-

Home

-

Maritimes NEWS

-

Ports

- maritimes

maritimes

BIMCOs Shipping Market Overview & Outlook - June 2021. Focus: dry bulk and macroeconomics.

Macroeconomics: pandemic disruption hits supply chains as multi-paced recovery takes hold

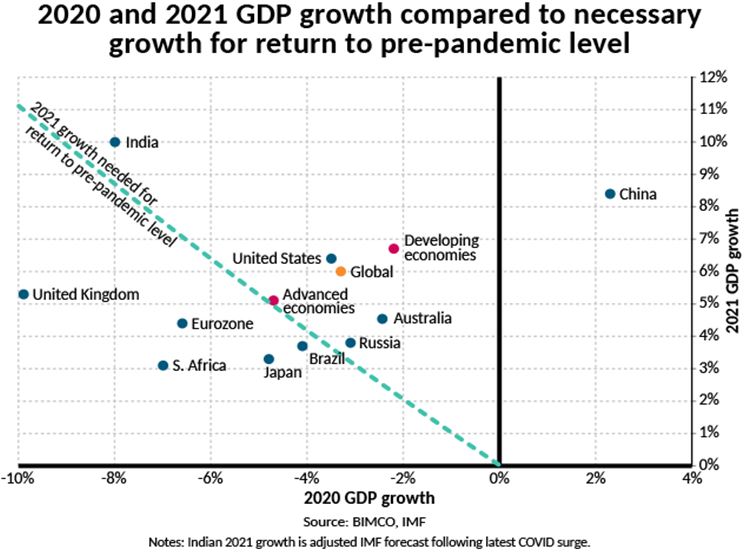

Despite diverging pandemic paths in the world, global growth is forecast to reach 6% this year, according to the International Monetary Fund, following a 3.3% contraction last year. There are, however, still plenty of downside risks, especially as parts of the world are facing their worst coronavirus outbreaks to date and the prospect of a large part of the global population being vaccinated is still a long way off.

Despite diverging pandemic paths in the world, global growth is forecast to reach 6% this year, according to the International Monetary Fund, following a 3.3% contraction last year. There are, however, still plenty of downside risks, especially as parts of the world are facing their worst coronavirus outbreaks to date and the prospect of a large part of the global population being vaccinated is still a long way off.

Even in countries that seem to have the worst of the pandemic behind them, growth this year is expected to vary. China and the US are expected to forge ahead, solidifying their position as the top two global economies, whereas the EU, Japan and the UK are lagging behind and need at least another year to return to pre-pandemic levels.

With the global recovery picking up steam as vaccines are rolled out widely across the developed world, manufacturing activity is picking up, especially in developed economies where it dropped last year, unlike in China where it drove the recovery.

Despite April seeing the highest number of confirmed COVID-19 cases so far, the global manufacturing PMI reached its highest level since April 2010, at 55.8, the tenth month of expansion. The higher PMI is a result of not only rising ouput and new orders – though both of these have been strong (55.7 and 56.7, respectively) – but also longer supplier delivery times and higher input prices as manufacturers struggle to secure all the raw materials they need to keep up with their orderbooks.

The strength of consumer demand for manufactured goods and the unpredictability of the past year has left supply chains under more pressure now than at any other point in this pandemic, as securing the needed inputs has become an increasing challenge in many industries, with delays and temporary factory closures still being announced worldwide.

In the attached report you will find focus sections for Asia, US and Europe.

Outlook for macroeconomics

With the pandemic still raging, the number of daily new confirmed cases and deaths rising, and a geographically very uneven vaccine distribution, the post pandemic world is still some way off. However, despite all the risks the current situation still presents, the richest economies in the world are lifting restrictions, which – if they avoid new surges – will boost their economies.

Although services are picking up in countries where the vaccine roll-out is going well, goods will continue to drive global economic growth. The World Trade Organization forecasts that merchandise trade will grow by 8.0% in 2021 (after a 5.3% drop in 2020), with container and dry bulk shipping both seeing record high volumes so far this year. As long as travel restrictions and social distancing measures remain in place, however, global oil demand, and thereby demand for tanker shipping, will remain far from record levels.

The delays in supply chains that are affecting production around the world will also continue to cause problems for many months to come, as manufacturers scramble to piece together the components needed for their production lines. While a knee-jerk reaction for some will be to look at options for relocating production and increasing protectionism, the solution to a global problem will have to happen on a global scale. Protectionist measures will only complicate the issue.

The delays in supply chains that are affecting production around the world will also continue to cause problems for many months to come, as manufacturers scramble to piece together the components needed for their production lines. While a knee-jerk reaction for some will be to look at options for relocating production and increasing protectionism, the solution to a global problem will have to happen on a global scale. Protectionist measures will only complicate the issue.

As The Economist puts it: “Globalisation is the work of decades. Do not let it run aground”.

Dry bulk shipping: record-breaking start to year drives earnings to decade highs

Demand drivers and freight rates

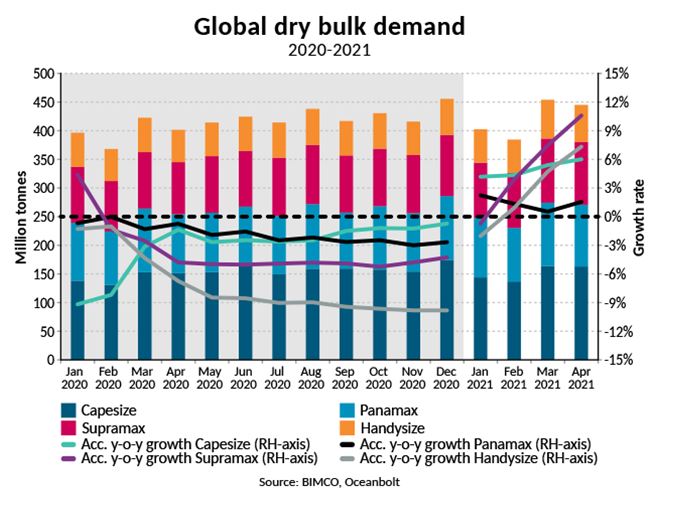

The first four months of 2021 have been record-breaking in volume terms, with demand reaching 1.69 billion tonnes – the highest-ever start to a year. Volumes are up 6.1% compared with the same period in 2020, and only slightly down from the 1.72 billion tonnes in the final four months of 2020. Strong starts to the year for the high-volume commodities of iron ore and coal – thanks to infrastructure-heavy stimulus in some parts of the world – as well as plenty of agricultural exports, have all contributed to the record-breaking start, with strong volumes clearly reflected in dry bulk earnings.

