South Korean shipbuilders eyed for LNG carriers deal worth $3.8 billion

CBI Energy and Chemical, which is controlled by Australian and Canadian investors and has offices in Hong Kong, also disclosed in a statement to Reuters that it would be seeking to buy floating LNG production and import facilities as part of an ambitious plan for Africa and Asia.

The orders would be a major shot in the arm for South Korea's ailing shipbuilding industry, which has been hit by a collapse in new orders as global trade growth slows and after the slump in commodities prices in recent years.

CBI Energy would be taking advantage of low shipbuilding costs and cheap credit, that make it easier for newcomers to tap into a global switch towards cleaner sources of energy, LNG traders said. Depressed LNG prices are encouraging demand for the fuel, they added.

The company said in a statement to Reuters that "there is a need to custom-build specialty LNG carriers that will meet CBI's business needs."

It said that CBI has plans for Africa and Asia that include natural gas extraction, pipelines, marine transportation logistics, LNG plants, rail transport, power generation, chemical plants, and an LNG distribution network, including retail gas stations.

CBI has entrusted Korea Offshore and Ship's Technology Co Ltd (KOST) to find South Korean shipbuilders for the projects, officials from the two companies said.

"South Korea's LNG carriers are the best in terms of design, shipbuilding and delivery speed," an executive at CBI, who declined to be identified, told Reuters. "The shipbuilding industry is in a slump. This would be a stimulus."

MASSIVE OVERCAPACITY

KOST could approach STX Offshore & Shipbuilding, Daewoo Shipbuilding & Marine Engineering Co, Samsung Heavy Industries and Hyundai Heavy Industries Co Ltd to build the vessels, the person added.

It is not yet clear whether the contract would be concentrated with one or two shipbuilders or be spread more widely, said the official from KOST, who also declined to be identified. Initially there would be 10 firm orders, with an option to buy 10 more carriers, this person said.

South Korean shipbuilders have also been hit by increased competition from Chinese and Japanese yards, and massive overcapacity in the shipping industry.

The collapse of Hanjin Shipping, the world's seventh largest container shipper at the end of August, dealt a further blow to sentiment. Korea Development Bank forecast in a report the same month that the country's shipbuilders would suffer a 92.3 percent plunge in orders this year.

"Global shipyards including those in the main shipbuilding countries of South Korea, China and Japan, have seen the volume of orders in tonnage terms slump this year to the lowest level in more than 20 years," said Peter Sand, chief shipping analyst at ship owners lobby group BIMCO.

LNG carriers are a bright spot, though, because of demand for cleaner energy, said the KOST official.

The person said talks with shipbuilders would start after detailed plans were made, adding that it would take two to three months to select contract winners based on price, quality and the ability to meet delivery deadlines.

The vessels would each have the capacity to transport 120,000 to 175,000 cubic meters of LNG, the two sources said.

The first ship was due to be delivered in 2019, they said, adding the remaining vessels would be delivered at a rate of one ship every two-to-three months.

SHIPPING LNG TO CHINA

CBI Energy is a holding company registered in the British Virgin Islands and lists offices in Hong Kong, Beijing and Switzerland.

Its core investments are in coal poly generation, a "clean coal" technology, as well as LNG and associated supply chain businesses, according to the company statement.

The CBI executive said the group was 70 percent Australian owned and 30 percent Canadian owned. He declined to provide further details.

It has raised 2 billion euros from European private equity investors to fund the orders, the executive added.

The KOST official said CBI planned to ship LNG from Africa and the Middle East to China.

KOST, which is based on South Korea's southeastern island of Geoje, the country's shipbuilding hub, supervises shipbuilding projects.

The order would increase the global fleet of LNG tankers by more than 3 percent, making CBI a significant new player in the LNG logistics business if it opted to operate all the vessels itself. There are currently 460 tankers in service, with a further 170 on order.

A 174,000 cubic meter LNG carrier costs around $198 million to buy, down from $205 million two years ago, shipping services firm Clarkson said.

