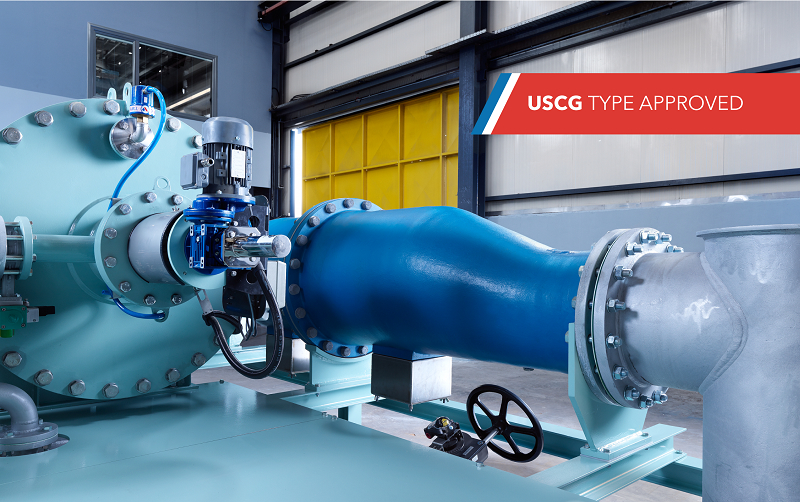

Golar LNG signs agreement with Erma First to install BWTs

|

The first installations of ERMA FIRST BWTS is expected to take place during the company’s next dry-docking scheduled for the second quarter of 2018. The installation of the system will continue until the end of 2022 following the shipping company’s dry-docking schedule.

Golar LNG has worked intensively with ERMA FIRST over the previous months to optimize and adapt the individual systems to the company’s vessels.

“We decided to install ERMA FIRST BWTS, which is designed and produced in Greece, starting at an early stage which provides us with certain commercial and financial advantages, including availability of equipment, minimization of downtime, unrestricted worldwide trading in the following years and the financial benefits of a block order,” OISTEIN DAHL, COO AT GOLAR LNG

ERMA FIRST BWTS became the first full flow electrolysis system, that received the United States Coast Guard (the USCG) type approval certificate in October 2017.

The Ballast Water Management (BWM) Convention entered into force on September 8, 2017. The United States Environmental Protection Agency (EPA) had adopted a similar regulation for ballast water treatment which became effective on January 1, 2016.

Under the rules of the IMO convention, all ships engaged in international trade are required to manage their ballast water to avoid the introduction of alien species into coastal areas, including exchanging their ballast water or treating it using an approved ballast water management system.

ERMA FIRST BWTS FIT is an advanced modular system developed to exceed all special installation requirements either for New Building vessels or any retrofit projects. Covering an extensive capacity range of 50-3740 m3/hr, ERMA FIRST BWTS FIT is a simple solution suitable for all types and sizes of vessels. The major components of the system are a high-end backwash filter and an electrolytic cell with outstanding performance under the most demanding conditions. The self-cleaning automatic screen filter has a nominal filtration rate of 40 microns. For the de-ballasting of the vessel there is no need to use the system; It is completely by-passed and the water can be discharged directly overboard, after neutralization where applicable, with considerable gains in energy saving for the operators/managers of the vessel. Using an active substance that is produced by the method of electrolysis, any danger for re-growth of microorganisms is eliminated.

ERMA FIRST’s design simplicity and expertise on delivering challenging projects, has been well acknowledged by many ship-owners and operators who have already trusted the company with their newbuilds and retrofit installations. Nowadays, ERMA FIRST has a prestigious reference list comprised of ship-owners and shipyards worldwide such as in Greece, China, Italy, Turkey, Romania, Japan, Korea, US, Denmark, UK, Germany.

