in place) additional equipment. To blend bunker, low sulfur distillates are mixed with high sulfur residuals to create the required sulfur content. The used distillates are lost for the market. Both options will have residual “left-overs” from production.

In addition, the maritime industry will start to compete with other shore-based industries by acquiring higher distilled fuels. Refiners will then sell to the market offering the greatest returns.

How big is the shift?

The IMO study sets the high sulfur fuel oils demand of 2012 as its base for its calculation, it was 228 million metric tonnes. In 2020 this could sink to 36 million tonnes (p. 13). Refiners would sell ~85\% less high sulfur fuels to the maritime industry than they did in 2012. The IMO concludes that these oils will be a niche product, only used by ship operators who decide to install scrubbers. By 2020 more than 3,800 ships are expected to use such cleaning technology (p. 151).

This is basically a swap, because vessels will continue to use fuels. The demand for total marine heavy fuel oils containing less than 0.5\% sulfur is expected to rise to 233 mt. Adding the anticipated 36 mt of high sulfur oils shows that the bunker market is expected to be bigger in 2020 than it was in 2012. (p. 13)

How big is the market impact?

Since the end of the 80s the global demand for residuals (all industries) has been sinking continuously, despite maritime demands for HFO rising continuously. In 1990 almost 13.3 million barrels per day (BPD) of residuals were produced. In 2012 production and demand were both four million BPD lower.

On average, the maritime industry requires roughly 35\% of the global residual fuel production for HFO, the other 65\% is consumed by shore-based industries such as power plants.

Considering the number of vessels which are expected to continue burning HFO, the total global demand for residual fuels will be “only” ~30\% lower than it was in 2012. A part of the 30\% overhead could be used within new-build coking units. This would ease the demand for distillates to blend bunker, although it seems unlikely that there will be a sufficient number of new coking units by 2020. (Data by John M. Mayes and John Auers of Turner, Mason & Company and IndexMundi.com)

Dealing with an HFO surplus and avoiding market disruptions for non-maritime HFO demands is the real challenge, not producing enough S ≤ 0.5 fuels. This matters because it shows that maritime bunker is only a share of the refiner’s residual fuel oil customer portfolio.

Source: Matti Bargfried, CODie software products e.K. (Matti Bargfried is Head of Marketing at the maritime IT company „CODie“- A Germany based producer of fleet and crew management systems. Matti is serving the industry since 10 years. Visit CODie.com for more.)

GREEK SHIPPING AWARDS 2016: THE WINNERS

A NEW RECORD attendance and a host of celebrities contributed to the success of the Lloyd’s List Greek Shipping Awards for 2016, which were presented at a packed dinner event on Friday, December 2 at the Athenaeum InterContinental Hotel in Athens.

Nearly 1,200 of Greece’s leading shipping personalities, executives and their guests were present to see some of the Greek shipping industry’s best-known personalities and companies recognised.

The event, organised by Lloyd’s List, the international maritime newspaper established in 1734, included welcoming speeches by Greece’s minister of Shipping and Island Policy, Panagiotis Kouroumblis, and Junichiro Iida, executive vice president of ClassNK, the event’s overall lead sponsor.

Guests enjoyed a pre-dinner cocktail reception hosted by the Malta Ship Registry and the event was also supported by numerous Greek and international companies sponsoring individual awards.

Hellenic Chamber of Shipping President, George Pateras, presented a donation on behalf of the event organisers to ‘Argo’, the charity supporting children with special needs in the families of Greek seafarers.

The awards are held annually to recognise and reward achievement and meritorious activity in the Greek shipping industry as well as to promote Greece’s status as a maritime centre. Winners are chosen by an independent panel of judges representing a broad cross-section of the Greek shipping industry.

THE WINNERS

Panos Laskaridis was named 2016 Greek Shipping Personality of the Year. Mr Laskaridis for a landmark year that advanced Laskaridis Shipping Company’s diversification from its reefer business into becoming a leading dry bulk owner. Other new moves included investment in a new dry bulk terminal in Uruguay. Additionally, Mr Laskaridis has been earmarked as next President of ECSA – the European Community Shipowners’ Associations – a key position to represent Greek shipping’s concerns.