South Korean shipbuilders, Samsung Heavy and Daewoo Shipbuilding and Marine Engineering, are the most popular shipbuilders for LNG tankers, having built 22 percent and 21 percent respectively of the LNG carriers operating worldwide, according to data from shipbroker Banchero Costa (Bancosta). Of the LNG carriers under construction and on order, 37 percent of the current order book is placed at Daewoo shipyards, 14 percent at Hyundai Heavy and a further 11 percent at Samsung, Bancosta said.

Between 2016 and 2020, global LNG production capacity is expected to rise by about 50 percent to around 370 million tonnes a year, with major new projects in Australia, the United States and elsewhere, and this expected run-up in supply has dragged on prices.

"Although as many as 2,200 new cargoes of LNG are set to come on-stream by 2019 or 2020, the growth in the sector continues to be quite uncertain," according to a Bancosta report last month.

"European Union demand is fairly stable, global gas demand has slowed in the face of competition from other energy sources within the power sector, and from the persistence of low prices in energy commodities."

source:reuters.com

Fredriksen Said to Be Willing to Lend Seadrill $1.2 Billion

The loan of $800 million to $1.2 billion features in a proposal by a working group of fewer than 10 banks, said the people, who asked not to be identified because the talks were private. The plan would imply a postponement of all bank maturities to at least 2020, helping the lenders avoid outright losses, the people said.

Seadrill rose 22 percent to close at 21.75 kroner in Oslo trading, after erasing earlier losses.

The proposal will be assessed by the wider group of 42 Seadrill lenders and the company’s bondholders, the people said. Seadrill Chief Executive Officer Per Wullf said on Sept. 14 that he aims to have a solution for restructuring the company’s net debt of more than $9 billion by the beginning of December.

Seadrill declined to comment on the details of the proposal, according to a spokesman who asked not to be named in line with company policy. The refinancing plans remain on track, he said. A senior adviser to Fredriksen didn’t immediately reply to an e-mail and a phone call seeking comment.

Seadrill Pressure

Seadrill and other offshore-rig operators have been hit hard by the collapse in crude prices over the past two years as oil companies slashed spending on services such as drilling. The pain has been compounded by a wave of new rigs, creating massive oversupply in the industry and decimating rental rates. Drillers have cut costs, suspended dividends, renegotiated contracts and idled or scrapped rigs to weather the market rout.

The pressure is particularly high on Seadrill, whose net interest-bearing debt of $9.1 billion at the end of the second quarter is the highest among its peers.

The company “might have found a way to begin untangling the mess,” Janne Kvernland, an analyst at Nordea AB, said in an e-mailed note to clients Tuesday following the news that Fredriksen could provide capital through a loan. “It is hard to assess the valuation impact as the structure and terms of the capital injection is unknown, but we would see it as a positive if Seadrill is able to start to build a credible runway into 2020.”

Crown Jewel

All eyes have been on Fredriksen, who founded Seadrill in 2005 and built it up to become at one point the biggest offshore driller by market value. The company was the crown jewel of his shipping and oil empire until the market collapsed at the end of 2014. The stock has dropped more than 90 percent since July 2014. Fredriksen’s net worth is currently estimated at about $10.2 billion, with more than half in cash and other assets, according to the Bloomberg Billionaires Index.

Under the proposal being discussed for Seadrill’s restructuring, Fredriksen’s contribution would come as a loan and not new equity because he views debt as a less risky investment than stock given the industry’s outlook, the people said.

Seadrill will still need at least $1 billion in equity by the end of 2018, even if bond and bank maturities are extended, said Kvernland of Nordea, which has a sell recommendation on the company’s stock.

“Even if the initial outcome eventually proves to be additional debt, it is undoubtedly not a sustainable solution,” she said. “The huge dilution risk obviously remains.”

Seadrill’s $843 million bonds due September 2017 rose to 46.5 cents on the dollar on Tuesday, the highest in more than two months and 5 cents higher than the last transaction recorded on Friday, according to Trace, the bond price reporting system of the Financial Industry Regulatory Authority.