About ERMA FIRST

ERMA FIRST S.A. was established in 2009 by a team of specialists with strong background and expertise in waste and water treatment technology in Marine applications. Driven by the maritime needs and regulations, and monitoring the Environmental Protection challenges, the company started designing and manufacturing ballast water treatment systems. Being successfully tested in the most prominent test facilities, ERMA FIRST systems are certified and have been awarded prizes for technological achievement many times through the years. ERMA FIRST technology uses a 40 μm filtration followed by efficient full flow electrolysis.

hansbuch.dk

RBS Slims Down, Ships Out of London Office Where Big Bosses Sit

The bank will leave the 280 Bishopsgate building by the end of 2019, moving staff up the road to 250 Bishopsgate, where modernization work will begin later this year, an RBS spokesman said by email. Ultimately, the bank plans to sell the vacant building, which it has occupied since 2002.

RBS no longer requires as much space as it becomes a smaller, more U.K.-focused bank that encourages more flexible working practices, the spokesman said. The Telegraph newspaper reported the plan to vacate 280 Bishopsgate earlier.

RBS, which is headquartered in Edinburgh, has slashed the amount of office space it occupies in London as it slims down in the wake of the global financial crisis. The bank already vacated the 135 Bishopsgate building across the street from the executive office and sold an adjacent site called Premier Place last year. It previously exited a large office on the south bank of the River Thames and sold another property in the Aldgate district in 2015.

An increase of 19.13\% was reported at the Car Terminal of PPA S.A.

recording an increase of 19,13\%. 331,832 were transhipment vehicles, which afterwards were transhipped to other ports in the Mediterranean, increased by 22,07\% compared to 2016, emerging the port of Piraeus as one of the biggest terminals for car traffic across the Mediterranean.

As the Chairman and CEO of PPA SA Captain Fu Chengqiu stated at the

inauguration ceremony of the new offices at Car Terminal:

"Our target is the further increase of throughput at the Car Terminal through the expansion of existing infrastructure and the upgrade of our services”.

Navios Maritime Partners L.P. Announces $22.0 million Acquisition of Two 2006-built Panamax Vessels

Based on the existing charters of the vessels ($9,375 net per day until May/November 2018 and $9,844 until March/August 2018, respectively) and the current rate environment (Clarksons’ 1-

year time charter rate for Panamax vessels as of January 19, 2018), the vessels are expected to generate approximately $4.8 million of EBITDA for the first year, assuming midpoint of

redelivery from charterers, operating expenses approximating current operating costs and 360 revenue days.

Navios Partners is expected to finance the acquisition with cash on its balance sheet and $14.3 million bank debt maturing in 2023 and bearing interest at LIBOR plus 300 bps per annum.

Fleet Update

Following this acquisition, Navios Partners controls 38 vessels.

About Navios Maritime Partners L.P.

Navios Partners (NYSE: NMM) is a publicly traded master limited partnership which owns and operates container and dry bulk vessels. For more information, please visit our website at

www.navios-mlp.com.

Drewry’s Global Reefer Freight Rate Index increases for 4th consecutive quarter, as shipping lines gain control of shippers’ purses

“The recent wave of carrier consolidation, which will continue well into 2018, is having a direct impact on global market structure,” said Stijn Rubens, senior consultant at Drewry Supply Chain Advisors. “As shipping lines gradually regain control of prevailing freight rates, the markets are becoming increasingly tight with behaviours one would more commonly associate with oligopoly conditions. The recent drop in investment in reefer containers only lends further weight to our expectations of further rate increases during 2018.”

|

Drewry’s Global Reefer Freight Rate Index reveals four quarters of uninterrupted increases in global average reefer freight rates.

“With this market context in mind, supply chain professionals should ask themselves two key questions; firstly, am I paying too much for my reefer container shipments in terms of how the rates I have secured compare to my competition and secondly, how do I lock-in the most favourable terms going forward,” added Rubens. “Answers to both questions are provided to members of our exclusive Reefer Benchmarking Club.”

Source: Drewry

Capital Ship Management Corp. and Liberty One announce new Joint Venture: “Capital Liberty Invest” To Focus On Container Ships

The Joint Venture commenced operations in January 2018 and is based out of the Liberty offices in Leer and headed by Liberty CEO, Dietrich Schulz.

