The Disappearing Shipyards: Not Much Of A Mystery?

This number has now dropped by 62\% to stand at 358 yards as of start July 2017, the lowest number of active yards for many years. With a significant number of yards exiting the market, this month’s Shipbuilding Focus investigates the nature of the these changes.

|

An ‘active’ yard is defined here as one with at least one unit (1,000+ GT) on order, and a yard is active in a specific sector if it has a ship of that type on order. The number of ‘active’ yards can be a useful indicator of shipyard capacity, with the falling number of active yards contributing to the recent decline in capacity. It should be noted that many yards are active in multiple sectors, so the total number of active yards is not equal to the sum of the yards active in each sector.

The Hound Of The Bulkervilles

As of the start of 2009, there were 293 yards active in the bulkcarrier sector, with almost a third of total active shipyards having a bulker on order, due to the boom in bulker ordering and the relatively lower barriers to entry in the sector. This total has now fallen by 67\% to stand at 97 yards. On a regional basis, the largest drop has been in China, with the number of Chinese yards with a bulker on order declining by 73\% to stand at 50 at the start of July. In terms of consolidation, the ‘top 10’ yards (ranked by total dwt on order in the sector) account for 54\% of the total bulker orderbook in dwt terms.

Tanker Tailor Soldier Spy

The number of active yards in the tanker sector (10,000+ dwt) on order has decreased by 55\% since 2009 to currently stand at 89 shipyards, only 8 yards fewer than in the bulker sector. China, Korea and Japan each have between 10 and 20 fewer active yards in the sector. In terms of vessel types, the number of yards building crude tankers has remained steady, with the decline mainly accounted for by product and chemical tankers. Similarly to the bulker sector, the ‘top 10’ yards account for 56\% of the total tanker orderbook in dwt terms.

Pandora’s Boxships

In the containership sector, the number of active yards has declined by 40\% since 2009 to 56 at the start of July. The number of active Asian shipyards has dropped from 64 to 46, while the largest decline was at European yards, with only one shipyard in Europe currently building a boxship, down 96\% (German yards alone accounted for 17\% of the boxship orderbook in 1998 in TEU terms). Consolidation is a little stronger in the boxship sector than in the bulker and tanker sectors, with the ‘top 10’ yards accounting for 61\% of the orderbook in TEU.

So, in total, there are currently 62\% fewer yards ‘active’ than at the start of 2009. The largest drop has been in the bulker sector, but the number of active yards has also declined significantly elsewhere. Furthermore, 30\% of currently active yards are set to complete construction of ships on their orderbook by the end of this year. With these trends in place, it will be no mystery as shipyard capacity continues to slide.

Source: Clarksons

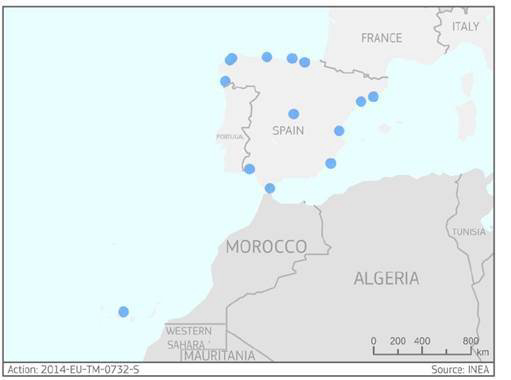

Market study reveals huge potential for lng as a marine fuel in the iberian peninsula

|

| CORE LNGas Hive credit Inea |

DNV GL conducted the market study on behalf of the six-year CORE LNGas hive project1, which aims to provide an investment plan for LNG fuelling in Spain and Portugal. The 33 million Euro project is coordinated by Enagas, and co-funded by the European Commission.

The DNV GL market study has forecasted the potential future demand for LNG as a ship fuel and the required future infrastructure for the areas around Spain and Portugal, covering the Mediterranean, Atlantic and Gibraltar Strait peripherical regions. The results of DNV GL’s analyses have now contributed to the CORE LNGas Hive project’s recommendations for the development of the LNG supply chain infrastructure, involving over 40 ports in the project area.

