Stealthgas inc. reports third quarter 2017 financial and operating results

OPERATIONAL AND FINANCIAL HIGHLIGHTS

- Operational utilization of 95.4\% in Q3 17’ (88.1\% in Q3 16’).

- Commercial off hire days reduced in Q3 17’ by 63\% compared to Q3 16’.

- 89\% of fleet days secured on period charters for the remainder of 2017, with a total of around $176 million in contracted revenues.

- Sale of two more of our oldest vessels, the Gas Moxie (1992 built) and the Gas Nirvana (1996 built), both for further trading.

- Revenues of $38.5 million, an increase of 11.9\% compared to Q3 16’

- Adjusted EBITDA of $15.3 million in Q3 17’ compared to $11.2 million in Q3 16’.

- Moderate gearing as debt to assets stands at about 40\%.

- Cash in hand of about $41.3 million with operating cash flow of $34.7 million.

Nine Months 2017 Results:

- Revenues for the nine months ended September 30, 2017, amounted to $115.9 million, an increase of $9.2 million, or 8.6\%, compared to revenues of $106.7 million for the nine months ended September 30, 2016, primarily due to improved market conditions.

- Voyage expenses and vessels’ operating expenses for the nine months ended September 30, 2017 were $11.8 million and $44.4 million respectively, compared to $11.7 million and $44.3 million for the nine months ended September 30, 2016. The $0.1 million increase in voyage expenses was mainly due to the higher bunker prices prevailing in the first nine months of 2017 compared to the same period of 2016. The $0.1 million increase in vessels’ operating expenses was mainly due to higher utilization of several vessels that faced a lot of idle time during the same period of last year, thus leading to increased maintenance costs.

- Drydocking Costs for the nine months ended September 30, 2017 and 2016 were $2.5 million and $3.2 million, respectively, representing the costs of 5 and 9 vessels drydocked in the corresponding periods.

- Depreciation for the nine months ended September 30, 2017, was $29.3 million, a $0.1 million increase from $29.2 million for the same period of last year.

- Included in the first nine months of 2017 results were net losses from interest rate derivative instruments of $0.3 million. Interest paid on interest rate swap arrangements amounted to $0.3 million.

- The Company recorded an impairment loss of $6.5 million in the first nine months of 2017 for seven of its oldest vessels, four of which had been classified as held for sale, as of the end of the related period.

- As a result of the above, the Company reported a net loss for the nine months ended September 30, 2017 of $2.0 million, compared to a net loss of $3.4 million for the nine months ended September 30, 2016. The weighted average number of shares outstanding for the nine months ended September 30, 2017 was 39.8 million. Loss per share for the nine months ended September 30, 2017 amounted to $0.05 compared to loss per share of $0.09 for the same period of last year.

- Adjusted net income was $4.7 million, or $0.12 per share, for the nine months ended September 30, 2017 compared to adjusted net loss of $3.8 million, or $0.09 per share, for the same period of last year.

- EBITDA for the nine months ended September 30, 2017 amounted to $39.6 million. Reconciliations of Adjusted Net (Loss)/Income, EBITDA and Adjusted EBITDA to Net Loss are set forth below. An average of 53.1 vessels were owned by the Company during the nine months ended September 30, 2017, compared to 53.3 vessels for the same period of 2016.

- As of September 30, 2017, cash and cash equivalents amounted to $41.3 million and total debt amounted to $398.2 million. During the nine months ended September 30, 2017 debt repayments amounted to $32.4 million.

Fleet Update Since Previous Announcement

The Company announced the conclusion of the following chartering arrangements:

- A three year time charter for its 1997 built LPG carrier, the Gas Galaxy, with an international petrochemical company until January 2021.

A two year time charter extension for its 2008 built LPG carrier, the Gas Defiance, with national oil company until January 2020.

A fourteen months’ time charter extension for its 2007 built LPG carrier, the Gas Flawless, with an international LPG trader until March 2019.

- A one year time charter for its 2007 built LPG carrier, the Gas Haralambos, with an international LPG trader until September 2018.

A one year time charter extension for its 2011 built LPG carrier, the Gas Myth, with an Oil Major until December 2018.

- A one year time charter extension for its 2012 built LPG carrier, the Gas Husky, with a shipping company until January 2019.

