Poseidon Med II event in Patras highlights the benefits of LNG as fuel and its prospects for sustainable development in Western Greece

|

The scope of the event was to offer a platform of discussion with local stakeholders focusing on the deployment of LNG as an alternative marine fuel and its key envisaged impact on the protection of the environment and on sustainable energy development at Western Greece. During the meeting, specific emphasis was given to the LNG bunkering installations in Patras Port which are designed within Poseidon Med II framework, as well as to safety aspects and global best practices and case-studies. Additionally, the monitoring of air emissions in ports and the establishment of Revithoussa terminal as LNG hub for the regional supply chain were also highlighted.

Nikos Kontoes, President & Managing Director of Patras Port Authority, noted: “Patras Port Authority sets as high priority the LNG establishment in port. At initial stage, it will accommodate LNG bunkering operations, expandable for industrial and domestic use. Within Poseidon Med II, the installation is designed in full alignment with the strict provisions of SEVESO Directive. This LNG unit will contribute to the sustainable development for the port of Patras, linking the currently isolated Western Greece with energy networks. Social-economic development and employment are among the key benefits for Western Greece, which is the third poorest region in Greece, as well as the environmental protection for the port of Patras and the wider area”.

Similar events raising awareness about the prospects of the LNG as marine fuel will take place at other ports participating to Poseidon Med II project the following months.

What is Poseidon Med II project?

Poseidon Med II project is a practical roadmap which aims to bring about the wide adoption of LNG as a safe, environmentally efficient and viable alternative fuel for shipping and help the East Mediterranean marine transportation propel towards a low-carbon future. The project, which is co-funded by the European Union, involves three countries Greece, Italy and Cyprus, six European ports (Piraeus, Patras, Lemesos, Venice, Heraklion, Igoumenitsa) as well as the Revithoussa LNG terminal. The project brings together top experts from the marine, energy and financial sectors to design an integrated LNG value chain and establish a well-functioning and sustainable LNG market.

from left to right: Nikos Kontoes, President & Managing Director, Patras Port Authority; Stavros Antipas, Holding & Development Director, Patras Port Authority; Maria Fotiadou, Head of Corporate Development Activities Division, Public Gas Corporation of Greece (DEPA) S.A. ; Joseph Florentin, Project Manager, Hellenic Gas Transmission System Operator S.A. (DESFA S.A.); Thanos Koliopulos, Global Special Projects Manager, Lloyd’s Register; Anna Apostolopoulou, EU Projects Management & Coordination Leader, Lloyd’s Register; Antonis Boutatis, Port Master Planner, Senior Partner, Rogan Associates S.A.; Dr Adamis Mitsotakis, Research Associate, Centre for Research and Technology Hellas (CERTH)

Snapshot from the audience, Patras

CELESTYAL CRUISES LAUNCHES ITS NEW WEBSITE

Celestyal Cruises, announces the launch of its new website. Created to provide the best-possible user experience, the redesigned site, now compatible with all browsers and mobile devices, offers visitors a faster, simpler booking process and a comprehensive introduction to the company’s cruises, services and unique selling points. CelestyalCruises.com now features enhanced rich content, providing complete information on all of the cruises organized by the company in the Greek destinations and in Cuba.

The website provides all the necessary information the traveler needs in order to discover, explore and book a cruise, as well as the possibility to purchase integrated services provided by Celestyal Cruises both on board and on shore, such as excursions or drinks package upgrades.The site also features the latest company news, special offers and stunning high-resolution images of Greece and Cuba, as well as bespoke videos and information on the Celestyal Inclusive, the company’s value for money experience.

“The content, design and structure of our new website are based on the thorough research we conducted of our customers’ behavior,” said Celestyal Cruises CEO Kyriakos Anastassiadis. “We studied how our customers interacted with the features and content on our previous website, and we examined current online travel industry trends. Our site is now perfectly aligned with our company vision. Its fresh, uncluttered design emphasizes the Celestyal experience we provide our passengers, both in the Aegean and in Cuba, and we are sure it will captivate and inspire both new cruisers and returning passengers.”

About Celestyal Cruises

Celestyal Cruises is the only home-porting cruise operator in Greece and the preeminent cruise line serving the Greek Islands and circumnavigating the island of Cuba, year-round. The company operates five mid-sized vessels; each one being cosy enough to provide genuine and highly-personalized services. The foundation of the company’s philosophy is the ‘destination.’ Every cruise focuses on true cultural immersion, offering authentic, lifetime experiences both on board and onshore wherever its vessels sail.