Fernando Impuesto, CORE LNGas hive project coordinator from Enagas, says: “The consortium partners selected DNV GL to execute the demand studies of the project based on the fact that DNV GL has been at the forefront of the development of LNG as a ship fuel. DNV GL’s network and market knowledge have added to a successful outcome. Through this market study we now have a strong decision basis to prepare the supply side on the Iberian Peninsula in meeting future demand for LNG bunkering at competitive conditions.”

Fernando Impuesto CORE LNGas hive project coordinator from

Despite LNG fuelled shipping being high on the agenda in the maritime industry, the market drivers are seen to change. From previously being encouraged by a lower price of LNG compensating for the added cost for installation of the LNG fuel equipment, results from interviews conducted by DNV GL indicate a shift towards compliance with emissions regulations to be the main motivation.

The study has revealed a huge potential for LNG as a marine fuel that will utilize the current spare capacity of the existing LNG import terminals. The consolidated quantitative results show that by 2030 up to 2 million m³/y of LNG is to be bunkered by ships (with Algeciras, Las Palmas and Barcelona as most important ports) and by 2050 approximately 8 million m³/y of LNG.

On the logistical side, the market study further concludes that existing LNG terminals will need to develop break bulk capacity to allow for loading LNG to small carriers and LNG bunker vessels. In most ports, development of local intermediate storage capacity needs to be synchronized with increasing LNG demand by larger vessels. Besides bunker stations and local storage facilities, small carriers for delivering batches of LNG to ports over sea will play an important role for the times ahead.

However, in order to realize the predicted LNG supply chain in 2030, about 1 billion Euro of capital expenditures (CAPEX) investment will be needed, adding up to a total cost of 3,7 billion Euro in 2050.

Liv Hovem, Senior Vice President, DNV GL – Oil & Gas, adds: “DNV GL’s market study has clearly shown the major potential LNG has as a fuel in the region. We hope that the conclusions from our study will help ship owners, natural gas suppliers, bunker companies, port authorities and LNG terminal operators gain the confidence they need to move forward with LNG as a fuel for a more sustainable shipping industry.”

Liv Hovem

1. The six-year CORE LNGas hive project is co-funded by the European Commission and is scheduled for completion by December 2020. The CORE LNGas Hive project is to provide recommendations to the National Policy Framework (NPF) with regard to the demand for LNG as a maritime fuel in Spain and Portugal on the deployment of alternative fuels infrastructure. It also aims to provide an investment plan for scaling associated project results. See website here: http://corelngashive.eu/en/

2. LNG can significantly reduce SOx, NOx and particulate emissions, and can also contribute to the reduction of greenhouse gas emissions.

China, EU Bolster Greener Global Shipping to Curb Emissions

Over 200 representatives convened this week at the International Maritime Organization, the United Nations shipping supervisor based in London, to discuss regulation that could turn their industry, currently responsible for as much as 3 percent of the world’s emissions, into a zero-carbon operation by the second half of the century.

The shift toward clean power was prompted by the Paris climate agreement, as well as the threat of regional rules being considered by the EU and tested in China. Europe has proposed a plan to add ship emissions to its trading system by 2023 if the IMO talks don’t succeed. China is piloting a similar program that includes Shanghai’s ports and shipping industry.

The EU proposal “sets a deadline for the IMO to introduce a target and measures,” said Sotiris Raptis, senior adviser to the European Sea Ports Organization and former EU parliamentary adviser. “But it’s a global industry, it’s difficult to regulate emissions generated outside of jurisdiction.”

Imposing emissions would close a loophole left by the 2015 Paris climate agreement. Ship engines almost always burn heavy fuel oil, one of the dirtiest and cheapest forms of energy. IMO members will return to discuss their strategy and level of ambition in October. An agreement could be drafted by next year and implemented in 2023.

|

“We’re seeing that delegates are willing to discuss matters,” said Edmund Hughes, head of air pollution and energy efficiency at the IMO.

The loudest voices at the talks are small Pacific states such as the Marshall and Solomon islands and Kiribati, which are among the most vulnerable to rising seas from climate change. Some islands could be submerged by water as soon as the next decade, prompting them to form a coalition with some EU countries to seek strict IMO emission rules.