A one year time charter extension for its 2008 built LPG carrier, the Gas Shuriken, with a national oil company until November 2018.

- A one year time charter extension for its 1995 built LPG carrier, the Gas Texiana, with an international trading house until December 2018.

?

- A one year time charter extension for its 2006 built LPG carrier, the Gas Ethereal, with an international trading house until December 2018.

- A one year time charter extension for its 2016 built LPG carrier, the Eco Dominator, with a national LPG importer until January 2019.

- A six months’ time charter for its 1998 built LPG carrier, the Gas Legacy, with an Oil Major until April 2018.

A three months’ time charter for its 2006 built LPG carrier, the Gas Enchanted, with an international petrochemical trader until January 2018.

A three months’ time charter for its 2006 built LPG carrier, the Gas Sikousis, with an international trading house until March 2018.

- A three months’ time charter for its 2017 built LPG carrier, the Eco Frost, with an international LPG trader until January 2018.

- A two months’ time charter for its 2014 built LPG carrier, the Eco Corsair, with an international LPG trader until February 2018.

- A one months’ time charter for its 2015 built LPG carrier, the Eco Lucidity, with an international petrochemical trader until November 2017.

With these charters, the Company has contracted revenues of approximately $176 million. Total anticipated voyage days of our fleet are 89\% covered?for the remainder of 2017 and 63\% covered for 2018.

Board Chairman Michael Jolliffe Commented

In the third quarter of 2017, our market continued the positive momentum noticeable since the beginning of the year. As a result, we witnessed a further strengthening of the freight rates, a strong demand in spite of the weak seasonal period and managed to decrease our idle days by 63\% compared to the same period of last year.

Our revenues were 12\% higher than the third quarter of 2016, but our profitability, excluding non-cash items was somewhat impacted by a slight increase of our operating cost base. This increase was mostly attributed to a rise in maintenance costs due to the higher utilization of many older vessels that previously faced a lot of idle days.

We proceeded with the sale of two more of our older vessels at a 78\% and 220\% premiums over scrap value respectively. These sales took place in order to further boost our liquidity and ease our operating cost base. We still maintain strong earnings visibility and have a strong fleet coverage of 63\% for 2018.

As our market fundamentals are improving and look promising for the future, we hope to further improve upon our performance – increase our revenues, strengthen our profitability and continue to contain our costs.

About STEALTHGAS INC.

StealthGas Inc. is a ship-owning company primarily serving the liquefied petroleum gas (LPG) sector of the international shipping industry. StealthGas Inc. currently has a fleet of 52 vessels. The fleet comprises of 48 LPG carriers, including two chartered in LPG vessels, with a total capacity of 258,071 cubic meters (cbm) and three M.R. product tankers and one Aframax oil tanker with a total capacity of 255,804 deadweight tons (dwt). The Company has agreed to acquire a further 3 LPG carriers with expected deliveries in 2018. Giving effect to the delivery of these acquisitions, StealthGas Inc.’s fleet will be composed of 51 operating LPG carriers with a total capacity of 324,071 cubic meters (cbm). StealthGas Inc.’s shares are listed on the NASDAQ Global Select Market and trade under the symbol “GASS”.

European Shipowners welcome the agreement reached on CO2 Emissions Trading System

“European shipowners have a strong interest to decarbonise the industry and we think it is the right decision that the EU will leave regulation of shipping’s CO2 emissions to the International Maritime Organization”, commented Martin Dorsman, ECSA’s Secretary General. “The IMO is currently busy drawing up its strategy for reducing CO2 emissions from the international shipping. IMO is the organisation to regulate our global industry”, he concluded.

The IMO has certain agreed milestones in its plan of global climate strategy. In April 2018 the IMO should adopt an initial strategy for comprehensive emissions reductions from ships and in 2023 it should adopt a final strategy.