So far, Capesize earnings are on track for the best month of May since 2010, with a daily average of USD 36,536 per day, more than 9 times that of May 2020. The current strength of the market is only underlined by comparing current earnings to peak seasons in past years. The last time average earnings in Q4 were above even USD 25,000 per day was in 2013, and to get above May’s average so far, you have to go back to Q2 2010.

The rest of the market is also delivering strong profits to owners and operators, with Panamax earnings standing at USD 24,903 per day and Supramaxes USD 27,43 per day on 26 May. Even for a 38,000 DWT Handysize ship, earnings are above USD 24,000 per day.

Just as freight rates are up for all ship sizes, the appetite for cargo transport has increased across the board. Supramaxes are the biggest winners, with demand for these soaring by 10.6% in the first four months of this year, compared with 2020. Capesize demand rose by 6.0%, while Panamax edged up 1.5%. Demand for Handysize ships grew the least compared to its pre-pandemic level, up just 0.1% from the first four months of 2019, despite 7.3% growth from the start of 2020.

Focus section on fleet news is found in the attached report.

Outlook for dry bulk shipping

Outlook for dry bulk shipping

So far this year, coal demand has developed differently across the shipping segments. Almost half of all seaborne coal trade happens on Panamax ships where volumes in the first four months of this year fell by 3.6%; meanwhile, coal demand on Capesize ships grew by 6.5% (source: Oceanbolt).

Demand for coal is increasingly coming under scrutiny, especially following US President Joe Biden’s Climate Summit and in the lead up to the COP26 climate summit in Glasgow, which is expected to be held in November. Despite this, concrete targets were few and far between when it came to the largest coal consumers.

At the Biden Climate Summit, China announced its coal consumption would continue to grow over the next five years, albeit at a more limited rate. It then committed to peak its coal consumption in the next five-year plan that runs between 2026 and 2030. With imports making up only a small part of total consumption, given China’s large domestic production, it will be up to the Chinese to decide which source they want to cut down on first. Even if imports are the first to go, a sudden drop is not just round the corner.

Also included in China’s new five-year plan is an increased focus on technology and high-value manufacturing. This indicates a move away from the more traditional construction and heavy industry sectors, potentially lowering demand for some Chinese dry bulk goods over the next few years.

Muddying the water is the deteriorating relationship between China and Australia, although the iron ore trade between the two nations looks to be protected as both are highly dependent on it.

India, the second-largest coal importer, offered even fewer targets on its path to decarbonisation. Coal and lignite feeds 54.7% of the country’s current installed power generation capacity. Other than a pledge to increase its renewable energy capacity by 450 gigawatts by 2030, there was little talk of limiting coal consumption or imports at the Biden summit.

Despite the current strength of the dry bulk market, fundamentally little has changed, with high demand primarily being driven by short-term factors linked to pandemic-related stimulus spending and stockpiling. This means that, even though volumes are currently strong and the orderbook relatively low, BIMCO is not holding its breath for the next supercycle to begin.

Whatever happens in the longer run, the strong start to this year has padded dry bulk owners’ and operators’ bottom lines, and with continued strong demand for many of the major dry bulk goods, this year looks set to be one to remember.

bimco.org

Guidelines to support new carbon intensity cutting measures agreed by working group ahead of MEPC.

An International Maritime Organization (IMO) working group has agreed a set of draft guidelines to support mandatory measures to cut the carbon intensity of all ships.

The proposed mandatory measures have already been approved by IMO’s Marine Environment Protection Committee (MEPC) and are expected to be adopted when the MEPC meets for its 76th session from 10-17 June, 2021.

The proposed amendments to the MARPOL Convention would require ships to combine a technical and an operational approach to reduce their carbon intensity. This is in line with the ambition of the Initial IMO GHG Strategy, which aims to reduce carbon intensity of international shipping by 40% by 2030, compared to 2008.

These are two new measures: the technical requirement to reduce carbon intensity, based on a new Energy Efficiency Existing Ship Index (EEXI); and the operational carbon intensity reduction requirements, based on a new operational carbon intensity indicator (CII).

The dual approach aims to address both technical (how the ship is equipped and retrofitted ) and operational measures (how the ship operates).

The Intersessional Working Group on Reduction of GHG Emissions from Ships (ISWG-GHG 8), which met remotely from 24-28 May, agreed, for consideration by the Committee, with a view to adoption on the following comprehensive set of guidelines accompanying the new requirements:

draft 2021 Guidelines on the method of calculation of the attained energy efficiency existing ship index (EEXI);

draft 2021 Guidelines on survey and certification of the energy efficiency existing ship index (EEXI);

draft 2021 Guidelines on the shaft / engine power limitation system to comply with the EEXI requirements and use of a power reserve;

draft 2021 Guidelines on operational carbon intensity indicators and the calculation methods (CII Guidelines, G1);

draft 2021 Guidelines on the reference lines for use with operational Carbon Intensity Indicators (CII reference lines guidelines, G2);

draft 2021 Guidelines on the operational carbon intensity reduction factors relative to reference lines (CII Reduction factor Guidelines, G3);

draft 2021 Guidelines on the operational Carbon Intensity rating of ships (CII rating guidelines, G4).

The amendments to MARPOL Annex VI and this accompanying detailed set of guidelines provide important tools for Administrations and industry to implement the new requirements, and building blocks for future energy efficiency measures.