Capital Maritime & Trading Corp., CEO Gerry Ventouris emphasized the benefits of the Joint Venture: “I am pleased to see Capital join forces with Liberty. I hold Mr. Schulz and his company in high esteem and I believe that through our Joint Venture, we will be able to provide quality ship management services and asset trading platforms to the German market and beyond.”

CEO Dietrich Schulz of Liberty is delighted to start the partnership with Capital: “This Joint Venture will provide us with an expanded capability to offer a range of services to stakeholders in the German shipping market and across different shipping segments and sizes. I am personally delighted to work with such an established shipping company as Capital Ship Management Corp., which enjoys an excellent reputation in global shipping markets.”

Capital Ship Management Corp. (‘Capital’) is a distinguished oceangoing vessel operator, offering comprehensive services in every aspect of ship management. Capital and its affiliates currently operate a fleet of 74 vessels including 49 tankers (14 VLCCs, 5 Suezmaxes, 2 Aframax, 27 MR/Handy product tankers and 1 small tanker), 6 bulk carriers (4 modern Capesize and 2 handy bulk carriers) and 19 container vessels (15 Post-Panamax and 4 feeder container carriers) with a total dwt of 9 million tons approx. Capital is a subsidiary of Capital Maritime & Trading Corp. The fleet under management includes the vessels of Nasdaq-listed Capital Product Partners L.P.

Liberty is a one stop shop for the maritime industry. Designed to combine amongst others shipmanagement by Liberty Blue, experience in asset trading and a strong standing in the German shipping market.

Source: Capital Ship Management Corp.

Diana Containerships Inc. Announces the Sale of Two Post-Panamax Container Vessels

The Company expects the Vessels to be delivered to the buyer at the latest by March 30, 2018. The unaffiliated purchaser of the Vessels is the same party with which the Company entered into a previously announced agreement to sell up to seven vessels, subject to the purchaser arranging financing. The Company has been advised by the purchaser that such financing has not been arranged and, concurrently with the sale of the Vessels, the Company and the purchaser have agreed to terminate all rights and obligations under the prior agreement.

The Company expects to use the net proceeds from the sale of the Vessels to repay indebtedness under its previously announced credit agreements.

Upon completion of the aforementioned sale, Diana Containerships Inc.’s fleet will consist of 9 container vessels (4 Post-Panamax and 5 Panamax). A table describing the current Diana Containerships Inc. fleet can be found on the Company’s website, www.dcontainerships.com. Information included on the Company’s website does not constitute a part of this press release.

About the Company

Diana Containerships Inc. is a global provider of shipping transportation services through its ownership of containerships. The Company’s vessels are employed primarily on time charters with leading liner companies carrying containerized cargo along worldwide shipping routes.

Shipbuilding In 2017: Any Signs Of Improvement?

Some sectors saw improved contracting activity, while deliveries remained relatively firm, but shipbuilders will be looking to see more positive changes before predicting a return to better times.

|

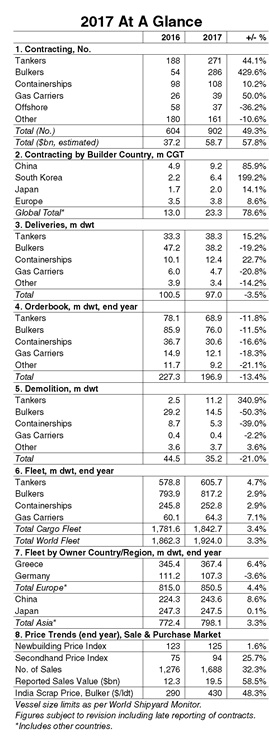

Although contracting began to pick up last year from record lows in 2016, when only 604 vessels were ordered, shipbuilders continued to face difficult conditions in 2017. Just 902 orders of 72.8m dwt were reported globally, only the third year in the past twenty in which less than 1,000 new orders were reported. Of the major sectors, bulkcarrier orders saw the biggest uptick, with 286 vessels contracted last year, although this remained subdued compared to historical levels. Driven by large crude units, tanker contracting increased to 271 vessels, but fell well below the level of ordering in 2015. Meanwhile, the boxship newbuilding market showed fewer signs of improvement and just 108 units were ordered. Gas carrier and ‘ship-shaped’ offshore ordering was also limited, with just 39 and 37 contracts reported respectively in 2017.