Lloyd’s List’s Greek Shipping Newsmaker of the Year Award went to Polys Hajioannou, chief executive of US-listed Safe Bulkers, for “playing good defence” and by being transparently fair to shareholders. Regular deals with lenders in 2016 strengthened the position of Safe Bulkers. Mr Hajiannou has also been creative in finding new funds without diluting the company’s shareholders. Steps included himself purchasing two newbuildings on terms that favoured his public investors. The Award is decided by the editorial staff of Lloyd’s List.

Nicos D. Efthymiou was awarded the Lloyd’s List / Propeller Club Lifetime Achievement Award for an outstanding career that included serving as President of the Union of Greek Shipowners from 2003-2009. He has long been a champion of the Greek flag, Greek seafarers and development of Piraeus into an international business centre.

Stavroula Betsakou won the New Generation Shipping Award, open to personalities of no more than 40 years of age. A graduate of the University of Piraeus, Ms Betsakou is head of Tanker Research for Howe Robinson, leading a team of four analysts operating from London and Singapore. She has performed more than 220 tanker market presentations in 21 cities and is frequently hailed as one of the industry’s most exciting young talents.

Peter Hinchliffe was elected International Personality of the Year, the only award open exclusively to non-Greeks. Mr Hinchliffe joined the International Chamber of Shipping in 2001 after 27 years with the Royal Navy. Since 2010 he has been Secretary General of the ICS, and a stalwart supporter of the industry in all fora.

The recipient of the Dry Cargo Company of the Year Award for 2016 was Samos Steamship Co, a company with a 140-year history that has this year expanded with several bulker acquisitions, including the purchase of its largest-ever dry cargo vessel, a Very Large Ore Carrier.

As Tanker Company of the Year the panel chose one of the industry’s most celebrated names – Thenamaris, long recognised as one of the most advanced tanker companies worldwide in its systems, planning and treatment of employees. The Thenamaris fleet now stands at about 60 tankers including 10 on order, and the company has been building a presence in new sectors such as LNG and LPG.

The judges chose Minoan Lines as Passenger Line of the Year for a variety of reasons: the quality of its ships and services, its increasing investment in Hellenic Seaways, the leading domestic ferry operator, and its impressive results as it emerges from the crisis plaguing the sector. It has steadily supported numerous charities in Crete and in Greece.

Carriers Chartering Corporation won the Shipbroker of the Year Award, its second victory in this category. Shipowners that nominated Carriers testified to its close relationships with first-class charterers, its market expertise and support, and its ethical approach to its profession. 2016 has been a particularly good year for Carriers with more than 650 deals in the first nine months, up from 2014 and 2013.

The Shipping Financier of the Year Award went to National Bank of Greece. NBG has been in shipping finance for a century and from the mid-1990s, led by the late Alexandros Tourkolias, it expanded as a major lender. Today NBG maintains a $2.5bn portfolio of loans to Greek owners. Despite difficult conditions the bank has been selectively lending to stand by its existing clients. In 2016 it also launched a new tool providing trade finance and advice to support Greek maritime manufacturing exports.

Vassilis Papageorgiou, Vice Chairman of the Tsakos Group, won the Technical Achievement Award. He spent 23 years with Lloyd’s Register, rising higher than any other Greek surveyor before him. For Tsakos, he has overseen 70 newbuildings of diverse types in various countries and has stood out for his contribution to making shipping a stronger, safety-focused industry.

HEMEXPO was recipient of this year’s prestigious Piraeus International Centre Award. HEMEXPO – the Hellenic Marine Equipment Manufacturers and Exporters – was established in 2014 to promote Greek-made equipment on ships constructed overseas. It has already succeeded, with the support of a few of the country’s leading shipowners, in penetrating markets that previously were unaware of Greek manufacturing companies.