Corporate Responsibility

Celestyal Cruises is deeply committed to sustainability and ethical business practices. The company actively supports the local communities in the destinations it visits, particularly in the field of education. Since 2015, more than 1,200 students on the Greek islands of Milos, Patmos and Ios have enjoyed a ‘journey to knowledge’, by attending specialized educational programs, initiated by Celestyal Cruises. Additionally, Celestyal Cruises supports cultural NGOs; while promoting youth entrepreneurship, marine student development and child welfare.

ISO Certification

The entire spectrum of Celestyal Cruises’ ship management, including technical, hotel and crew management, and offices, are certified in accordance with ISO 9001/14001 standards. The certifying authority is DNV-GL, which is by widely recognized as the biggest and most respected rating agency in the marine industry.

Awards & recognition

In 2017, Celestyal Cruises received four Cruisers’ Choice Awards from Cruise Critic, the world’s largest online cruise community, being voted ‘Best’ in the mid-sized category, for ‘Embarkation’, ‘Entertainment’, ‘Shore Excursions’ and ‘Value’. At the Greek Tourism Awards 2017, the company won five awards, as an indication of its dynamic presence in the cruise sector, as well as its great value offered. More specifically, the company won the gold award in the following categories: ‘Tourism Season Expanding Initiatives-Greek Tourism Product Enrichment’, ‘Guest Service Excellence’, ‘Gastronomic Tourism’ and ‘Corporate Identity-Corporate Reputation Management- Branding’; while also receiving a silver award in the ‘Integrated Marketing Campaign’ category.

Connect with Celestyal Cruises:

Facebook, Instagram, Twitter, LinkedIn

|

China banking regulator voices support for financial leasing in shipping

With China’s shipbuilding industry undergoing a challenging period of transformation and consolidation, the active participation of domestic financial leasing companies has become all the more important in helping shipyards clinch newbuilding deals with credible counterparties and export domestically-built ships, according to Mao Wanyuan, director of non-banking department at China Banking Regulatory Commission (CBRC).

For the part of CBRC, the regulator will assist in guiding the leasing houses to strengthen their risk management, widen their vessel-types portfolio, raise their level of professionalism, broaden their capital supplement channels, and encourage eligible lessee companies to establish locally-based subsidiaries, Mao said at a recently-held industry forum.

“Up until end-March 2017, China boasts 23 institutions involved in ship financial leasing, with their combined portfolio consisting of 989 ships sitting on deals valued at around RMB113.9bn ($16.5bn). Among the total value, 68\% are direct financing lease deals, an increase of 58\% year-on-year,” she told delegates at the forum.

Financial lease or capital lease, which is on the rise, sees the risks and rewards related to the ownership of asset leased being transferred to the lessee and so assets appear on the balance sheet.

Mao pointed out that Chinese leasing houses also offer operating lease deals to help shipowners who prefer to optimise their fleet structure by reducing their asset-liability ratio, with the asset not showing on the balance sheet.

Qiao Kai, vice-chairman of China Minsheng Financial Leasing, shared that out of the group’s hundreds of billions worth of assets (not just in shipping), the share of financial leasing accounts for up to 75\%, leaving the share of operating leasing much lower.

ICBC Financial Leasing is currently the leading Chinese lessor sitting on deals valued at RMB42bn involving 247 ships. The vessel types include containers, bulkers, and tankers, as well as cruise ships and LNG carriers, with clients across 11 countries and regions.

Seatrade Maritime News reported earlier this month that western shipowners are seeing more flexible and competitive terms being offered by Chinese financial leasing institutions compared to traditional bank lendings.

According to estimates, traditional banks have gone from financing around 80\% of the shipping industry in 2008 to about 60\% in 2016, while Chinese leasing firms have grown their market share to about 20\% last year, with part of that share coming from an expanding base of western shipowners.