“The sector needs to urgently step up its efforts,” said Mike Halferty, transport minister of the Marshall Islands, which has the most ships registered under its flag. “If international shipping was a country, it would have the seventh-largest emissions in the world.”

China & India

China and India, the world’s two most populous nations, submitted a joint document supporting a switch to lower-carbon shipping. Under their plan, countries would be free to create individualized emission reduction plans.

Oil-producing countries such as Saudi Arabia and the United Arab Emirates emphasized that a compromise would be necessary, according to statements on Wednesday that signaled unwillingness to readily agree on proposed measures. Delegates from South American nations including Argentina and Chile said the cost impacts of long-haul trade from geographically-remote ports need to be considered.

“We’re still seeing significant disagreement among major economies over a CO2 reduction target for the sector, but we are hearing clear signals on the need to invest in and develop alternative low carbon fuels and new technologies to accelerate decarbonization,” said Bill Hemmings, director of shipping and aviation at Brussels-based NGO Transport & Environment, who is observing talks at the IMO this week.

Member states are beginning to agree to switch to cleaner fuels, according to Tristan Smith, a lecturer at University College London’s energy institute and former naval architect.

“What we’re seeing for the first time at these talks is a collective focus on alternative fuels,” Smith said. “Previously, member states typically backed efficiency measures. Technology is not the problem, it’s been a political-will problem.”

Norway and Finland are among the leaders in the transition, and have begun to operate ferries with batteries. Lithium-ion pack maker Leclanche SA recently got its 4.3-megawatt maritime battery approved by DNV GL, clearing the way for the market to grow. Royal Dutch Shell Plc is making a big bet on hydrogen to power ships. Emissions-free nuclear propulsion has long been used by warships and ice breakers and the IMO has studied atomic power for cargo vessels.

|

With global trade expected to nearly double by 2030, according to a study by PricewaterhouseCoopers LLP, the task to reign in emissions from shipping -- which carries about 90 percent of the world’s goods -- will become more important. If left unchecked, the industry could account for 17 percent of the world’s carbon emissions by 2050, according to research from the European Parliament.

That in turn would make achieving Paris accord’s goal to keep global warming well below 2 degrees Celsius (3.6 degrees Fahrenheit) even more elusive.

source:www.bloomberg.com

The Tsakos Energy Navigation Ltd (NYSE:TNP) Given Consensus Rating Of “HOLD” By Analysts

Maxim Group set a $7.00 price objective on shares of Tsakos Energy Navigation and gave the company a “buy” rating in a research note on Sunday, May 14th. Jefferies Group LLC reaffirmed a “buy” rating and issued a $6.00 price objective on shares of Tsakos Energy Navigation in a research note on Tuesday, July 4th. BidaskClub raised shares of Tsakos Energy Navigation from a “sell” rating to a “hold” rating in a research note on Thursday, July 6th. Zacks Investment Research raised shares of Tsakos Energy Navigation from a “sell” rating to a “hold” rating in a research note on Thursday, March 23rd. Finally, Credit Suisse Group reaffirmed a “hold” rating and issued a $5.00 price objective on shares of Tsakos Energy Navigation in a research note on Friday, March 17th.

Tsakos Energy Navigation Ltd (NYSE:TNP) has been assigned an average recommendation of “Hold” from the nine brokerages that are presently covering the firm, MarketBeat.com reports. One analyst has rated the stock with a sell rating, three have given a hold rating and five have given a buy rating to the company. The average 12 month price objective among analysts that have covered the stock in the last year is $6.30.

The firm’s 50 day moving average price is $4.44 and its 200-day moving average price is $4.67. Tsakos Energy Navigation has a 52 week low of $3.92 and a 52 week high of $5.59. The stock has a market cap of $429.07 million, a P/E ratio of 13.48 and a beta of 1.69.