Fighting For The Spoils

Chinese builders won the largest share of orders last year, picking up the majority of bulker orders and taking 9.2m CGT in total. Ordering at Korean yards improved on record low 2016 levels, but remained limited at 6.4m CGT, while reported contracting reached 2.0m CGT at Japanese yards. The strength of cruise newbuilding continued to benefit European shipbuilders, which accounted for 38\% of global estimated contract investment in 2017 in value terms, though many yards operating outside of the cruise sector struggled.

Orderbook On The Slide

While it began to stabilise towards the end of 2017, the size of the orderbook declined 13\% in dwt terms in the full year, to reach 3,158 units of 196.9m dwt. This is the first time the orderbook has fallen below 200m dwt since 2004, accompanied by a decline in the number of ‘active’ yards (those with at least one vessel of 1,000+ GT on order) from 440 at the start of 2017 to 360 as of start 2018.

World Fleet Still On The Up

Although contracting remained limited in 2017, shipbuilders continued to deliver a steady volume of tonnage. Total shipyard output reached 97.0m dwt, although ‘non-delivery’ of the scheduled start year orderbook was still significant at 30\% in dwt terms. However, given the smaller orderbook, deliveries are currently projected to decline by around 20\% in tonnage terms in 2018. After a strong start to the year, total demolition activity in 2017 declined by 21\% in tonnage terms to total 35.2m dwt. This left overall fleet growth relatively steady at 3.3\%, slightly faster than the previous year but well below pre-2015 levels. The total world fleet stood at 1,924.0m dwt at the end of the year, with fleet growth remaining firm in the gas carrier and tanker sectors.

Hope On The Horizon?

With output set to decline following multiple years of weak contracting, shipbuilders will be hoping that the moderate upward trend in orders last year accelerates in 2018. Capacity reductions remain ongoing, but many shipyards are still hungry for new orders. Although contracting activity has picked up slightly, conditions remain difficult, and shipbuilders will be hoping for further signs of market improvement in the coming year.

Source: Clarkson

PPA S.A. presented its proposals for the Master Plan of the Port of Piraeus

The compilation of the Master Plan for the development and operation of the Piraeus Port was made according to:

(i) all the Laws and regulations of general implementation, together with all the existing applicable regulatory rules

(ii) the methodology and specifications quoted in the “Specifications of Master Plan” document

(iii) regulations and guidelines for the establishment of Program Design as listed in ANNEX 6.2 of the Concession Agreement 2016.

The target is the correct Planning of the future development of the Port in pursuit of the techno-economic data related mainly with the enhancements included in the development plan. The timeframe covers the period 2016-2021 and aims in the compilation of an appropriate design of facilities in order to maximize the service potential and minimize the loss of space and utility. The Plan also defines the maximum allowable limit of the port zone, the allowable infills, the land use, the construction restrictions, traffic arrangements and every other necessary element for the service of the operation and the safety of the Port.

The ultimate goal is for the Piraeus Port to be set as a worldwide transportation hub emerging in this way the development of Greek economy in general.

The consultation attended: The Deputy Governor of Piraeus Prefecture Mr. Gavrilis G., the Mayor of Piraeus Mr. Moralis Y., The Mayor of Keratsini-Drapetsona Mr. Vrettakos Ch., the Mayor of Perama Mr. Lagoudakis Y., the President of SEEN Mr. Sakellis M., the Harbor Master Mr. Leontaras K., the President of the Union of Captains Mr. Tsikalakis M., representatives of the Naval Chamber, the Αthens Chamber of Commerce and Industry, the Chamber of Small and Medium Industries, the Piraeus Traders Association, the Shipping Agents, the Trade Unions and other institutions.

All the parties participating in the consultation will send their proposals for the final compilation of the Master Plan.

Greek companies are becoming larger and newer

![]()

Powered by ![]() © Μaritimes 2019

© Μaritimes 2019