CII reduction factor

Under the draft MARPOL amendments, ships of 5,000 gross tonnage and above (the approximately 30,000 ships currently already subject to the requirement for data collection system for fuel oil consumption of ships) have to determine their required annual operational carbon intensity indicator (CII). The ship’s CII determines the annual reduction factor needed to ensure continuous improvement of the ship’s operational carbon intensity within a specific rating level.

Under the draft MARPOL amendments, ships of 5,000 gross tonnage and above (the approximately 30,000 ships currently already subject to the requirement for data collection system for fuel oil consumption of ships) have to determine their required annual operational carbon intensity indicator (CII). The ship’s CII determines the annual reduction factor needed to ensure continuous improvement of the ship’s operational carbon intensity within a specific rating level.

The actual annual operational CII achieved (attained annual operational CII) would be required to be documented and verified against the required annual operational CII. This would enable the operational carbon intensity rating to be determined.

A key element in the draft guidelines is the proposal for the CII reduction factor (the ‘Z-factor’), included in the draft guidelines on the operational carbon intensity reduction factors relative to reference lines (G3).

The reduction rates are intended to achieve the levels of ambitions set out in the Initial Strategy, in particular, the 2030 level of ambition of reducing carbon intensity of international shipping by at least 40% by 2030, compared to 2008.

The group put forward to the Committee the concept of a phased approach, which would see an annual successive carbon intensity reduction rate of -2% compared to the 2019 reference line from 2023 (when the MARPOL amendments would enter into force) through to 2026 – at which time a review required under the draft MARPOL amendments would be undertaken to further strengthen the annual reduction rate.

CII rating

The draft 2021 Guidelines on the operational Carbon Intensity rating of ships (CII rating guidelines, G4) set the method to determine the rating boundaries.

The rating would be given on a scale - operational carbon intensity rating A, B, C, D or E - indicating a major superior, minor superior, moderate, minor inferior, or inferior performance level. The performance level would be recorded in the ship’s Ship Energy Efficiency Management Plan (SEEMP).

Under the draft MARPOL amendments, a ship rated D for three consecutive years, or E, would have to submit a corrective action plan, to show how the required index (C or above) would be achieved.

Administrations, port authorities and other stakeholders as appropriate, are encouraged to provide incentives to ships rated as A or B.

Correspondence group established

The Working Group agreed to establish a Correspondence Group on Carbon Intensity Reduction, to:

further consider and finalize the draft updated Guidelines for the development of a Ship Energy Efficiency Management Plan (SEEMP);

further consider and update existing guidelines, procedures or guidance, including the 2017 guidelines related to the ship fuel oil data collection system;

develop draft guidelines on correction factors for certain ship types, operational profiles and/or voyages for the CII calculations (G5)

develop in new or existing guidelines specific guidance on the audit and verification processes of SEEMP as well as possible parameters and templates for reporting, verification and submission of data for trial CIIs of individual ships on voluntary basis

Attained and required Energy Efficiency Existing Ship Index (EEXI)

The attained Energy Efficiency Existing Ship Index (EEXI) is required to be calculated for every ship at its first survey following entry into force of the amendments. This indicates the energy efficiency of the ship compared to a baseline.

Ships are required to meet a specific required Energy Efficiency Existing Ship Index (EEXI), which is based on a required reduction factor (expressed as a percentage relative to the EEDI baseline).

Review mechanism

The draft amendments would require the IMO to review the effectiveness of the implementation of the CII and EEXI requirements, by 1 January 2026 at the latest, and, if necessary, develop and adopt further amendments. IMO’s Initial GHG Strategy is to be revised by 2023.

MEPC 76

The MEPC 76 session meets in remote session 10-17 June 2021.

Hill Dickinson strengthens team in Greece

Maritime legal specialist Hill Dickinson has strengthened its position in Greece with significant development and new appointments in Piraeus.

Responding to market support and client needs, the firm has unveiled a host of new hires throughout 2020 and 2021, including expert casualty support and a refreshed Marshall Islands and Liberian law service.

In May 2021, Kostas Karachalios joined the Piraeus office as a Senior Associate (from Stephenson Harwood, Piraeus), bringing with him 15 years of ship finance experience advising both banks and borrowers on a wide variety of shipping and ship finance transactions.

In January 2020, the Piraeus and London offices welcomed casualty specialist and partner Ian Teare. Ian joined from Wikborg Rein’s Singapore office where he had been both managing partner and led the casualty response practice for Asia. Following his return to Europe from South East Asia, Ian splits his time between both Hill Dickinson’s London and Piraeus shipping teams and provides valuable additional capacity for marine investigations and emergency casualty response for our clients in the Greek market and internationally.

In August 2020, Vanessa Tzoannos joined the Piraeus office (from Ince, Piraeus) as Of Counsel. Vanessa is the first Greek and European woman to qualify in the Marshall Islands (qualifying in 2019) and her expertise on matters relating to Marshall Islands law is widely recognised in Greece. Vanessa also advises on disputes and transactional matters applying Liberia law and is a leading specialist on economic substance regulations in both jurisdictions.

Additional hires in recent months include Maria Nomicos (from Penningtons Manches Cooper, Piraeus) in January 2020; Maria-Loukia Markantonaki (from Geronymakis & Partners Law Office, Piraeus) in March 2020; Chris Primikiris, who relocated from the firm’s London office to Piraeus in August 2020; Eleni Baxivanou, (from Daniolos Law Firm, Piraeus) in August 2020; Anastasis Voskos who joined in September 2020; Iris Vamvaka who joined in November 2020; Kleopatra Diamanti (from SACH Solicitors, London) in November 2020; Myrto Zioma who joined in December 2020; and Eleni Kachpani who joined (from Argyriadis Law Firm, Thessaloniki) in February 2021.

Combined with the promotions of Anthony Paizes to Legal Director in May 2020 in the Shipping Finance team and Alexander Freeman to Legal Director in May 2021 in the Shipping Litigation team, the depth and breadth of Hill Dickinson’s Piraeus office has developed significantly to support its loyal client base in Greece, Cyprus and the Middle East.