Tsakos Energy Navigation (NYSE:TNP) last posted its quarterly earnings data on Friday, May 12th. The shipping company reported $0.16 EPS for the quarter, beating the Zacks’ consensus estimate of $0.12 by $0.04. Tsakos Energy Navigation had a net margin of 9.61\% and a return on equity of 3.40\%. The company had revenue of $108.16 million for the quarter, compared to analyst estimates of $113.51 million. On average, analysts predict that Tsakos Energy Navigation will post $0.43 EPS for the current year.

The business also recently announced a quarterly dividend, which will be paid on Friday, July 14th. Investors of record on Tuesday, July 11th will be paid a dividend of $0.05 per share. This represents a $0.20 annualized dividend and a yield of 3.91\%. The ex-dividend date of this dividend is Friday, July 7th. Tsakos Energy Navigation’s dividend payout ratio is presently 51.28\%.

A number of hedge funds and other institutional investors have recently modified their holdings of TNP. Ameriprise Financial Inc. raised its position in shares of Tsakos Energy Navigation by 49.8\% in the first quarter. Ameriprise Financial Inc. now owns 27,235 shares of the shipping company’s stock valued at $130,000 after buying an additional 9,060 shares in the last quarter. KCG Holdings Inc. raised its position in shares of Tsakos Energy Navigation by 74.6\% in the first quarter. KCG Holdings Inc. now owns 31,543 shares of the shipping company’s stock valued at $151,000 after buying an additional 13,473 shares in the last quarter. Creative Planning raised its position in shares of Tsakos Energy Navigation by 59.1\% in the second quarter. Creative Planning now owns 42,160 shares of the shipping company’s stock valued at $202,000 after buying an additional 15,660 shares in the last quarter. Essex Investment Management Co. LLC raised its position in shares of Tsakos Energy Navigation by 29.9\% in the first quarter. Essex Investment Management Co. LLC now owns 99,023 shares of the shipping company’s stock valued at $474,000 after buying an additional 22,802 shares in the last quarter. Finally, HPM Partners LLC bought a new position in shares of Tsakos Energy Navigation during the first quarter valued at about $484,000. 27.51\% of the stock is currently owned by institutional investors and hedge funds.

Source: MarketBeat

Capital Ship Management Corp. is Selected as a Finalist for Four Categories at the Lloyd’s List Global Awards 2017

Award winners will be announced at a special ceremony on 27 September at London’s National Maritime Museum.

About Capital Ship Management Corp.

Capital Ship Management Corp. (a subsidiary of Capital Maritime & Trading Corp.) is a distinguished oceangoing vessel operator, offering comprehensive services in every aspect of ship management. The Capital Maritime Group currently operates a fleet of 71 vessels with a total dwt of 7.8 million tons approx. The fleet under management includes the vessels of Nasdaq-listed Capital Product Partners L.P.

|

|

|

|

APL reduces CO2 emissions by 48\% since 2009

APL, a unit of CMA CGM, reported its highest reduction in emissions for its fleet in 2016 – 3\% lower than 2015 and 48\% lower than the base year of 2009 –and its seventh consecutive year of CO2 emissions by its fleet.

The line’s emissions were verified by Lloyd’s Register Group according to the Clean Cargo Working Group (CCWG) verification protocol and ISO14064-3:2006 standard.

“APL is pleased to register our best carbon reduction performance as yet, improving our fleet emission level by about 3\%, versus our reduction in 2015. APL prides ourselves as a responsible carrier and will persevere in our pursuits of environmental excellence as we facilitate global trade,” said APL ceo, Nicolas Sartini.

In a target set by parent CMA CGM, APL aims to reduce carbon dioxide emissions per container transported by 30\% between 2015 and 2025.

“APL believes that every stakeholder plays a role in protecting our environment. This is also why our sustainability programmes are being extended to our customers so that they too can make a difference in reducing carbon footprint via their shipments with APL,” Sartini added.

http://www.seatrade-maritime.com

Unmanned ships on the horizon

|

The little craft bearing the DNV GL logo gingerly braves the waves, as it skippers across the Trondheim Fjord under the watchful eyes of Kjetil Muggerud and Henrik Alfheim from the Norwegian University of Science and Technology (NTNU) in Trondheim. Both students are investigating how advanced control systems and navigation software could control an unmanned vessel, using a 1:20 model of DNV GL’s concept vessel ReVolt: “Advances in sensor technology, data analytics and bandwidth to shore are fundamentally changing the way shipping works. And as operations are digitalized, they become more automated,” says Dr Pierre C. Sames, Director of Group Technology & Research at DNV GL.