While rental rates for floating rigs may have bottomed out, it’s impossible to say when they will finally recover, Wullf said on Sept. 14. The CEO said at the time that he was “carefully optimistic” about Seadrill’s restructuring process. “It’s a big puzzle,” he said.

source:bloomberg.com

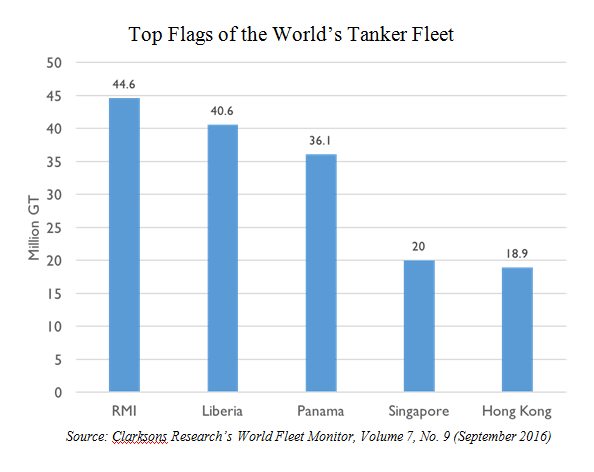

Republic of the Marshall Islands Becomes No. 1 Flag for World's Tanker Fleet

|

International Registries, Inc. and its affiliates (IRI), which provide administrative and technical support to the RMI Maritime and Corporate Registries, is committed to the continued decentralization of services to better support the Registry's owners and operators in every aspect of their business. This principle has led the RMI Registry to an average year-on-year growth of 15\% since 2001.

Overall, the RMI Registry now stands at 137.3 million GT, with an average age of 8.7 years. The 3,937 vessels flying the RMI flag are afforded the excellent safety record of the flag that has been on the US Coast Guard's Qualship 21 program for 12 consecutive years and continues its status on the White Lists of the Paris and Tokyo Memorandums of Understanding.

"Qualship 21 is a particularly difficult standard to meet," said Bill Gallagher, President, IRI. "As mentioned at the Connecticut Maritime Association's (CMA's) Shipping 2016 Conference, 13 of the 26 eligible flag States from 2015 fell off Qualship," he remarked. "This dramatic development in the spring led directly to the increased tonnage for the Registry in the summer," continued Mr. Gallagher. "The RMI is the only flag State of the three largest that holds Qualship 21 status; where others have faltered, we have remained steadfast for more than a decade," said Mr. Gallagher.

The RMI Registry's success is in large part due to IRI's customer focused approach and excellent quality record.

"Tanker tonnage undergoes a strenuous vetting process and choosing a quality flag is one of the most important factors in the process for owners, operators, and charterers," said Bill Gallagher. "Through our exceptional operations and customer service to so many of the world's top shipping companies, the RMI Registry is in the business of running a high-quality and sustainable flag," he continued. "We pride ourselves on our proactive approach to our shipowning customers, whether this means practical advice on ensuring that a ship meets port State control standards or addressing our owners and operators concerns in the development of international regulation, we provide a high l evel of support from any of our 27 worldwide offices," he continued.

The RMI continues to be proactive at the International Maritime Organization (IMO) and in September established a dedicated team of experts to guide shipowners through the complications of complying with the recently ratified Ballast Water Management Convention (the "Convention").

The move follows Finland's ratification of the Convention which means that more stringent ballast water management regulations will enter into force in September 2017.

To comply, existing vessels will need to have installed a Convention Type Approved Ballast Water Management System (BWMS) by the first renewal of the vessel's International Oil Pollution Prevention (IOPP) Certificate.

The RMI Registry allows an early renewal of the IOPP Certificate before the entry into force of the Convention, which allows five years from the renewal date for BWMS installation. The RMI will be supporting proposals at the IMO's Marine Environment Protection Committee (MEPC) October meeting for a delay of BWMS installation on some existing vessels.

"We are committed to working with the industry to find practicable solutions to the Convention requirements," said Bill Gallagher.

"After making the difficult decision of choosing a flag, shipowners should enjoy peace of mind knowing that they have the full support of the RMI Registry," he concluded.

|

BIMCO raises serious concern over data on available fuel ahead of MEPC decision on global sulphur cap implementation date

The official IMO study which assessed the relevant availability of fuel oil has failed to fully address the IMO’s terms of reference – in BIMCO’s view – in several critical areas:

On fuel oil quality. A significant amount of the fuel oil that the IMO study concludes will be available for marine use is unsafe to store and use onboard ships.

On how an assessed shortage of sulphur removal capacity in refineries will be resolved so that capacity would be in place by 2020.

