More Mega-Ships Are a Big Problem for Cargo Carriers

Corrine Png, chief executive officer of research firm Crucial Perspective, estimates freight-carrying capacity on container ships will rise 5.9 percent this year, outstripping demand growth for the first time since 2015.

That’s largely because more than 40 huge container vessels

Greek shipowner newbuilding appetite continues with $1.4bn contracted in 2018

Indeed, over the turn of the year projects involving some 25 vessels surfaced involving a diversified range of ships costing their eight contracting principals over $1.4bn. And just for the record Greek shipping companies invested a confirmed $4.7bn in the acquisition of used oceangoing vessels in 2017.

Spending spree was confirmed when Clarkson Research ranked Greek shipping top in transactions and among the biggest investors in new ships, with total investment exceeding $9.3bn for almost 400 vessels.

The new year dawned with orders revealed for LNG carriers, VLCCs, suezmax tankers, product tankers and kamsarmax bulk carriers featuring the latest in technology. Contracts for gas carriers and kamsarmax bulker led the way.

TMS Cardiff Gas has contracted one 174,000 cu m LNG vessel with WinGD's X-DF low pressure dual-fuel propulsion technology at South Korea's Hyundai Heavy Industries (HHI). There is an option for a second vessel, with some saying there is a second option, in a deal which could run to $500m. The contract follows the Christos Economou-led company being selected as a preferred bidder for two seven-year time charters from Total. Economou said: “We look forward to providing them with first-class LNG shipping services as they continue to expand their LNG activities.”

Peter G Livanos-backed, GasLog has contracted one 180,000 cu m LNG carrier with X-DF propulsion technology. Booked at Korea's Samsung Heavy Industries (SHI) the ship will be ready for delivery in third quarter 2019. It is costing an unconfirmed $197m, with GasLog ceo, Paul Wogan, saying "the vessel has been secured at a very attractive cost and will be equipped with the latest propulsion and cargo containment technology". This order lifts to five LNGs now on order for GasLog, three at SHI and two at HHI.

Evangelos Pistiolis’ Central Shipping group has taken up two suezmax tanker newbuilding berths at HHI with options for two more. The ships are expected to be built at Hyundai Samho Heavy Industries, and cost around $60m each, with the firm ships set for mid-2019.

Dino Caroussis-led Chios Navigation reportedly ordered a 50,000 dwt MR product tanker at Hyundai Mipo Dockyard just prior to Christmas. The Tier II tanker is due for delivery first half of 2019 and is reportedly costing around $33m.

Harry Vafias-led StealthGas is meanwhile being linked to an order for a pair of 80,000 cu m VLGC newbuildings at HHI. Reportedly due for delivery in 2019, the pair, costing around $70m each, are said to be booked on the back of a long term charter to trading house Trafigura.

These orders come on top of a number of orders involving Greek interests that came to light in the latter part of December. Embiricos-controlled Aeolos Management booked a 318,000 dwt Imo Tier III VLCC at Korea's Daewoo Shipbuilding and Marine Engineering (DSME) for delivery in 2020, costing around $84m.

Enesel / NS Lemos contracted a fourth 320,000dwt VLCC at HHI, with delivery from July 2018 through to September 2019. The Tier III VLCCs are reportedly costing just over $80m each.

Lavinia Bulk / Laskaridis booked three 81,500 dwt kamsarmax bulkers plus an option at China's Penglai Zhongbai Jinglu, a deal worth about $100m.

It has also emerged that Alpha Bulkers has turned to China for kamsarmaxes with an order for four 81,800 dwt units at Jiangsu New Yangzi Shipbuilding, delivery in 2018. They are reportedly costing between $24.2m and $24.7m each. It's reported two of the ships will be Tier II and two Tier III, with two flagged in the Marshall Islands and two under the Greek colours.

LNG as a marine fuel – tipping points, step changes, blizzards, and snowballs

One theme that pervaded every month of 2017 for the marine industry was 2020 – the 0.5\% global sulphur cap looms large and has been the source of much debate and conjecture. Although it could be argued that there remain more unanswered questions than definite answers, the momentum behind LNG as a viable, sustainable marine fuel is undeniable.