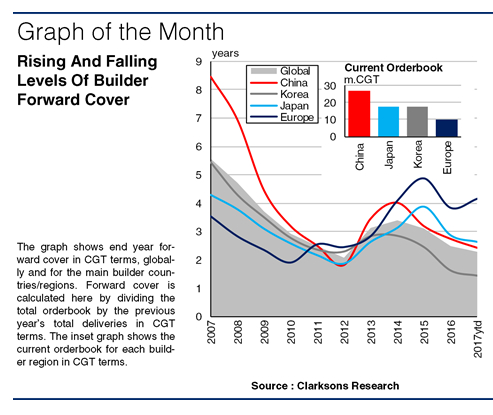

Shipbuilders Feeling Forward Cover Fluctuations

On a regional basis there are some interesting trends, with forward cover highest at European yards and at record lows at South Korean yards. This month’s Shipbuilding Focus investigates what factors have been behind these changes and how the situation may develop.

***image2.left***Regional Peaks And Troughs

Forward cover is one measure of shipbuilders’ future work, calculated here in CGT terms by dividing the current orderbook by the previous year’s output level. While as an indicator it fails to capture changes in shipyard capacity by relying on the previous year’s delivery data and doesn’t account for the impact of slippage and cancellation, it is still a useful measure of the shipbuilding industry’s health. Global forward cover is now at 2.3 years, low but not quite at the 2012 trough of 2.1 years. Korean yards’ forward cover has reached a historical low of 1.5 years, falling by 49\% from its last peak in 2014. Meanwhile, Chinese yards’ forward cover has declined by 40\% since 2014 and currently stands at 2.4 years. Japanese yards’ forward cover has fluctuated less, declining by 32\% since its last peak in 2015 and is currently at 2.6 years. Conversely, European yards’ cover is the highest at a healthy 4.2 years and has increased by 8\% in the year to date.

The Whys And Wherefores

Many factors influence forward cover, with recent declines at the ‘big 3’ builder countries largely caused by weak contracting which has depleted yards’ orderbooks. In China and Korea, strong deliveries have further reduced forward cover and the Chinese and Korean orderbooks have decreased by 36\% and 44\% respectively since start 2016 in CGT terms. The strong level of forward cover in CGT terms at European yards reflects their dominance in the cruise ship sector, with European yards’ orderbook stretching out to 2025. Meanwhile, Japanese shipyards’ relatively more stable contracting and delivery volumes have helped maintain a steady level of forward cover.

Looking To The Future

Needless to say falling levels of forward cover does not bode well for shipbuilders. As of 1st May 2017, there are 369 active shipyards globally (with a 1,000+ GT vessel on order). Of these yards, only 44\% are reported to have taken a newbuild order in 2016 or 2017 and 39\% are scheduled to deliver all vessels on their orderbook by the end of 2017. Furthermore, only 26\% have delivery slots booked further than 2018. If, for example, in 2017 there is the same level of contracting as in 2016, and assuming yards deliver around 33m CGT in full year 2017, we could see global forward cover drop below 2 years by the start of 2018. Even if ordering doubled year-on-year in 2017, global forward cover would simply remain steady at 2.3 years.

So, forward cover is falling for most builder countries as the global orderbook declines. This largely reflects historically weak newbuild contracting as well as relatively steady delivery levels. With forward cover likely to decline further or at best remain steady, the significant pressure on shipyards’ to build up their orderbooks is clear.

Source: Clarksons

LPG freight rate recovery to be confined to smaller vessels

However, the small vessel segment is the only category where fleet growth will be minimal, leading to a recovery in rates, according to the latest edition of the LPG Forecaster, published by global shipping consultancy Drewry.

Most vessel size segments are expected to witness another year of rapid supply growth in 2017, with the overall fleet forecast to expand by 16\%. This will keep freight rates under pressure over the next two years.

|

However, the small LPG vessel segment (1,000-5,000 cbm) will be the exception where fleet growth will be minimal and rates are expected to improve. After growing at an annual rate of 4\% over the last three years, pressurised vessel (p/r) fleet growth will slow to 3\% in 2017. Thereafter, p/r fleet growth is likely to turn negative as only one vessel will be left from the current orderbook to be delivered in 2018 and none beyond it, while some vessels will indeed get demolished.

Although the improvement in rates will mainly be led from the supply side, some push will also come from the demand side as refining capacity expands in China, increasing cargo supply for the intra-regional trade.

“As a result of slowing fleet growth, Drewry expects rates for small LPG vessels to strengthen further. We anticipate time charter rates for a 3,500 cbm p/r vessel to average $182,000 per month in 2017, an increase of 8\% from 2016. As fleet growth slows further from next year, rates will continue to improve and average $210,000 per month by 2019,” commented Shresth Sharma, senior analyst for gas shipping at Drewry.