Jasel Chauhan, who heads the Piraeus office and the firm’s International Finance team, said: “The past year has been a turbulent period for the shipping sector – with Covid-19 and Brexit alone having had a huge impact on businesses and personal lives without exception. Investing and developing our team in Piraeus is very much thanks to the continued support of our clients and highlights our long term commitment to the Greek market through difficult times and beyond.”

Tony Goldsmith, who heads the marine business group internationally, added: “Although 2020 brought with it the tragic loss of Patrick Hawkins and the Covid-19 pandemic, the team has shown exceptional resilience and fortitude and has become stronger for it. The phenomenal growth is testament to this, and I am proud to welcome each new member to the Hill Dickinson family and look forward to working closely with them in the years to come.”

About Hill Dickinson

Hill Dickinson LLP is a leading and award-winning international commercial law firm employing 850 people including 185 partners and legal directors, with offices in Liverpool, Manchester, London, Leeds, Piraeus, Singapore, Monaco and Hong Kong. Hill Dickinson delivers advice and strategic guidance spanning the full legal spectrum. The firm acts as a trusted adviser to businesses, organisations and individuals across the globe and from a wide range of market sectors, advising on non-contentious advisory and transactional work through to all forms of commercial litigation and arbitration. Hill Dickinson’s network of international offices reflects the global nature of its work; the Monaco office focuses on the needs of its yacht and superyacht client base, and its offices in Piraeus, Singapore and Hong Kong specialise in the marine, trade and energy markets.

Decarbonizing shipping – why now is the time to act

The shipping industry must reach zero emissions by 2050, and to get there zero-emission ships must become the dominant and competitive choice by 2030.

A zero-emission fleet is only viable if zero-emission energy sources are competitive with traditional fuels, yet there is a competitiveness gap the market cannot solve by itself.

It is critical for shipping's long-term success the International Maritime Organization and member states show progress by adopting regulation allowing shipping to decarbonize in line with the Paris Agreement.

A conversation with a six-year-old will lay to rest any doubts you may have about the importance of tackling climate change. Environmental awareness is the hallmark of our time. While older generations ponder over the “whats” and “hows”, younger ones wonder why so much time goes on debating rather than doing.

The call for tackling climate change is gaining momentum among citizens, investors, companies and countries around the world. US Climate Envoy, John Kerry, recently announced that the US is joining international efforts to achieve zero emissions from international shipping by 2050. And the maritime industry wants to play its part. Since 2019, the Getting to Zero Coalition has been working on making zero-emission vessels commercially viable by 2030 from the perspective of technology, business models, growth opportunities and policy.

For world to decarbonize, shipping must decarbonize

Shipping connects the world by supplying essential goods that society needs to thrive. Whilst this is done with the lowest carbon footprint of any mode of transport per ton transported, shipping is still emitting significant amounts of greenhouse gases. With a sizeable carbon footprint that only shows signs of growing, and a decades-long investment horizon, shipping cannot afford to wait. For the world to decarbonize, shipping must decarbonize.

To stay in step with the needs of society – and thus stay relevant as an industry – now is the time to act. The shipping industry must reach zero emissions by 2050, and to get there zero-emission ships must become the dominant and competitive choice by 2030, when we need to reach 5% zero-emission energy sources in international shipping.

But herein lies a conundrum. A zero-emission fleet is only commercially viable if zero-emission energy sources are competitive with traditional fuels. However, fossil fuels remain readily available, reliable and cheap – and compatible with existing ships and engines – creating a competitiveness gap that the market cannot solve on its own.

New policies are needed, regulating and incentivising shipowners, operators and fuel providers in a direction that drives investments in new fuels and technology to enable a zero-emission fleet. And we need to move the needle now.

3 priorities for the IMO

In shipping, we are fortunate to have the International Maritime Organization (IMO) as the international body regulating our activities, ensuring a level playing field, and an efficient global maritime transport system. It is, however, critical for the reputation and long-term success of our industry that the IMO and its member states demonstrate progress by adopting regulation allowing shipping to decarbonize in line with the Paris Agreement and public expectations.

We are calling on the IMO and the member states to urgently address three priorities:

1. The IMO must align international shipping with the Paris Agreement temperature goal by adopting a target of full decarbonization of international shipping by 2050, when the IMO’s Initial GHG Strategy is revised in 2021 and 2022. This would set a clear direction for the industry – a direction which has already been set for domestic emissions by many of the world’s nations including China, the EU, Japan, South Korea, the UK and the US.

2. The IMO must make progress this year at MEPC 76 and 77 on meaningful measures bridging the competitiveness gap between carbon-based fuels and zero-carbon energy sources. This includes market-based measures setting an adequate price on GHG emissions based on a full life cycle analysis of energy sources. Progress this year is needed to instil confidence across the maritime value chain that such measures will enter into force in 2025 and make the transition to zero-emission shipping investable at scale.

The required price on GHG emissions from international shipping needed to reach 5% zero-emission fuels by 2030 can be significantly reduced if the generated revenue from a market-based measure is used to support the deployment at scale of zero-emission vessels and fuels. This would also help de-risk first movers and make investments in zero-emission vessels and fuel production possible.

3. The IMO must ensure a globally effective and equitable transition to zero-emission shipping. This could be achieved if part of the funds raised through a market-based measure was used to support climate vulnerable countries as well as to support the development and deployment of economically viable zero emission fuels and technologies in developing countries, particularly in Small Island Developing States and Least Developed Countries.

Recent reports from the World Bank show that meeting the future demand for zero-emission shipping fuels will create new growth and job opportunities all around the globe not least in developing countries and emerging economies. This demonstrates that the transition to zero-emission shipping can go hand in hand with sustainable economic growth.

Decarbonizing shipping is possible, but it will require urgent and sustained action by the private sector as well as by governments. Let us move forward together to make shipping a zero-emission industry, so we can be proud of the answer we give a six-year-old, when they ask: “What are you doing to address climate change?”

The signatories to this op-ed are all active in the Getting to Zero Coalition.

https://www.weforum.org/

LR launches Maritime Performance Services Hub in South Europe.