Orders

Despite an uncertain jigsaw when it comes to the future fuel matrix, prices, and availability, ship owners are continuing to bet on LNG’s potential by ordering LNG-fuelled vessels. A survey conducted by German trade fair organiser, Hamburg Messe and Congress revealed that 44\% of respondents cited LNG as their first choice when contemplating newbuild orders. And evidence shows that this is being acted upon.

Today there are 119[1] LNG-powered vessels in operation with a further 1251 on order. The passenger and cruise segment can be commended for leading the charge and stimulating the demand for LNG bunkers. A headline from Interferry 2017 – “From Ferry-tale to Reality” – captures this sentiment well! This trend continues with Carnival’s seven newbuilds on order, plus newbuildings planned by Royal Caribbean and P&O Cruises, to give just a few examples.

But importantly, this confidence in the future of LNG as a marine fuel is now permeating other segments of the industry too, to cite a few examples; Teekay Offshore Partners has options for two Suezmax-sized, DP2 shuttle tankers, Van der Kamp has a dredger on order, and the OOS Zinlandia – the world’s largest semi-submersible crane vessel – will also be LNG-fuelled. In the US, TOTE Maritime (TOTE), Matson, and Pasha Hawaii, have all announced LNG-fuelled newbuilds. And TOTE announced its partnership with MAN Diesel & Turbo for its retrofit of Alaska trade vessels.

However, what really marks a step change in the evolution of LNG as a marine fuel is that we are now seeing orders for deep sea shipping extending beyond ECAs, for example Sovcomflot has ordered six Aframax tankers, Siem has two transatlantic car carriers on order for charter to Volkswagen, Polaris Shipping confirmed orders for ten, LNG-ready very large ore carriers (VLOCs). Notably, 2017 culminated in a major announcement from CMA CGM, stating that it will power its nine ultra-large container ship newbuilds – due to be delivered from 2020 – with LNG delivered by Total. “LNG is the fuel of the future for shipping,” Rodolphe Saade, chairman and chief executive of CMA CGM was quoted as saying.

Like a game of chess, this decision by CMA CGM is so significant as it tips the balance for so many that may have – until now – been contemplating their next move, waiting to see how the largest industry actors will influence 2020 game plans. Other container lines are now likely to follow suit, as volume brings investment, which expands infrastructure and stimulates supply chains. The snowball effect is inevitable.

Infrastructure

The lack of infrastructure is always top of the list for those citing the largest hurdles to uptake of LNG as a marine fuel. However, this argument is being steadily eroded and it’s fair to say that 2017 represents a tipping point for LNG infrastructure. Indeed, one respected industry publication recently reported “a blizzard of LNG bunkering developments in 2017.” And it certainly seems that way – of the world’s top oil-bunkering ports, nine of the top ten (the exception being Long Beach) offer LNG bunkering or will do so by 2020.

LNG is now readily available in bulk at approximately 150 locations worldwide, and there is a huge bulk LNG infrastructure of regasification terminals and liquefaction plants globally. Of significance, this infrastructure is already well aligned with many deep-sea trade routes. It is the movement of LNG from bulk facilities to the ships, more commonly known as the ‘last mile’, where efforts are being concentrated to enable easy access to LNG as a marine fuel. Ship-to-ship (STS) transfers are a much quicker and more efficient operation than jettyside truck-to-ship (TTS) bunkerings, and by 2018 there will be six LNG bunker vessels in service globally, with four more projects confirmed.