Source: Drewry

Vale’s VLOC headache is contagious

But, should Vale lose faith in the VLOC fleet, the repercussions will boom throughout the market.

So, what’s a VLOC when it’s at home? The Stellar Daisy, Stellar Unicorn and Stellar Queen are three of 50 vessels that started life as single-hulled tankers carrying crude oil. Several high profile spillages led to single-hulled tankers being phased out in 2005-10 in favour of more secure double-hulled tankers. But many of the single-hulled tankers were relatively young and shipowners were reluctant to scrap them and lose a revenue stream. Some were converted to double-hulled tankers, some to floating storage units, and 50 were converted to bulk carriers — VLOCs.

Parts of the tanker were sealed off and turned into void spaces while the deck plating was changed and reinforced along the length of the hull with a myriad of other changes. These converted carriers are now coming up on their 25th year — the oldest that most dedicated dry bulk carriers would reach before being scrapped. The sinking of the Stellar Daisy and the problems discovered in the other vessels has also put owners and the Korean Register of Shipping, which carried out surveys on many of the ships, under scrutiny.

Polaris — owner of the Stellar Daisy and other very large crude carrier (VLCC) converts — has started checks and surveys on the vessels and found that the Stellar Hermes required reinforcement work. Caution may have led to similar work on the Stellar Cosmo although this has not been confirmed.

Vale has 50 VLOCs on charter. Most were converted in the late 2000s and chartered from the owners on 10-year contracts to carry iron ore between Brazil and China. Others were hired by steel producers such as Baosteel. Some of Vale’s agreements were extended at lower rates when the freight market crashed in 2011-12, but the majority will start to expire from 2018. And this is when Vale has scheduled delivery of the first of 29 new Valemax ships — its second tranche after the 37 ships built in 2011-13.

Valemaxes usually have a deadweight tonnage of between 388,000dwt and 404,000dwt, whereas the converted VLCC vessels are between 260,000dwt and 310,000dwt, so each Valemax could carry around 75,000-100,000t more iron ore than a converted VLCC ship.

But the sinking of the Stellar Daisy with the presumed loss of 22 lives, along with the hull cracks found in the Stellar Unicorn and Stellar Queen are a concern for the iron ore producer. With the backwash from the Samarco dam collapse still making life uncomfortable, it is a concern the company could do without.

So, Vale faces a significant choice. If it abandons the VLOCs, it will have 60mn t of iron ore — assuming four journeys a year carrying 300,000t ore for each ship — that it will have to charter spot market ships for until its Valemaxes start to be delivered in 2018-19. In addition, standard Capesize ships can probably only carry 150,000-180,000 t of material, so it will likely need two Capesize ships for every VLOC it stops using. If Vale stops using one VLOC, it will need to charter eight Capesize ships on the spot market over the course of the year, assuming four journeys per VLOC.

Vale was more active than usual in the first quarter of 2017. It only chartered about 30 ships between Brazil and China but this was sufficient to push rates from $10/t to $17/t — the highest since August 2015. An additional 10-20 fixtures would drive rates significantly higher, especially if they came in the third or fourth quarters when the cost of freight usually peaks. Each dollar per tonne increase will cost Vale an additional $150,000 per voyage. But if rates averaged $5/t higher, which would not be unreasonable, and the company required 12 additional voyages — covering three VLOCs — it would cost an extra $7.5mn above current freight costs. Rates on the route have reached $25-30/t in previous years when spot volumes from Brazil were more significant.

An increase in fixing activity on the Tubarao to Qingdao route usually has a far larger impact than an increase on the west Australia to Qingdao route — China’s principal iron ore artery. This is because vessels chartered from Brazil are usually out of the market for far longer. The journey between Tubarao and Qingdao take 54 days at 9 knots but a vessel can be out of the market for closer to 90 days including the turn time, loading and discharge times and the time taken to reach the port.

A journey between west Australia and China, on the other hand, takes just 12 days port to port and keeps ships out of the spot market for around three weeks. This would mean that any one fixture between Brazil and China would put substantially more upwards pressure on the spot market and a rush in such fixtures could push the cost of freight higher by several dollars rather than the $1-2/t that the west Australian route might gain.

Ouch!

source:http://blog.argusmedia.com

Asia-Europe marine container shipments notch new record: First-quarter reading sails past high marked a year earlier

Some 3.81 million twenty-foot-equivalent units, or TEUs, traveled that route in figures released Wednesday by the Tokyo-based Japan Maritime Center. This marked a 5.2\% surge from the record logged a year earlier.