New initiative underpins LR’s global strategy to ensure the safe, sustainable and efficient operations of its clients.

LR has announced the creation of a new Maritime Performance Services (MPS) Hub in South Europe to support shipowners and operators to improve the sustainability and efficiency of their operations, thereby enhancing their competitiveness.

The MPS Hub will act as an umbrella of the recently launched Decarbonisation Advisory Centre and Nettitude cyber-security operations centre, offering the full portfolio of LR’s advisory and software services, enabling clients to improve their environmental performance, facilitate fleet management and optimise the efficiency of their vessels.

The launch underpins LR’s global strategy to support its clients to address two key challenges; reducing business and operational risk and increasing operational profitability, through a combination of professional services and software solutions for fleet management and fleet optimisation.

A dedicated local team of experts with cutting-edge technical knowledge and rich experience of LR’s integrated digital platforms will provide a wide-range of professional services – from technical advisory, fuel testing, condition assessment programmes to emissions modelling capabilities – while support from cloud-based platforms will offer valuable insights for fleet management and fleet optimisation, tailored to specific client needs.

Theodosis Stamatellos, LR South Europe Marine and Offshore Regional Manager, said: “The Maritime Performance Services Hub will provide our South Europe clients with access to aggregated human expertise and digital intelligence, offering efficiency enhancements, cost savings whilst safeguarding operational safety. These are all significant factors in any decision our clients will make to maintain sustainable shipping operations, during this decade of change.”

Andy McKeran, LR Maritime Performance Services Director, commented: “The new South Europe MPS Hub underpins our global strategy to address the key business challenges of our clients and support safe, sustainable and efficient operations. We have chosen to start this initiative in Greece given the influence of its shipowners and operators in successfully navigating maritime industry trends. With uncertainty around the investment decisions that may be required in the decade ahead, a trusted guide is vital and LR takes immense pride in the strong relationships we have with Greek shipowners and operators and we look forward to supporting their competitiveness as they address future challenges.”

About Lloyd’s Register (LR). For a safer world.

Lloyd’s Register is a global professional services organisation specialising in engineering and technology solutions. Our experts advise and support clients to improve the safety and performance of complex projects, supply chains and critical infrastructure. We help to keep the world moving safely, efficiently and sustainably.

Lloyd’s Register is the world’s first marine classification society, created more than 260 years ago to improve the safety of ships. Now our technical expertise is offered in more than 70 countries, by more than 6,000 employees. The surplus we generate funds our shareholder, Lloyd’s Register Foundation, a global charity whose mission is to enhance the safety of life and property. Our independence means we provide reliable, impartial and informed advice.

RINA Hosts Inaugural Hellenic Decarbonization Committee

Athens, May 28, 2021 - As part of its broader decarbonization program, RINA hosted the first Hellenic Decarbonization Committee (HDC) on May 6th, 2021. Chaired by Mrs. Ioanna Procopiou, Prominence Maritime Managing Director, the committee discussed improvements in technology, regulatory changes, digitally enabled services and the potential funding or financing of green technologies to benefit the entire industry. Speakers included senior marine, decarbonization and technical experts from RINA along with a presentation on EEXI/CII and working towards zero carbon from Panos Kourkountis, Technical Director, Seatraders.

Ioanna Procopiou, Chairwoman of the HDC, said, “RINA's initiative has brought different stakeholders of the industry into a constructive dialogue. We were able to share ideas, voice concerns and distinguish between pragmatic and idealistic solutions for shipping when it comes to climate change.”

Giosuè Vezzuto, EVP Marine at RINA, said, “We believe that regulators and the industry have to work in synergy to find viable solutions to decarbonization challenges, and we will work to support the technical strength, innovative vision, and tradition of the Greek shipping sector. This first meeting of the HDC was a positive beginning, as it will continue to work exchanging views, discussing new technologies, and formulating proposals for the industry. Further meetings will be organised with participation of members from RINA’s Decarbonization Committees in other countries to increase multi-sector and multi-competency sharing to maximize the impact of this initiative”.

Spyros Zolotas, RINA Marine Southern Europe & Africa Area Senior Director, added, “This inaugural meeting of the HDC lays the foundation for an intelligent and pragmatic methodology by the shipping industry towards climate change. Our approach must be a combination of technical and operational steps, incorporating digital tools to optimize ship performance. The HDC brings together a great deal of experience across shipyards, engine manufacturers and other main players in the sector.”

Present at the first meeting of the HDC the top management of all founding members: Attica Group, Borealis, Cyprus Sealines, Dynacom, Global Ship Lease, Interunity, Laskaridis Shipping, Minerva, Minoan Lines, M/Maritime, Orion, Prime, Prominence, Roxana Shipping, Seanergy, Seatraders, Stealth, Technomar, Thenamaris and Transmed.

RINA provides a wide range of services across the Energy, Marine, Certification, Real Estate & Infrastructure, Mobility and Industry sectors. With expected net revenues in 2020 of 485 million Euros, over 3,900 employees and 200 offices in 70 countries worldwide, RINA is a member of key international organisations and an important contributor to the development of new legislative standards.

The Greek-owned fleet bolstered the ranks of the European shipping industry

This year marks the 40th anniversary of Greece's accession to the European Union (EU), through which the Greek-owned fleet bolstered the ranks of the European shipping industry. Today, Greek-owned vessels represent 58% of the EU-controlled fleet, being the cornerstone of the European maritime cluster and a strategic asset for the EU, carrying essential goods. The large Greek fleet of tankers and bulk carriers also reduces the EU's energy dependency by securing diverse energy imports. Looking ahead, Greek shipping will continue its essential role, serving European trade and contributing to the EU's economic growth and the welfare of its citizens.