Gas4Sea has the Engie Zeebrugge, its Zeebrugge-based 5,000 m3 LNG bunker vessel that was delivered in April 2017 and the first LNG bunker vessel to enter into operation. In August 2017, Shell took delivery of the 6,500 m3 Cardissa, an LNG bunker tanker that is being operated from Rotterdam. Shell has also announced a cooperation with Anthony Veder on the conversion of the Dutch shipowner’s 7,500 m3 coastal LNG carrier Coral Methane into a bunker vessel, with plans for long-term charters of bunker barges serving the Amsterdam, Rotterdam, and Antwerp (ARA) region in North West Europe and the southeast coast of the US. Skangas took delivery of a purpose-built LNG bunker vessel this summer – the 5,800 m3 Coralius. The Clean Jacksonville is North America’s first ocean-going LNG bunker barge, with a 2,200 m3 fuel capacity. And Titan LNG will introduce its first LNG bunker vessel, the FlexFueler1 pontoon, in mid-2018 to enable the delivery of LNG fuel to vessels throughout the ARA region.

With the majority of LNG bunkering stations currently located in Europe, the region currently dominates the LNG bunkering market with a share of 85\%. But with high marine trade and home to Singapore, the world’s largest bunkering location; Asia-Pacific is expected to catch up quickly. Ports play a crucial role in facilitating this uptick in confidence, not only in relation to infrastructure, but also through incentives. This year, for example, the Maritime and Port Authority of Singapore (MPA) commenced its LNG bunkering pilot project, which provides various companies grants of up to S$2 million per LNG-powered vessel constructed; and in Japan, the Yokohama-Kawasaki International Port has initiated an ambitious LNG bunkering programme.

Future-gazing

Looking ahead, the supply side is gearing up significantly and we are seeing announcements for investments in the next tier of bunker vessels, focused on NW Europe, the US East Coast, China, and Korea. ENN Group, for example, has announced plans to develop an LNG-bunkering hub at Zhoushan, near Shanghai, which includes plans for an 8,000m³ LNG bunker-supply ship. The Wärtsilä built Tornio Manga LNG terminal project in Northern Finland also has plans to provide bunkering for LNG fuelled ships visiting the northern Baltic Sea waters. And with increasing bulk LNG supply capacity from Qatar, the US, Australia, and Russia, new entrants and pressure from existing buyers for more flexible, shorter-term contracts are likely to stimulate the emergence of a more liquid LNG market.

On the regulatory side, we are seeing a push to develop uniform bunkering standards, informed by the work our partner association, the Society for Gas as a Marine Fuel (SGMF), is doing. Striving for harmonisation of regulations on a global level is critical to the long-term success of LNG. Ports, for example, are learning from early adopters, such as the Ports of Rotterdam and Jacksonville, and sharing knowledge and best practice to create uniform local regulation.

The global 0.5\% Sulphur cap provides immediate impetus for the development of LNG as a marine fuel, but as new Emission Control Areas (ECAs), with far tighter local emissions limits, emerge, this stimulus will increase further. ECAs are being considered in areas including the Mediterranean, the Strait of Malacca, Central America, Japan, and Australia. And China is taking a phased approach to the introduction of full ECAs by regulating the Sulphur content of fuels at four locations around their major ports. The introduction of new ECAs supports local and regional uptake of LNG as a marine fuel, and longer term, bunkering infrastructure established in the ECAs is likely to emerge as key hubs for the deep-sea shipping space.

We know that ship owners are looking for certainty on LNG supply and infrastructure, and those developing the infrastructure are looking for people to order LNG-fuelled ships. With so many examples of tipping points and step changes for LNG in terms of both newbuilding orders and infrastructure developments throughout 2017, it seems that the blizzard of change will continue through 2018, with a snowball effect that’s gathering momentum apace towards 2020 and beyond.

As an organisation, SEA\LNG has grown from 13 founding members to more than 30, representing the entire marine LNG value chain, uniting key players including shipping companies, classification societies, ports, major LNG suppliers, downstream companies, infrastructure providers, shipyards, and OEMs. We are proud that our members have been at the forefront of developments during 2017, which will no doubt continue through 2018 and the years ahead.