Governments around the world are looking into unmanned shipping as a way to move more cargo to sea in order to contain the spiralling costs of road maintenance caused by heavy lorry traffic, not to mention air pollution. Norway has taken the lead in exploring innovative ways of tackling this issue and bridging its many fjords and sea passages to ease transit. Cost is a key consideration in all of this. In 2016 government agencies and industry bodies established the Norwegian Forum for Autonomous Ships (NFAS) to promote the concept of unmanned shipping. In support of these efforts, the Norwegian government has turned the Trondheim Fjord into a test bed for autonomous ship trials. Other nations, most notably Finland and Singapore, are pursuing similar goals.

DNV GL is in the midst of this development, following its mission to make sure the technologies enabling autonomous ships will perform to the benefit of humans, their assets and the environment.

The human factor

“If we look at recent advances in driverless car technology, the thought of trying something similar with ships does not appear too far-fetched. After all, water has at least one great advantage: there is less traffic than on roads and reaction times are usually longer,” says Sames.

The DNV GL experts identified three main factors that could positively influence the uptake of autonomous shipping: “Automation reduces the potential for human error. In addition, water transport can be cheaper and more energy efficient than moving goods on land.”

With a battery propulsion system, as seen on DNV GL’s ReVolt model, an autonomous ship would also be lower in maintenance than conventional ships. Additionally, an unmanned cargo vessel would also become more economical, as eliminating the superstructure would save weight and create more cargo space. Furthermore, unmanned ships may be used in hazardous operations, e.g. firefighting, or as stand-by rescue vessels for offshore structures.

Smart sensor technology increases the safety and efficiency of ship operations. Combining data from various sources can provide the crew with an enhanced understanding of their vessel’s surroundings.

Small craft with great ambitions

DNV GL has initiated or is taking part in various projects revolving around ship automation and autonomous control. The ReVolt project is one example; once all aspects of the autonomous control technology are mature, such a design could possibly be built and deployed as a 100 TEU feeder vessel on fixed routes in coastal waters.

Another project with DNV GL involvement, the Advanced Autonomous Waterborne Applications Initiative (AAWA), led by Rolls-Royce, is investigating a wide array of aspects relevant to commercial unmanned shipping – from technical development to safety, legal and economic aspects as well as societal acceptance. “At DNV GL, we are doing a lot of work to understand the potential risks that come with autonomous ship systems in order to set new standards for them,” explains Sames. “We are already working on developing requirements to be able to test and classify unmanned vessels in the future,” he adds.

The Autosea project of NTNU, supported by DNV GL, Kongsberg and Maritime Robotics, seeks to understand the performance of novel sensor systems and the error potential of autonomous control technology, especially collision avoidance. The NTNU scientists are also working on an autonomous craft for Trondheim harbour. The idea is to provide an on-demand ferry service to passengers and bicycles across a channel at the push of a button. Featuring electric propulsion, an induction-charged battery, GPS navigation and an anti-collision system, the craft will carry up to twelve persons. It is intended to function as a cost-saving alternative to building a bridge. A pilot study is planned for this year, and the ferry is expected to start operating in 2018/2019.

In the race to put the first autonomous ship on the water, Rolls-Royce is getting the autonomous navigation and propulsion systems ready for the Fjord1 ferry project, developed by Multi Maritime.

An unmanned multi-purpose utility vessel, Hrönn will start operating in 2018 servicing offshore sites.

Meanwhile two commercial projects are nearing completion: Rolls-Royce is supplying automatic crossing systems for two DNV GL-classed double-ended, battery-powered ferries the Norwegian operator Fjord1 plans to commission in 2018. Both vessels will navigate autonomously under the captain’s supervision, and he has the option to take control at any time. The first ferry will still require human-controlled berthing, while the second one will be able to perform this task automatically as well.