The study fails to model the disruption that an overnight introduction of the global cap (from 31 December 2019) would cause.

As a result, BIMCO states it is not possible to determine that the global refining industry will have the capacity to produce enough marine fuel by 2020. BIMCO also raises concerns that the supply of fuel to other sectors of the global economy could face major disruption if the scenario is not addressed beforehand.

BIMCO, among others, have funded an independent supplementary study (carried out by EnSys and Navigistics) to assess the availability of marine fuel, which addresses all the above issues. This study concluded that it is unlikely that there will be sufficient low sulphur fuel available in 2020, while maintaining uninterrupted supply of fuel to all other sectors of the global economy.

Lars Robert Pedersen, Deputy Secretary General at BIMCO, said:

“It is clear that the IMO study is flawed, meaning it is not possible to determine from the study that there would be sufficient fuel available in 2020. On that basis, our opinion is that it would be irresponsible for IMO to make the decision to go for 2020 at MEPC 70 in October. There is clearly a need for additional analysis to ensure the supply chain for global trade is not seriously disrupted and developing nations are not hit hard by a lack of affordable energy”.

“This is not about the cost of low sulphur fuel for ships – that has long been known. We know that the shipping industry will buy the fuel they need. But if it is in short supply, the cost will rise not just for shipping but for all users of the fuel. This will price those in poorer economies out of the market”.

“It’s a complex issue – but the difficulties in ensuring sufficient refinery capacity and the disruption caused by an overnight introduction have to be thoroughly taken into account”.

BIMCO

Official operning of Neptune Lines new service in the Gulf

To mark the opening of Neptune Lines, an official reception was held in Dubai on the 27th of September, attended by UAE government officials as well as leaders of the shipping and logistics industry.

Neptune’s President and Chief Executive Officer, Mrs. Melina Travlos said: “I am delighted to be here, to celebrate together with our distinguished guests, our entry into a visionary region with world-class infrastructure that strives for continuous growth and development. We are creating a sea bridge dedicated to the automotive trade, servicing the Emirati ports as well as the ports of Oman, Qatar, Saudi Arabia, Kuwait, Iraq and Iran, aiming to boost and facilitate the trading of vehicles overall, offering permanent solutions for reliable, on-time deliveries. We are committed to contributing to this region our pioneering expertise and professionalism alongside our pledge for excellent quality shipping services”.

His Excellency Mr Jamal Majid Bin Thaniah, Vice Chairman DP World, added: “On behalf of DP World, I wish to extend a warm welcome to Mrs Travlos and Neptune Lines and wish them every success in their new endeavors”.

The new Neptune Lines service is supported by NMT Shipping, its commercial agents in the region, and is scheduled to connect the UAE ports of Jebel Ali and Khalifa to the ports of Shuwaikh (Kuwait) and Umm Qasr (Iraq), as well as Bandar Abbas (Iran), Sohar (Oman), Dammam (Saudi Arabia), Hamad (Qatar) and Khalifa Bin Salman (Bahrain). Upon demand and subject to availability, the new service will also operate alternative routes on an inducement basis. The leading executive of Neptune Lines operations in the region, based in Dubai, is Mr. Markos Vassilikos. Mr Vassilikos, as the former head of Neptune Lines operations, has a vast experience in the field and a deep knowledge of the company and its business culture.

NEPTUNELINES.COM

New survey findings worsening global shortage of trade finance

Only 52\% of respondents reported an increase in trade finance activity, compared to 63\% in 2015 and 80\% in 2012. Furthermore, the perceived shortfall came predominantly from regional and global banks – 78\% and 56\% respectively, compared to 41\% of national banks.

ICC Secretary General John Danilovich said: ‘We must emphasise the importance of trade finance. It is often forgotten – trade finance has dropped off the international agenda. We need to do more to communicate its central importance to the global economy.’

The Global Survey also shows that SMEs face 58\% of total rejections – despite submitting 44\% of all trade finance proposals, in contrast to 40\% submitted by large corporates (33\% of rejections) and 16\% by multinational corporations (9\% of rejections).