Volume rose 8.4\% to 1.35 million TEUs for March alone, rebounding from February’s dip. In typical years, shipments during and after March soften before the summer-demand period. But demand for furniture, clothing and other goods has proved brisk this year, especially for shipments to the U.K. Cargo bound for oil producer Russia has also increased amid the petroleum price recovery that began last fall.

Expanded demand is forcing shipping companies to utilize more than 90\% of their carrying capacity. There are cases where shippers cannot secure space, a mixed-cargo operator reports.

Shipping fees are also trending upward. Spot rates for Asia-Europe freight now come to around $960 per TEU, up 18\% from the most recent low plumbed in late March. Shipments will hold steady for the time being, according to a major marine transporter, meaning that rates will likely be on the high side for the immediate future.

Source: Nikkei

Q88VMS Makes a Splash in Greece with Maran Tankers Management Signing

The cloud-based platform will allow Maran Tankers Management seamlessly to operate its growing fleet across their various offices without disruption or delay. “Q88VMS’ integrated approach to managing the voyage chain was a huge factor for our company, which encourages team work, open dialogue and sharing of information,” said Georgios Asteros, Operations Director of Maran Tankers Management.

“Having chartering, operations and post fixture in various offices across the globe, we needed a system that not only enables quick and accurate voyage calculations, fixtures, operations and reporting but also works across devices and locations. Q88 has delivered on their promise, getting us up and running in days.” Q88VMS, the latest product in Q88 LLC’s portfolio, is a web-based platform for managing all voyage related information.

Built by people with chartering and operations experience, Q88VMS is designed to empower its users, catering to real-world industry dynamics. Q88VMS’ user base has more than doubled over the past 9 months, with the majority of growth concentrated in Europe. Fritz Heidnereich, President of Q88 LLC, said, “We are very excited about Maran Tankers Management joining the Q88VMS community. Greece is a crucial market to us, and having a company like Maran Tankers, with such great history and a reputation of excellence, onboard is huge. We look forward to continuing our relationship with Maran Tankers and further serving the Greek shipping community.”

Maran Tankers Management (“MTM”) is the Oil Tanker Shipping unit of the Angelicoussis Shipping Group Limited (“ASGL”). MTM was established in 1992 to manage the Oil Tankers of ASGL. ASGL has a well-established track record in shipping, dating back to 1947. ASGL’s fleet now comprises bulk carriers, tankers and LNG vessels. Today it employs a staff of approximately 300 shoreside professionals as well as over 3,700 officers and crew. Today, MTM manages a fleet of over 40 vessels including VLCC’s, SUEZMAX’s and AFRAMAX’s, with more vessels scheduled to be delivered in the coming months.

Source: Q88 LLC

EURONAV announces execution of five year contracts for its FSO joint venture

The contract was signed with North Oil Company (“NOC”), the future operator of the Al-Shaheen oil field, whose shareholders are Qatar Petroleum Oil & Gas Limited and Total E&P Golfe Limited.

The new contracts for these custom-made 3 million barrels capacity units which have been significantly converted and that have been serving the Al-Shaheen field without interruption since 2010 will have a duration of five years starting at the expiry of the existing contracts with Maersk Oil Qatar. The existing contracts will remain in force until expiry in the third quarter of 2017.

The new contracts are expected over their full duration to generate EBITDA (earnings before interest, taxes, depreciation and amortization) in excess of USD 360 million for the joint

ventures. Based on Euronav’s 50\% ownership in the joint ventures the five year contracts are expected to generate in excess of USD 180 million of EBITDA for the Company.

The FSO Africa and FSO Asia floating storage platforms are both high specification and long duration assets with a potential trading life to 2032. In addition the joint venture

with International Seaways will be debt free from July 2017 providing further optionality to create value.

Paddy Rodgers, CEO of Euronav said: “We are pleased as these contracts provide Euronav with an additional degree of high quality earnings visibility. Combined with our underlying time charter portfolio, this provides Euronav with a solid base of fixed income”.

Euronav takes this opportunity to highlight to investors a short film on the original conversion of the FSO Asia to indicate the scale, investment and technical complexity of the operation.

IMO in the polar environment: the Polar Code explained

![]()

Powered by ![]() © Μaritimes 2019

© Μaritimes 2019