[1] https://www.dnvgl.com/article/uptake-of-lng-as-a-fuel-for-shipping-104195

https://sea-lng.org

China leads in global shipbuilding industry in 2017

Data released by the British shipbuilding analysis agency Clarkson Research Services shows that in 2017, China took the first place in three indexes measuring the development and capacity of a country's shipbuilding industry: the completion of ships, new orders, and volume of holding orders.

"The completion rate reached 41 percent [of the global market], while the volume of new orders came to 42.4 percent, and our holding orders accounted for 44 percent. I should say that it's not easy to achieve such a level in this difficult situation," said Guo Dacheng, chairman of China Association of the National Shipbuilding Industry.

From the 1950s to the beginning of the 21st century, the three indexes had been topped by Japan or South Korea. In 2010, China exceeded South Korea and ranked first in the world. The record was kept for years until China was surpassed by South Korea in the completion in 2016 and ranked second.

Among the three indexes, the volume of new orders is the most noticeable. The new order China received in 2017 saw a year-on-year growth or nearly 30 percent. The increase reflects an improvement of the quality of China's shipbuilding industry.

For example, currently the largest container vessel ever built is the OOCL Hong Kong, which can carry 21,000 containers. And the record is going to be broken by China as the country has received an order of 22,000 twenty-foot-equivalent-units container vessels.

"It's a process from quantitative change to qualitative change. In the past we imitated and followed others, now we are at the same pace with the entire market. Generally speaking, ship-owners always want their ships to carry more goods with less fuel consumption, so that the operation cost can be reduced to the minimum. So there is no 'best ship type', but only 'the most suitable ship type' according to their needs," said Yu Lai, deputy director of the department of civil ships at MARIC.

Shipbuilders in China have been developing not only productions with high value-added, but also advanced customization service for the customers.

For instance, China has successfully delivered the world's first 33,800-ton smart ship approved by UK's Lloyd's Register of Shipping, as well as the world largest 38,000-cubic meter ethylene tanker, and an offshore ocean farming facility with the largest individual space and the highest automation level at present.

Sources: CCTVPLUS

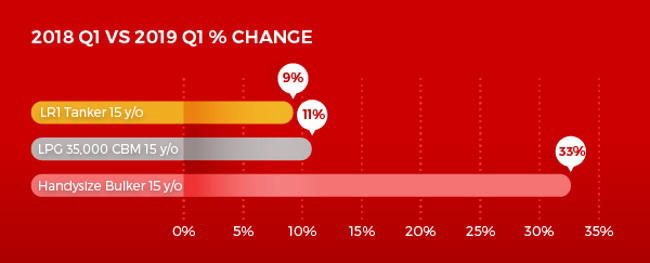

2019 Ship Values – What Types Have The Largest Potential Upside

Topping the list are 15 year old Handysize Bulkers, which are predicted to increase in value by 33\%, from $8.92 million in Q1 2018 to a forecasted value of $9.73 million in Q1 2019.

Coming in second are 15 year old LPG vessels sized 35,000 CBM, forecasted to increase by 11\%, and 15 year old LR1 Tankers are in third place, with a forecasted 9\% increase over the next 12 months.

|

The shipyard crisis deepened in 2017, as deliveries from the yards continued to outpace new orders. Higher steel prices and more ordering dampens the fall in newbuilding prices, and hence second hand prices. Dry bulk has started its cyclical recovery, while tankers are lagging somewhat. This provides renewed demand for shipbuilding and rising newbuilding prices.

|

Source: Vessels Value

Schulte Group acquires LNG ship manager PRONAV

A purchase agreement was signed just before Christmas and is still subject to approval by the German antitrust authority.

Closing of the transaction is expected by the middle of February, a representative of Bernhard Schulte told Fairplay, explaining that the deal put the group in a “top position to exploit further shipowning and ship management potential in the booming LNG market”.

PRONAV was established in Hamburg in 1995 with a clear focus on project development, full technical management, and crew management for LNG carriers.

According to IHS Markit data, it currently has management responsibility for six vessels, four of them operated by Qatargas Liquefied Gas and two of them by Rasgas: Al Ghariya, Al Ruwais, Al Safliya, Duhail, Milaha Qatar, and Milaha Ras Laffan.