In addition, 90\% of Global Survey respondents cited the cost and complexity of compliance requirements relating to Anti-Money Laundering (AML) and Know Your Customer (KYC) regulation as barriers to the provision of trade finance, up from 81\% in the 2015 Global Survey. Indeed, 40\% of respondents reported terminating banking relationships due to compliance requirements, with 83\% expecting compliance costs to increase in 2016. Other impediments to trade finance noted by respondents included low issuing bank credit ratings (86\%), low country credit ratings (82\%), regulatory requirements (76\%), and low obligator or company ratings (70\%).

A decrease in the use of traditional trade finance was also evident in this year’s Global Survey report, with nearly 50\% of respondents reporting a decrease in commercial Letters of Credit, while nearly 35\% reported an increase in supply chain finance deals.

‘Year on year, the Global Survey continues to provide a snapshot into market trends, ensuring that the trade finance industry keeps pace with an ever-changing banking environment and remains fit for purpose,’ said Daniel Schmand, Chair of the ICC Banking Commission that conducted the Survey. ‘This year’s Survey highlights the challenges ahead, revealing that compliance is one of the main impediments to trade finance provision – with the majority of industry players only expecting complexity and cost to increase further over the rest of the year. Urgent action is required to limit the effects of such requirements on trade finance provision, and to help meet the needs of global SMEs, which are being disproportionately affected.’

This year’s Global Survey also highlights the benefits that digitization brings to the industry – particularly by automating processes and reducing the cost and complexity of trade finance. Despite this, only 7.4\% of banks reported that their trade finance processes had been digitized ‘to a great extent’, while 43\% reported ‘very little’ advancement, with global banks the most likely to embrace digital solutions. However, the Global Survey predicts an acceleration towards digitization in the years to come for the trade finance industry.

The increasing engagement of African economies and businesses in international trade is also a key focus of this year’s Global Survey. While intra-African trade has shown signs of significant growth – accounting for nearly 18\% of the region’s total trade in 2014, an upward trend from 10\% in 2010 – intra-African investment accounts for only 12\% of the total value of investment in Africa, in comparison to 33\% in Asia. In addition, 66\% of businesses find access to finance a significant obstacle to trade in Africa.

‘Africa has a trade finance shortage estimated at between US$110 to US$120 billion – a range far higher than the previous estimate of US$25 billion,’ said Vincent O’Brien, a member of the ICC Banking Commission Executive Committee. ‘In particular, the unprecedented fall in commodity values has created liquidity gaps for many banks across the region. Initiatives that facilitate internal and external trade should be fully encouraged, while Africa also needs to attract much-needed financing to support trade and meet the significant trade finance deficits.’

ICC’s Global Survey – released every year since 2009 – is enriched by data, insights and expert commentary from a variety of partners, contributors and specialists in trade, financing and development. It provides a unique perspective on the foregoing issues in business and trade, and can inform the decision of bankers, financiers, business executives and entrepreneurs, as well as policymakers at national, regional and international levels – with the objective of helping to restore trade as a driver of economic growth, value-creation and development.

Data from this year’s Global Survey was put under the spotlight at a SIBOS Banking Commission meeting, which focused on the debate around trade and trade finance. In addition, the report findings aim to inform the high-level discussions at WTO, IMF and World Bank annual meetings occurring this week in Washington.

Source: ICC – International Chamber of Commerce

Noble Group sells US energy business in turnround drive

Noble Group has sold its American energy business to Calpine Corporation of the US for more than $800m plus working capital, as the Asian commodities trader seeks to shore up its balance sheet.

The Singapore-listed company, which has endured a torrid 20 months since questions were raised about its accounting, said the divestment of San Diego-based Noble Americas Energy Solutions was a big step toward reaching its goal for raising capital this year.

“The sale of Naes substantially completes the $2bn capital raising initiative that we announced in June,” said Noble’s co-chief executives Jeff Frase and Will Randall, who took the reins following the departure of Yusuf Alireza in June.

The sale of Naes, a wholesale retailer of gas and power to large customers, is for a base price of $800m plus working capital — an amount that Noble said was almost $250m, while Calpine put it at $100m.

Calpine’s figure for working capital is more reliable, and the overall sale price is “disappointing for Noble”, according to Iceberg Research, which originally raised the accounting concerns.

Hong Kong-based Noble has defended its accounting and denied any wrongdoing. It has sold off chunks of its business, including its agricultural arm, to help pay down debt and issued shares to raise capital.