The unmanned offshore vessel Hrönn, under construction at Fjellstrand shipyard for a Norwegian and UK consortium led by Automated Ships and Kongsberg, will also be delivered in 2018. The light-duty, fully automated utility ship will be deployed in a shuttle service for offshore installations but could be used for many other purposes, ranging from research to fish farming operations.

Furthermore, a plan to built the first unmanned and fully-electric container feeder ship was recently unveiled by Kongsberg and the Norwegian fertilizer specialist Yara. After her delivery, Yara Birkeland will initially operate as a manned vessel and start travelling between the Norwegian ports of Brevik and Larvik autonomously in 2020.

The challenges

Overall, autonomous shipping opens up great opportunities for the European shipbuilding and shipping industries. But new competencies have to be built before autonomous ships can become a commercially viable reality. Key research must be done to improve sensor technology, the acquisition of high-resolution ranging data and instrumentation accuracy. Software plays a very important role in this scenario by enabling situational awareness, a prerequisite for automated decision management. "While existing know-how from the aerospace and automobile industries can be leveraged, specific expertise in ship autonomy has yet to be built up," states Sames. The research activities at NTNU, sponsored by DNV GL and industry stakeholders, are instrumental in creating a new generation of highly skilled ship autonomy experts.

Another concern is the operational availability of on-board machinery. No immediate repairs are possible on an unmanned craft so reliability of all mechanical and electronic components is of utmost importance. “In addition, having battery-powered unmanned vessels would eliminate movable parts from the power generation system and make them easier to maintain,” says Sames.

Segments that could see the first autonomous vessels in operation, include ferries or offshore supply vessels operating in coastal areas or smaller cargo vessels operating in short-sea-shipping.

However, the expert cautions that, as yet, there is no legal framework that governs the use of unmanned ships. DNV GL is developing a set of rules, but to avoid potential conflicts with international law autonomous ships will not be able to operate in international waters until the IMO develops appropriate regulations, which will take time. For the deep-sea segments, autonomous shipping is not an option today, says Sames. “These vessels travel distances that go beyond the range of battery propulsion, and they require well-trained crews on board who can respond quickly to any technical issue,” says Sames. “If an unmanned vessel had a technical issue in the Atlantic, it would take days to reach it and fix the problem. This would not be safe or economical,” he adds.

Cargo vessels without a superstructure could one day be controlled from a virtual bridge on land.

Additional crew support

However, advances in automation can benefit all industry segments in some way, even without fully autonomous control. In the future, some ship traffic could be controlled remotely from land-based virtual bridges – with one ship master overseeing several vessels at the same time. “But the most likely scenario is that the technology which enables autonomous ship operations will simply be an additional option for operation – meaning they could be used for specific purposes without fully replacing traditional, manned operations,” Sames suggests. “So for example, autonomous navigation and control systems could support the crew in steering a vessel, increasing safety and optimizing operational efficiency.”

DNVGL.COM

Hellenic Technical Committee of RINA focuses on new environmental regulations and technologies

Co-Chairmen of the Committee, Mr. Theo Baltatzis, General Manager of Technomar Shipping Inc. and Mr. Akis Tsirigakis, General Manager of Nautilus Marine Acquisition Corp., welcomed new members and presented their views of RINA today who continued to increase its existing fleet worldwide and in Greece, now counting over 5000 Ships for about 38 million GT. The RINA marine international network has been growing constantly and currently counts over 170 Offices worldwide. The newbuilding projects of dual fuel Cruise ships (7 ships+3 options of 183,000 GT, 6600 pax each) for Carnival Group (AIDA, Costa Crociere, P&O and CCL) is proceeding and the first ship is expected to be delivered by November 2018.

Stefano Bertilone, Commercial Director Marine, RINA EMEA, gave an overview of the RINA Group and its financial results of 2016, including the acquisition of Edif and the “birth” of RINA Consulting, as well as the actions of the Group in Marine, Energy, Infrastructures, Business Assurance and other of its business areas in the difficult environment of today.