Helmepa Junior won the Award for Safety or Environmental Protection Congratulations to Helmepa Junior. Over the last year, members of the programme carried out a record 3,900 activities throughout Greece with the aim of helping the environment and raising awareness.

The Seafarer of the Year Award was won by Capt Diamantis Papageorgiou. Captain Papageorgiou has served as Master of more than 50 different ferries in Greece’s coastal services and is known for being entrusted with the most difficult routes. Difficult to replace, in his 16 years as a Captain he has taken a total of only one-and-a-half months’ leave. Currently, he is Master of the ‘Nissos Rodos’ for Hellenic Seaways and typifies the company’s commitment to provide a service to the islands under often difficult conditions.

The Eugenides Foundation was winner of the 2016 Education or Training Award. Its wide-ranging and consistent support for marine education over the years has included publishing 134 books, offering of scholarships, and donating simulators and other equipment to the state schools. The Foundation recently spent more than 700,000 Euros to repair and refurbish the Merchant Marine Academy of the Ionian Islands in Cephalonia after the earthquake damage of 2014.

The Ship of the Year Award went to the brand-new LNG carrier Maria Energy of Tsakos Energy Navigation. The Maria Energy was delivered in October 2016 from Hyundai Heavy Industries and was the Tsakos newbuilding department’s 100th newbuilding. The 174,000 cubic metre vessel is the company’s second LNG carrier and the company’s first with tri-fuel diesel electric propulsion.

The Lloyd’s List Intelligence Big Data Award was presented to Moore Stephens for its unique ship operating costs benchmarking tool, ‘OpCost’. Greek-owned ships are the biggest contributor to the OpCost database and the tool is keenly used by Greek owners, especially in poor markets that require even stricter cost controls. The winner was chosen by LLI.

The Awards are supported by prominent bodies in Greek shipping, including the Union of Greek Shipowners, the Hellenic Chamber of Shipping and the Greek Shipping Co-operation Committee. Supporting organisations also include The Hellenic Shortsea Shipowners Association, the Hellenic Marine Environment Protection Association - Helmepa, the Hellenic Shipbrokers’ Association, the Association of Greek Passenger Shipping Companies, the Propeller Club, International Port of Piraeus, WISTA Hellas, the Association of Banking & Financial Executives of Hellenic Shipping, and the Piraeus Association for Maritime Arbitration.

Lloyd’s List Greek Shipping Awards 2016

WINNERS AT-A-GLANCE

Dry Cargo Company of the Year

Samos Steamship Co.

Tanker Company of the Year

Thenamaris

Passenger Line of the Year

Minoan Lines

Shipbroker of the Year

Carriers Chartering Corporation

Shipping Financier of the Year

National Bank of Greece

Technical Achievement Award

Vassilis Papageorgiou

Achievement in Safety or Environmental Protection

Helmepa Junior

Piraeus International Centre Award

HEMEXPO

International Personality of the Year

Peter Hinchliffe

Seafarer of the Year

Capt. Diamantis Papageorgiou

Achievement in Education or Training

Eugenides Foundation

Ship of the Year

“Maria Energy"

Next Generation Shipping Award

Stavroula Betsakou

Lloyd’s List Intelligence Big Data Award

Moore Stephens

Lloyd’s List/Propeller Club Lifetime Achievement Award

Nicos D. Efthymiou

Greek Shipping Newsmaker of the Year

Polys Hajioannou

Greek Shipping Personality of the Year

Panos Laskaridis

|

| Mr. Junichiro Iida, executive vice president of Event Sponsor ClassNK, opened the event with a few words to the international audience. |

|

| The Honourable Mr Joe Mizzi, Minister for Transport and Infrastructure of Malta, addressed guests at the Welcome Reception sponsored by Malta Ship Registry. |

|

| The Minister of Shipping & Island Policy, Mr. Panagiotis Kouroumblis, greeted the audience with a brief Welcome Address. |

|

| Mr. Jiping Chen of China Classification Society made the Champagne Toast to the health of the Greek shipping industry. |