While the sale of one of its best-performing assets will lessen concerns over its balance sheet, analysts say the company still faces cash flow issues. Noble continued to burn through cash in the first half of the year and its adjusted net debt, which counts inventories of oil and coal as cash, ballooned to $2.4bn — about $500m more than its market capitalisation.

“[The sale] helps their balance sheet short term but it doesn’t help the unwinding or its cash flow problem,” according to an analyst at DBS bank in Singapore.

In the six months to June 30, Noble reported negative operating cash flow of $570m and a net loss of $14m.

Shares in Noble were up 6.8 per cent at S$0.205 on Monday afternoon in Singapore. They have fallen by a third this year, but since hitting a 13-year low of S$0.112 in September have rallied about 80 per cent.

Noble embarked on an aggressive expansion in 2009 after Chinese sovereign wealth fund CIC bought a 14 per cent stake.

The sale of Naes, which it acquired in 2010, marks the disposal of a business that had consistently generated cash but fell largely outside the vision of the company’s new co-chief executive. Noble’s former chief executive had said before his departure that Naes was not for sale.

In March, Noble completed the $750m saleof its stake in an agricultural joint venture to China’s state-backed grains trader Cofco. It has also scaled back or exited trading in gas, power and metals in Europe.

When it launched an emergency $500m rights issue in June Noble’s chairman, Richard Elman, subscribed to 56 per cent more shares than he originally pledged, maintaining a near 20 per cent stake in the company he founded.

Calpine Corporation is the largest generator of electricity from natural gas and geothermal in the US. The deal is subject to approval by Noble shareholders and the US energy regulator, but is expected to be completed by December this year.

Copyright The Financial Times Limited 2016.

Can Shipping Keep Its Big Break Going?

However, there’s still some way to go to better times, so it’s worth taking a look at how today’s ‘big break’ might leave the future potential scrapping profile.

The Big Break!

The Big Break!

Since the start of 2009, a total of 206.6m GT of shipping capacity has been sold for recycling, compared to an aggregate of 63.1m GT in the previous seven years. This total includes 94.7m GT of bulkcarrier tonnage and 29.1m GT of containerships, helping to address oversupply in the volume shipping markets. But given such a prolific run of demolition activity, what does the future potential scrapping profile look like? Well, there are many measures that can be used to investigate this, including the metric featured in the graph. If the average age of scrapping is taken as a useful indicator of the current state of conditions facing owners in each market, then calculating the amount of tonnage remaining in the fleet at today’s average age of scrapping or higher might tell us something interesting, especially if ongoing market conditions persist.

What’s Left On The Table?

In the tanker sector, which up until fairly recently was backed by stronger market conditions, the average age of scrapping in the year to date remains relatively high, at 25 years for crude tankers and 27 for product tankers (bear in mind that not many tankers have been sold for scrap recently, and the average age may fall). Given that a lot of older single hulled tanker tonnage was phased out in the 2000s, the amount of tonnage above the average age today is limited. In the bulker and containership sectors, both under severe market pressure for some time now, the statistics are a little more revealing. Despite heavy recycling in recent times, the share of tonnage above the current average age of scrapping is 8\% for Capesizes and 6\% for Panamaxes. For boxships sub-3,000 TEU the figure is 10\% and for those 3-6,000 TEU 12\%. Of course if the average age of scrapping falls, then the picture changes again. In the 3-6,000 TEU boxship sector, the youngest ship sold for scrap this year was just 10 years old; around 50\% of tonnage today is that age or older.

Cue More Demo?

What does this tell us overall? Well, using the sector breakdown shown in the graph, the statistics tell us that around 75m GT in the fleet is above the current average age of scrapping, 6\% of the world fleet. At 2016’s rate of demolition, that’s another 2.4 years’ worth. And given the age profile of the world fleet, after another 2 years an additional 21m GT will have crossed the current average age mark and after 5 years another 77m GT.

Break Not Over?

So, what chance does the industry have of keeping the demolition pressure on? Well, obviously freight and scrap market conditions and regulatory influences will have a big say. However, it looks like, in today’s terms at least, the industry might be in a good position to keep the break going. Have a nice day.