The two operating companies under the PRONAV brand, Consulting/Crew Management and Ship Management, were sold for an undisclosed sum by their managing owners Karl-Wiegand Braun, Jan Karl Themlitz, Kai Ramming, Klaus-Peter Stahl, and Vili Vrenko.

The Schulte Group representative told Fairplay that PRONAV would continue operating with about 30 shore-based staff as an independent entity within the group for the time being. Strategic options including integration with the group’s third-party management division, Bernhard Schulte Shipmanagement (BSM), are going to be reviewed over time.

PRONAV says on its website that it performed more than 2,100 LNG carrying voyages, with 4,200 cargo transfer operations during the first two decades since its launch.

Its acquisition adds major competence to Bernhard Schulte in a business area destined for significant growth.

Schulte already provides various third-party management services to 23 LNG tankers and has invested in one owned LNG bunker vessel and one owned LNG carrier with a capacity of 174,000 m³. Both are still under construction.

source: fairplay.ihs.com

2017 Review: How Are The Year End Stats Looking?

But challenges in the tanker, gas and offshore markets continue while uncertainty around environmental regulation builds. As ever, it’s been an interesting year!

ClarkSea Pick Up…

After its all time low in 2016, the ClarkSea Index, our indicator of vessel earnings, rose by 14\% y-o-y to average $10,768/day. Some welcome relief but still 10\% below the trend since the financial crisis and compared to OPEX of $6,394/day for the same basket of ships. It was also a year of contrasting fortunes across markets, especially ‘wet’ and ‘dry’.

Different Trajectories…

With overall earnings down 35\%, the tanker market continued its ‘wind down’, struggling to absorb 5\% fleet growth despite good developments in long-haul trades out of the Atlantic. Supportive fundamentals did flow through into an improving bulker market, with good first and fourth quarters helping rates jump by an impressive 77\% y-o-y. The containership market seems to have picked itself up from the ‘shock’ of Hanjin’s collapse, with consolidation, improved but volatile freight rates and increasing charter rates and S&P prices (see next week for more detail). The gas markets have had to ‘tough it out’ but perhaps there is some ‘light at the end of the tunnel’, especially for LNG where trade grew by an encouraging 11\% in 2017. The cruise and ferry markets had ‘solid’ years but the car carrier market had to wait until the end of the year for only marginal improvements. In offshore, increased FID and rig tendering and an improved oil price have been helpful but deep challenges remain. Offshore owners in a position to do so have been eyeing consolidation opportunities, especially in the rig sector, and S&P ‘bargains’. Overall some mixed trajectories but on balance encouraging signs.

Trade Surging…

After a sluggish few years, an improving world economy helped global seaborne trade to bounce back strongly in 2017, growing by 4.1\% to 11.6bn tonnes, the fastest rate of growth since 2012. Demolition fell back to 35m dwt (tankers up 348\% and bulkers down 50\%) but trade still outpaced fleet growth (3.3\%).

An S&P Record…

In our review of 2016, we reported it was ‘buy, buy, buy’ in the bulker market and during 2017 investors also placed containerships and tankers in their sights. In overall tonnage terms, 94m dwt represents an all time record, with boxships joining bulkers at record levels. Bulker S&P prices made excellent gains (a 5 year old Capesize up 38\%), as did containerships but tanker gains were more modest. Greeks again topped the buyer (and seller) charts, followed by the Chinese (although German owners were the biggest sellers of containerships). Scrap prices moved up by over 40\% to north of $400/ldt for the first time since 2013.

Watching The Yards…

After the 30 year ordering low of 2016, orders increased to 73m dwt in 2017, significant but still 24\% below the average since the financial crisis. China returned to the top of the output charts, with a 39\% share of deliveries, followed by Korea (32\%) and Japan (21\%). Delivery volumes were steady, although we expect them to decrease this year, while the overall orderbook declined 13\% to 197m dwt of $233bn. As ever, it’s been an interesting year.