Spyros Zolotas, RINA Area Manager for Greece and Cyprus, referred to the challenges that the Industry is facing worldwide and presented the actions that RINA is putting in place to help its customers. More experts, like surveyors, marine technical support coordinators and business development managers have been employed by RINA Hellas and are at the disposal of its clients so that they face today’s challenges more effectively. This investment on qualified personnel is followed by a significant growth of fleet in Greece and Cyprus which is expected to exceed 7 million GT by the end of the year.

The technical part of the meeting started with an overview of all new Rules and Regulations from IACS and IMO presented by Michael Markogiannis, Piraeus Plan Approval and Technical Support Manager.

Franco Porcellacchia, Vice President of Carnival Corp. & PLC presented the project of Carnival Corporation related to the compliance of their Company to new environmental regulations through the installation of scrubbers on their fleet of Cruise vessels.

Another aspect of environmental compliance though the use of LNG has been offered in the presentation on "Trend in the LNG market" delivered by Pieter van den Ouden, Gas/LNG Safety Expert, Business Development Manager, RINA Rotterdam.

Giorgos Plevrakis, RINA Piraeus Business Development Manager, Marine, offered all latest updates on MRV verification through his presentation titled “MRV Kick-off".

The latest concern on handling big data and related Cyber threats has been elaborated by Stefanos Chatzinikolaou, Piraeus R&D/Innovation Manager, RINA Academy Hellas Manager, in his presentation "From Big Data to CyberSecurity".

The issues presented and discussed, provoked a lot of interest for exchange of views among the members that was continued in a lively atmosphere during the drinks and buffet on the deck of the historical ship until late._

RINA Services S.p.A. is the RINA company active in classification, certification, inspection and testing services.

RINA is a multi-national Group which delivers verification, certification, conformity assessment, marine classification, environmental enhancement, product testing, site supervision & vendor inspection, training and engineering consultancy across a wide range of industries and services. RINA operates through a network of companies covering Energy, Marine, Infrastructure & Construction, Transport & Logistics, Food & Agriculture, Environment & Sustainability, Finance & Public Institutions and Business Governance. With a turnover of over 450 million Euros in 2016, about 3,700 employees and 170 offices in 65 countries worldwide, RINA is recognised as an authoritative member of key international organizations and an important contributor to the development of new legislative standards.

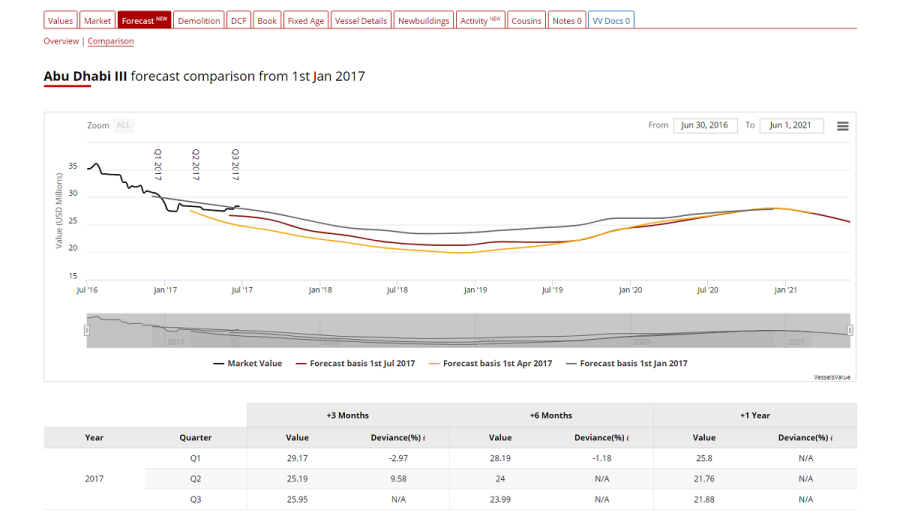

VesselsValue & ViaMar Launch Future Market Values

ViaMar was established in 1996 in Norway by Reidar Sundvor and the late Even Engelstad. They provide objective analysis of shipping markets and employ a fundamental model. Viamar, like VesselseValue, strongly believe that all analysis must be backed up by robust and transparent automated models.