Source: Clarksons

Nippon Yusen to Book $1.9 Billion One-Time Loss on Shipping Woes

Nippon Yusen will record a 195 billion yen ($1.9 billion) charge to reflect a drop in the value of its assets and those it plans to own, according to a statement from the Tokyo-based company Friday. The company is also considering revising its dividend payout and will announce any changes on Oct. 31, along with its fiscal second-quarter earnings, it said in the statement released after trading hours.

In a sign of the woes gripping the global shipping industry, South Korea’s biggest container mover Hanjin Shipping Co. filed for bankruptcy protection late August, while its peers grapple with losses or shrinking profits amid a trade slowdown in the aftermath of the 2008 financial crisis. Nippon Yusen and Kawasaki Kisen Kaisha Ltd., Japan’s third-largest shipping line, are both predicting losses this fiscal year.

“A recovery in rates is taking longer than expected,” Kouichi Kitamura, a spokesman for Nippon Yusen, said by telephone. “So, we decided to book a loss.”

Japan Credit Rating Agency put Nippon Yusen’s credit rating on negative outlook due to the one-time loss, it said in a statement. The company said it hadn’t accounted for the impact on its earnings in its previous forecasts.

“The extraordinary loss is equivalent to nearly 30 percent of the equity capital,” it said. That is “indicating that significant capital impairment cannot be avoided.”

Nippon Yusen shares rose 4.6 percent to 206 yen in Tokyo on Friday. They have declined about 30 percent this year, versus a drop of 11 percent in the Nikkei 225 Stock Average.

source:bloomberg.com

VesselsValue: Supramax dry bulk carriers’ values increase in September, while Capes and modern Handies soften up

CAPESIZE

Values have softened throughout September. 8 sales have been concluded this month. The ER Bayern and the ER Bavaria (179,400 DWT, 2010, HHI) were sold for USD 20.75 mil each, VV value day before sale was USD 20.85 mil and USD 20.95 mil respectively. The sale of the Hanjin Matsuyama (179,200 DWT, 2011, Sungdong) bought for USD 22.75 mil has further softened values. VV value day before sale USD 23.22 mil.

PANAMAX

Values have firmed throughout the month. 16 sales have been concluded. The Elpis I (75,200 DWT, 2001, Samho Tongyoung) sold for USD 4.5 mil, VV value day before sale USD 3.37 mil. The Nord Navigator (82,700 DWT, 2008, Tadotsu Tsuneishi) sold for a firm USD 10.5 mil, VV value day before sale USD 10.02 mil.

SUPRAMAX

Values have firmed throughout the month. 11 sales have been concluded this month. The two resales of Darya Rani and Darya Maya (64,000 DWT, 2016, Huangpu) have been bought by Celsius Shipping for USD 17.5 mil each. VV value USD 17.12 mil on 06/09/16. The Jin Han (61,400 DWT, 2011, Oshima) and the Jin Ming (61,400 DWT, 2010, Oshima) sold for USD 28 mil En Bloc. VV valued Enbloc at USD 24.3 mil. Older tonnage saw the Fleet Phoenix (55,900 DWT, 2006, Mitsui Ichihara) sold for a firm USD 8.85 mil, VV value at USD 7.97 mil. The Virginia (50,200 DWT, 2001, Mitsui Ichihara) sold for a USD 4.2 mil, VV value USD 3.93 mil.

HANDY

Modern tonnage has softened throughout the month, older tonnage has firmed. 16 sales have been concluded. Modern tonnage has softened, demonstrated by the sale of the Hanjin Isabel (36,800 DWT, 2012, Hyundai Vinashin) for USD 8.2 mil, VV value day before sale at USD 8.91 mil. The Daisy K (28,000 DWT, 2012, Imabari) sold for USD 7.9 mil, VV value at USD 8.97 mil. Older tonnage has firmed, Antonia (22,072 DWT, 2002, Tianjin Xingang) sold for USD 3.7 mil. VV value on day before sale was USD 3.17 mil. Long Beach (23,600 DWT, 2000, Kanda) sold for USD 3.2 mil, VV value at USD 2.38 mil.

Source: VesselsValue

![]()

Powered by ![]() © Μaritimes 2019

© Μaritimes 2019