Source: Clarksons

Greek minister hails Sino-Greek cooperation in new upgrade projects at Piraeus port

Work has started to upgrade the harbor ahead of the arrival of the new floating dock "Piraeus III", at the end of February, in a project that the managing company, China COSCO Shipping, launched last June, Greek national news agency AMNA reported.

Since China COSCO Shipping acquired a majority stake in Piraeus Port Authority (PPA) and took over the management in 2016 after winning an international tender, the image of the harbor is rapidly changing.

The new works includes dredging the harbor to create up to 20 meters of operating depth, providing new electricity and water supply networks, and installing four mooring buoys for anchoring ships.

The new floating repair dock -- 240 m long, 45 m wide, 22,000 tons lifting capacity and full crane equipment -- will be able to service ships with a capacity of 80,000 tons.

"The projects that have started at Perama and will proceed with the lifting of two wrecks off Pier II by the Shipping Ministry, so that the infrastructure for the installation of PPA's large floating dock can be created, show how smoothly the cooperation of the Greek government with the investors is progressing," Kouroumblis commented.

"They also show that the Shipping Ministry's policy will continue to facilitate any development activity stemming from COSCO's contractual obligations regarding bureaucracy and other obstacles," the Greek official told Xinhua.

"At the same time, we support workers' rights by welcoming the latest agreement between employees and the PPA for the signing of a Collective Labor Agreement," the minister said.

Shipping officials have said that ships will no longer need to carry out repair and maintenance operations in other Mediterranean shipyards, while this move is also expected to create new jobs in the Greek market.

The latest projects at Piraeus have received a warm welcome by representatives of the market.

Speaking to Xinhua, George Koumpenas, vice president of operations at Celestyal Cruises, welcomed the works as a very positive development, in particular for companies managing passenger ships operating in the region as well as for the Greek shipbuilding industry.

"In recent years, due to a lack of suitable dock sizes, companies have been obliged to dock our vessels to neighboring countries such as Malta, Turkey and Croatia. This has resulted in the loss of significant revenues for the national economy," he explained.

"The installation and operation of a large floating dock will help maintain and develop the shipbuilding industry in the wider Piraeus and Perama areas, as an important criterion for the choice of the port for seafaring companies is the ability to make repairs," Koumpenas stressed.

XINHUA

Maria Spiliopoulou

BSM supports innovative minds

|

BSM participated at the semi-finals and Grand Final, the latter taking place during October in Limassol with Johann Schulte being part of the judging panel. The two-day event attracted more than 550 people from business, investment and academic fields worldwide and showcased the next generation of successful start-ups.

Elena Pantazidou, BSM Director - HR Shore, emphasised that we are facing serious environmental and social challenges that are destabilising our quality of living, which is why BSM is sponsoring ClimateLaunchpad to bring people together to tackle these issues with entrepreneurial solutions.

http://www.bs-shipmanagement.com

TMS CARDIFF GAS announces time charter with TOTAL for seven years and places Newbuilding orders of X Carrier Series of LNG ships

The vessel will be built to the highest industry specifications, as per TMS Cardiff Gas standards.

This order marks the Company’s further expansion into the LNG sector with secured term employment upon delivery. The Company maintains its appetite for further growth in the sector, which is reflected by the additional capacity made available with optional vessels for delivery in 2020 and 2021.

Christos Economou, Founder of TMS Cardiff Gas, commented: “We are delighted to secure a new long-term time charter with TOTAL, one of the leading global energy companies. TOTAL is an important customer for TMS Cardiff Gas and we look forward to providing them with first class LNG shipping services as they continue to expand their LNG activities.”

About TMS Cardiff Gas Ltd.

TMS Cardiff Gas, established in 2011, is an operator and manager, with a fleet of 10 modern Gas Carriers (six LNG carriers and four VLGCs).

Visit the Company’s website at www.tms-cardiffgas.com

![]()

Powered by ![]() © Μaritimes 2019

© Μaritimes 2019