To further this aim, with all forecasts are compared against VV market values in real time to produce live accuracy statistics, a feature no other provier offers. See teh attached image 'Aframax Future Values'.

VesselsValue have been receiving demands from clients are want to use FMV as one input in their scenario analysis work, with many also using DCF, linear depreciation and demolition values as other inputs.

Separately, VV's core banking clients compliance departments are also actively using the new functionality to check values over the tenure of the loan.

About VesselsValue

Following the launch of FMV VesselsValue will be able to provide a complete suite of values, over the lifetime of a vessel. These values are Market, Demolition, DCF, Linear Depreciation, Book and FMV, which are all supported by our other analytical modules VV Trade and VV@ Mapping.

Richard Rivlin, a ship broker with 40 years of buying and selling experience, launched VesselsValue in 2011. The idea for an automated valuation system came about during the financial crash of 2008, when traditional valuation methods were withdrawn from the market.

Today VV has 4 offices – London, Isle of Wight, Stoke and Singapore, employing over 90 people. VV is used by the world’s leading commercial and investment banks, private equity, funds, shipowners and operators, lawyers, accountants and brokers.

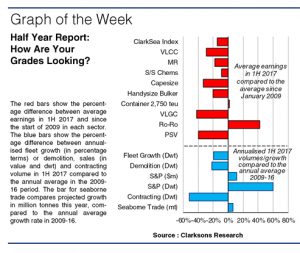

Shipping’s Half Year Report – Any Better This Year?

Don’t Rest On Your Laurels!

A year on from record lows, bulker earnings remain below trend (defined as the average since the financial crisis) but are showing signs of improvement. Capesize spot earnings moved from an average of $4,972/day in 1H 2016 to $13,086/day (75\% below trend versus 33\% below trend). Indeed, based on the first quarter alone, Panamax earnings moved above trend for the first time since 2014 and we have certainly seen lots of S&P activity. The containership sector has responded to the Hanjin bankruptcy with another wave of consolidation (the top ten liner companies now operate 75\% of capacity) and some improvements, albeit with lots of volatility, in freight rates. Improved volumes, demolition and the re-alignment of liner networks, helped improve charter rates and indeed feeder containerships rates have moved above trend for the first time since 2011. Although some gains have been eroded moving into the summer, fundamentals for both these sectors suggest improvements in coming years but it may be a bumpy road!

|

Dropping Grades!

After solid marks in last year’s reviews, the tanker sectors tracked here have moved into negative territory compared to trend, with the larger ships feeling the biggest correction as fleet growth, particularly on the crude side, remains rapid and oil trade growth slows. Aside from a small pick-up in the LNG market in recent weeks, the gas markets remain weak, with VLGC earnings 42\% below trend. Some increased activity, project sanctioning and investor interest has not yet taken offshore off the “naughty step” .

Still Top Of The Class?

The only sector significantly above trend for the first half is Ro-Ro, with rates for a 3,500lm vessel averaging euro 18,458/day, 42\% above trend. There also continues to be strong interest in ferry and cruise newbuilding (the 2 million Chinese cruise passengers last year, now 9\% of global volumes, is supporting a record orderbook of USD 44.2bn, as is the interest in smaller “expedition” ships). We must also give a mention to S&P volumes that are 60\% above trend (51m dwt, up 50\% y-o-y) and to S&P bulker values which improved 25\% in the first quarter alone.

Showing Potential?

Upward revisions to trade estimates have been a feature of the first half, and we are now projecting full year growth of 3.4\% (to 11.5bn tonnes and 57,000bn tonne-miles). Although demolition has slowed (down 55\% y-o-y to 16m dwt), overall fleet growth of 2.3\% is still below trend but an increase on 1H 2016 (1.6\%). While there has been some pick-up in newbuild ordering to 24m dwt (up 27\% y-o-y), this remains 52\% below trend. Last year we speculated on an appointment with the headmaster – still possible but perhaps this year extra classes on regulation and technology?

Source: Clarksons

![]()

Powered by ![]() © Μaritimes 2019

© Μaritimes 2019