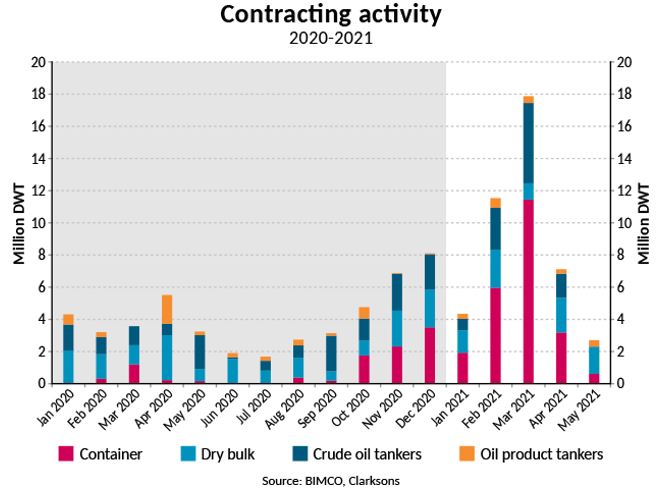

Container ships drive 119% jump in total new orders in first five months of 2021

Total orders of dry bulk, tanker and container ships in the first five months of the year have jumped 119.7% compared with the same period in 2020, primarily driven by record high container ship contracting, as investors in this segment find themselves flush with cash. So far 43.6m DWT of orders have been placed at shipyards, towering above the 19.8m DWT at the start of 2020, when order levels were lower due to uncertainty at the start of the pandemic. In all of 2020, 49m DWT was ordered, a level which is only 5.5m DWT above the level reached in just the first five months of 2021.

Although not matching the staggering growth in container ship contracting, demand for new crude oil tankers has been strong, up 47.4% from the first five months in 2020, despite the freight market being much more profitable than currently. Oil product tankers on the other hand have seen a fall in contracting, whereas dry bulk contracting, despite the strong freight and S&P markets, is only slightly above last year’s level.

“The vast amount of money pouring into container shipping is finding its way into the shipyards, with the current tightness in the supply of ships incentivising some owners to expand their fleets. Although also making good money in the current market, dry bulk owners have been more reluctant to order new tonnage, with the second-hand market proving more popular,” says BIMCO’s Chief Shipping Analyst, Peter Sand.

“The tanker market is split in two. We are seeing a rise in contracting for crude oil tankers, as owners who filled their coffers during the height of the market last year are betting on a better market when the ships are delivered, whereas oil product tankers are proving less popular,” Sand says.

Money from the container freight and charter markets pouring into shipyards

It has been a truly record-breaking start to the year for containership contracting, with 2.2m TEU being ordered. This is more than 12 times higher than the 184,254 TEU ordered in the first five months of 2020 and more than 60% higher than the previous record dating back to the start of 2005.

Norwegian Cruise line to redeploy eight additional ships

-Company’s Great Cruise Comeback to Continue with Planned Resumption of Operations from Highly Sought-After Destinations Around the World -

ATHENS, May 27 – Norwegian Cruise Line (NCL), the innovator in global cruise travel with a 54-year history of breaking boundaries, today announced that it will resume operations from additional U.S. and international ports this fall.

Guests will once again sail aboard Norwegian Breakaway, Encore, Escape, Pearl, Jewel, Sun, Spirit and Norwegian’s Pride of America to explore Hawaii, the Caribbean, Panama Canal, Asia and much more. Earlier this week, NCL also announced its return to Seattle for the Alaska cruise season, with a start date of Aug. 7, 2021. Further redeployments will be announced in the near future.

“When we first welcome our guests aboard Norwegian Jade this July, to cruise the Greek Isles with seven-night itineraries it will be exactly 500 days since our ships last sailed,” said Harry Sommer, president and chief executive officer of Norwegian Cruise Line. “I am so happy that we're finally getting back to what we love the most, and I'm very proud that we continue to redeploy our fleet methodically. We always said we wouldn’t rush to sail again, but that we'd get back to it when we felt we could do so safely while maintaining our incomparable guest experience. Our efforts to resume cruising safely will continue to be slow and steady, guided by the science-backed protocols of our Sail Safe health and safety program and in collaboration with our destination partners as well as with a variety of governing bodies. We cannot wait to see our guests rediscover the world and make memories with their loved ones again.”

NCL will continue its measured approach to redeploying its fleet, working in partnership with destination partners, governing bodies and the leading experts of the Sail Safe Global Health and Wellness Council. The Council will regularly evaluate the robust protocols of the Sail Safe health and safety program and make science-based decisions to protect guests, crew and the destinations it visits. As protocols evolve and are modified and additional information becomes available, updates will be published at www.ncl.com/sail-safe.

About Norwegian Cruise Line

As the innovator in global cruise travel, Norwegian Cruise Line has been breaking the boundaries of traditional cruising for 54 years. Most notably, the cruise line revolutionized the industry by offering guests the freedom and flexibility to design their ideal vacation on their preferred schedule with no assigned dining and entertainment times and no formal dress codes. Today, its fleet of 17 contemporary ships sail to over 300 of the world’s most desirable destinations, including Great Stirrup Cay, the company’s private island in the Bahamas and its resort destination Harvest Caye in Belize. Norwegian Cruise Line not only provides superior guest service from land to sea, but also offers a wide variety of award-winning entertainment and dining options as well as a range of accommodations across the fleet, including solo-traveler staterooms, mini-suites, spa-suites and The Haven by Norwegian®, the company’s ship-within-a-ship concept. For additional information or to book a cruise, contact a travel professional, call 888-NCL-CRUISE (625-2784) or visit www.ncl.com. For the latest news and exclusive content, visit the media center and follow Norwegian Cruise line on Facebook, Instagram and YouTube @NorwegianCruiseLine; and Twitter and Snapchat @CruiseNorwegian.

Tankers: Covid cloud continues to dampen the Dirty Tanker market, whilst glimmers of recovery surface for Clean Tankers

Using VesselsValue Trade, we will assess the current status of the Tanker market, using historical and current AIS derived supply and demand data.

Dirty Tankers: Demand and Rates continue to fall

The impacts of Covid for the dirty Tanker market are still very present as rates continue to deteriorate into May. After making a small recovery towards the end of March, VLCC rates dropped again at the start of May to below OPEX, resulting in over a 100% year on year decline. Alongside weak earnings, crude Tanker demand is also showing few signs of recovery.