|

| Mr. Anastasios Tzamouranis of Samos Steamship Co. accepting the Dry Cargo Company of the Year Award from Matthew More of sponsor Marichem Marigases. |

|

| Mr. Nikolas Martinos of Thenamaris accepting the Tanker Company of the Year Award from Mr. Lambros Chahalis of sponsor Bureau Veritas. |

|

| Mr. Antonis Maniadakis of Minoan Lines accepting the Passenger Line of the Year Award from Mr. Raffaele Palumbo of sponsor Palumbo Group. |

|

| Mr. Takis Christofides of Carriers Chartering Corporation accepting the Shipbroker of the Year Award from Mr. Harry Hajimichael of sponsor The Tsakos Group. |

|

| Mr. Leonidas Fragkiadakis of National Bank of Greece accepting the Shipping Financier of the Year Award from Ms. Milena Pappas of sponsor Star Bulk Carriers Corporation. |

|

| Mr. Vassilios Papageorgiou accepting the Technical Achievement Award from Mr. Loizos Isaias of sponsor DNV GL. |

|

| Mr. Nick Brown of sponsor Lloyd’s Register with Constantinos Kolovos and Olympia Zisi of Helmepa Junior with Mr. George Gratsos of Helmepa, receiving the Award for Achievement in Safety or Environmental Protection. |

|

| Ms. Despina Panayiotou Theodossiou of sponsor Tototheo Group presenting the Piraeus International Centre Award to Eleni Polychronopoulou of HEMEXPO. |

|

| Mr. Peter Hinchliffe accepting the International Personality of the Year Award from Mr. Gerry Ventouris of sponsor Capital Ship Management Corporation. |

|

| Ms. Natalia Tsavliris-Vasilopoulos of sponsor Tsavliris Salvage Group presenting the Seafarer of the Year Award to Capt. Diamantis Papageorgiou of “Nissos Rodos”. |

|

| Mr. Leonidas Demetriades-Eugenides of the Eugenides Foundation accepting the Award for Achievement in Education or Training from Mr. Dimitris Heliotis of sponsor Target Marine Group. |

|

| Mr. Mathieu Antin (centre) of sponsor RightShip with Ms. Vanessa Florou, Irini and Elisavet Tsakos and Ms. Alexia Papageorgiou accepting the Ship of the Year Award for “Maria Energy”. |

|

| Mr. Theofilos Xenakoudis of sponsor IRI/The Marshall Islands Registry presenting the Next Generation Shipping Award to Ms. Stavroula Betsakou. |

|

| Cyprus’ Transport, Communications and Works Minister Marios Demetriades (centre) presenting the Lloyd’s List Intelligence Big Data Award to Mr. Richard Greiner and Costas Constantinou of Moore Stephens. The Award was sponsored by the Department of Merchant Shipping of Cyprus. |

|

| Mr. Nicos D. Efthymiou receiving the Lloyd’s List/Propeller Club Lifetime Achievement Award from Mr. Vassilis Kroustallis of sponsor ABS. |

|

| Mr. Costis J. Frangoulis of sponsor Franman Group presenting the Greek Shipping Newsmaker of the Year Award to Mr. Polys Hajioannou. |

|

| Mr. Panos Laskaridis accepting the Greek Shipping Personality of the Year Award from Mr. Nikolaos Karamouzis of sponsor Eurobank Group. |

|

| Mr. George D. Pateras of the Hellenic Chamber of Shipping presenting the Lloyd’s List Greek Shipping Awards annual donation to ARGO, accepted by Mrs. Despina Papastelianou. |

|

| Co-hosts for the 2016 Greek Shipping Awards were Nigel Lowry and Andriana Paraskevopoulou. |

|

| The 17 trophies awaiting the winners of the 2016 Greek Shipping Awards. |

|

| A record attendance of 1,200 guests at this year’s event. |

![]()

Powered by ![]() © Μaritimes 2019

© Μaritimes 2019