Back in early 2020, reduced demand due to Covid19 was in fact supporting the Tanker market, further intensifying the need for floating storage, as refining curtailed and onshore storage reached capacity. However, crude Tanker demand experienced a rapid decline between May and October in 2020 as cargo miles fell to lows not seen since 2016. A Covid related demand slump was finally impacting the Tanker market and 6 months on, things have hardly improved since. To illustrate this, figure 1 shows crude Tanker global daily cargo miles since January 2020. Cargo miles combine actual distances sailed by each vessel and estimates of cargo volumes (number of Containerships) to indicate the true demand for vessels.

Figure 1: Crude Tanker global daily cargo miles (VLCC, Suezmax, Aframax)

This year, crude Tanker cargo miles stayed consistent between January 2021 and March 2021, until they took another blow in mid April when cargo miles fell again to 30.68 DWT bn-NM. This was 9% lower than cargo miles at the same time in April 2020, when Tanker rates were soaring due to a contango oil market and around 10% of the dirty Tanker fleet was being used as floating storage.

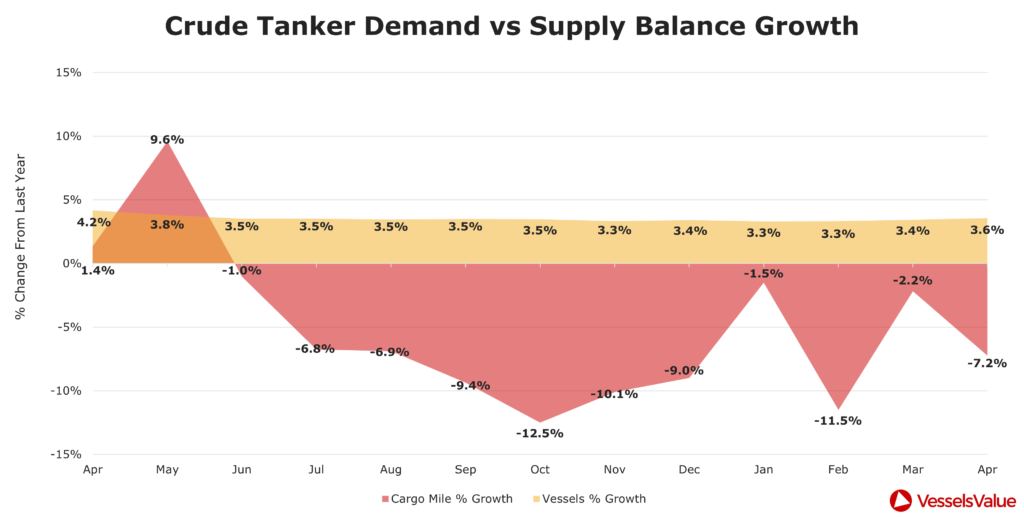

Dirty Tankers: Supply VS Demand

Cargo mile demand can also be compared with fleet growth for insight into market balance. Figure 2 shows the year on year percentage growth change for demand (cargo mile growth) and supply (fleet growth). Since Jun 2020, cargo mile growth has been negative, with the relatively stable fleet growth outstripping demand for the last 11 months.

Figure 2: Crude Tanker Demand vs Supply Balance and Growth

At the lowest point, cargo miles were 12.5% lower in October 2020 versus pre-pandemic levels in October 2019. Despite a large number of scrap candidates, weak cargo mile demand coupled with a crowded VLCC orderbook is expected to prolong the current supply and demand imbalance well into 2021, as the oversupply of available vessels continues.

Dirty Tankers: Routes

Global crude demand is still predominantly being carried by demand in the East, with China being the main consumer, supporting Chinese refiners. crude Tanker demand into South East Asia was confidently growing for the first three months of this year, increasing by 42% between the start of January and mid March. However, demand started on a downwards trajectory into May, falling by 34% between mid March and May. This suggests that even the driving force of crude imports (South East Asia) is still showing signs of volatility.

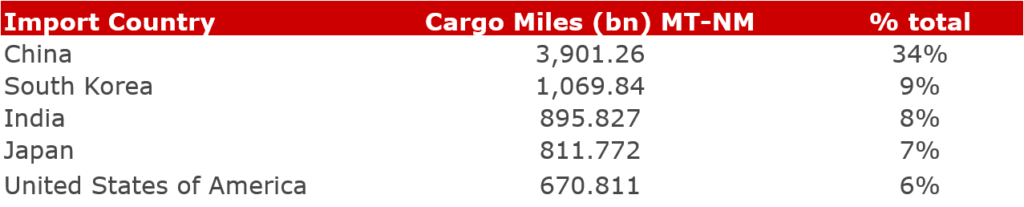

Hopes are that global oil demand must pick up at some point, but these hopes are further threatened by the resurgence of Covid outbreaks in some countries, especially India. India is a significant importer of crude oil, ranking third place for the highest cargo miles in the past year. Global cargo miles into India grew by an impressive 81% between the end of November and mid-December 2020, as the number of Covid cases had declined. Since then, between mid December and May 2021, cargo miles have fallen again by a further 20%, as the number of Covid cases has surged in recent months. Figure 3 shows the top 5 dirty Tanker destinations in the past year.

Figure 3: Top dirty Tanker import countries and cargo miles as a % of total global cargo miles in the past year (VLCC, Suezmax, Aframax)

With nearly 500 crude Tanker journeys in the past year heading into the country, equating to 8% of global cargo miles, the Covid crisis in India reminds us yet again how demand is still being jeopardised by the virus. With strict lockdowns reducing the need for oil and causing operational blocks.

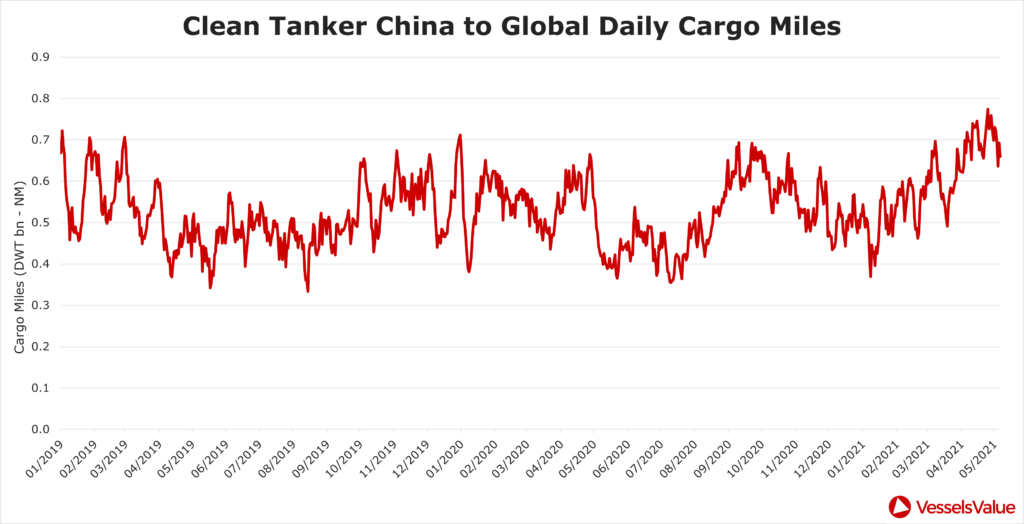

Clean Tankers: Improvement seen in Cargo Miles

The clean Tankers market is by no means out of the woods as Covid unpredictability remains, however, global demand data, coupled with earnings data, shows a slightly more positive picture for the clean market in recent months. MR rates increased rapidly in early May this year, reaching $20,000 per day. This was still 30% lower than rates in May 2020, but 400% higher than earnings at the end of April this year. Figure 4 shows clean Tanker (LR and MR) cargo miles and fleet count over the last year.

Figure 4: Clean Tanker Balance, cargo miles vs live vessels

The chart shows how cargo mile demand recovered well in March after the annual lull in February, reaching 376 bn MT NM. This was higher than cargo miles in March 2019, pre Covid, suggesting that clean Tanker demand could be on the road to a modest recovery, as demand heads in the same direction as fleet growth. In April, cargo miles reassuringly remained high, only falling by 0.5% compared to March. We are also seeing clean Tanker exports out of China increase steadily since January 2021, as Chinese refining ramps up.

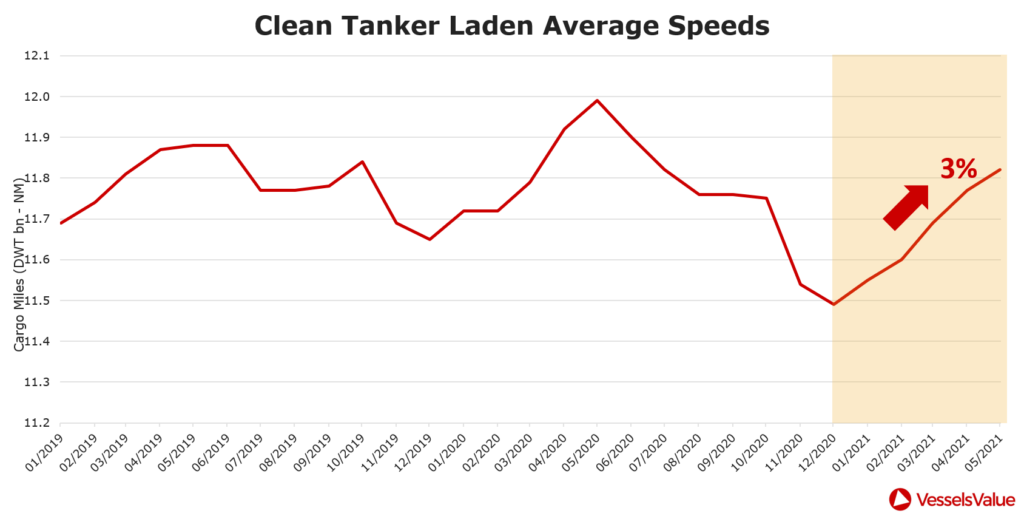

Clean Tankers: Speeds rising

At the same time as improving demand, clean Tanker average laden speeds are also seen to be improving steadily since December 2020. Figure 5 shows clean Tanker laden average speeds since January 2019.

Figure 5: Clean Tanker Monthly Laden Average Speeds

Clean Tanker laden speeds have been increasing month on month since the start of the year, growing by 3% between December 2020 and May 2021. Despite air travel still widely being at a standstill, lockdowns beginning to ease once again has meant that the consumption of liquid fuels such as petroleum and diesel is increasing. Cargo mile demand into North West Europe is a good example, remaining relatively stable since the end of last year when vaccination programmes were started. As vessel demand shows these signs of recovery, vessels are beginning to move faster, now surpassing speeds seen at the end of 2019, which is another indicator that vessel bookings are increasing.

Summary

With the unpredictability of Covid continuing to unsettle global trade, the Tanker market is still suffering the impacts of reduced demand and the reverberations of the floating storage surge this time last year. An imbalance in supply and demand continues across the dirty tanker sector, with a surplus number of vessels on the water, a growing VLCC orderbook and an unknown demand recovery timeline, as one of the world’s top crude importers suffers from a Covid resurgence. On the other hand, the clean Tanker sector is showing some signs of recovery when looking at the demand data. Clean Tanker speeds are increasing and cargo mile demand is rising in line with recent evidence of more promising rates. If the clean Tanker market continues in this direction and we see widespread vaccination success, then we could possibly see a more substantial clean Tanker recovery in Q3 of 2021. However, ultimately, the Covid cloud continues to threaten the Tanker market from both sides.

Trade data as at May 2021

Disclaimer: The purpose of this blog is to provide general information and not to provide advice or guidance in relation to particular circumstances. Readers should not make decisions in reliance on any statement or opinion contained in this blog.

![]()

Powered by ![]() © Μaritimes 2019

© Μaritimes 2019