In the last IMO intersessional meeting in October, the industry proposed that the sector’s total CO2 emissions should not increase above 2008 levels, thus establishing 2008 as the year of peak emissions from shipping, and that IMO should agree upon reduction percentages per ton-km as well as upon an reduction percentage by which the total emissions from the sector should be reduced by 2050.

http://www.ecsa.eu

Ship Finance International Says Could Face Further Tanker Losses in Fourth Quarter

Highlights

• Declaration of third quarter dividend of $0.35 per share, the Company’s 55th consecutive quarterly

dividend

• Net income of $29 million and $150 million of total charter revenues during the third quarter

• Continued diversification and renewal of the fleet with the delivery of two LR2 product tanker

vessels with long term charters to Phillips 66 and the sale of an older crude oil tanker vessel

• Strengthened balance sheet with early conversion of $121 million of convertible notes

Selected key financial data

|

Ole B. Hjertaker, CEO of Ship Finance Management AS, said in a comment: “Including today’s announced dividend, Ship Finance has made aggregate dividend payments in excess of $23 per share since 2004, and we have remained profitable every quarter from our inception. Our track record and significant industry relationships provide access to a consistent stream of investment opportunities, and we remain committed to continuing to build the Company and return value to our shareholders. The fleet renewal continues and we have strengthened our balance sheet through amendments to certain loan facilities, the issuance of new unsecured notes in the market and the early conversion of a large portion of our convertible notes. These proactive measures significantly enhance our financial profile, allowing us to intensify our focus on growth.” Dividends and Results for the Quarter Ended September 30, 2017 The Board of Directors has declared a quarterly cash dividend of $0.35 per share. The dividend will be paid on or around December 29 to shareholders on record as of December 11, and the ex-dividend date on the New York Stock Exchange will be December 12, 2017.

The Company reported total U.S. GAAP operating revenues on a consolidated basis of $93.7 million, or $1.00 per share, in the third quarter of 2017. This number excludes $7.9 million of charter revenues classified as ‘repayment of investment in finance leases’ and $48 million of charter revenues earned by 100\% owned assets classified as ‘investment in associates’. Inclusive of those revenues, the total charter revenues were $150 million, or $1.60 per share. Reported net operating income pursuant to U.S. GAAP for the quarter was $37.6 million, or $0.40 per share, and reported net income was $28.7 million, or $0.31 per share.

Business Update

As of September 30, 2017, the fixed rate charter backlog from the Company’s fleet of 70 vessels and rigs was approximately $3.3 billion, with an average remaining charter term of nearly 5 years, or more than 8 years if weighted by charter revenue. Some of the charters include purchase options which, if exercised, may reduce the fixed rate charter backlog and the average remaining charter term, but will increase capital available for new investments. Additionally, several charters include a profit sharing feature that may increase our operating results.

Tankers

The Company currently owns 15 crude oil, product and chemical tankers, 13 of which are employed on long term charters. The crude oil tanker market remained at soft levels during the third quarter and the vessels chartered to Frontline Shipping Limited (“Frontline”) did not earn average daily rates sufficient to generate a profit share above the contracted base charter rate of $20,000 per day. The market has improved since the end of the third quarter, but based on guidance provided by Frontline, the recovery may not be sufficient to expect to earn a profit share from these vessels in the fourth quarter. The average daily time charter equivalent rate of the Company’s two modern Suezmax tankers trading in a pool with two sister vessels owned by Frontline Ltd. was approximately $24,800 during the third quarter, down from $26,900 per day on average in the previous quarter. Three of the four vessels in the pool have been chartered out until late 2017 with a profit share above a floor rate, mitigating a soft spot market during the third quarter. During the third quarter, the Company sold the 1997-built Suezmax tanker Front Ardenne to an unrelated third party. The net sale proceeds were approximately $12 million, including compensation for the early termination of the charter, and Ship Finance recorded a minor book gain from the sale. Following this sale, Ship Finance has nine vessels on long term charter to Frontline, all of which are VLCCs. Ship Finance took delivery of two 114,000 dwt LR2 newbuilding product tankers in August 2017. Both vessels have commenced long term time charters to Phillips 66, and the total EBITDA1 contribution from these vessels is estimated to be approximately $11 million per year, with full cash flow effect expected from the fourth quarter.

Offshore

Ship Finance owns five offshore support vessels and four drilling rigs. With the exception of the jack-up rig Soehanah, which is currently employed under a short term charter, all of the Company’s offshore assets are employed on long term charters. The Company’s drilling rigs generated approximately $49 million in aggregate charter revenues in the third quarter of 2017. Three of the four rigs are chartered out on bareboat charters to fully guaranteed affiliates of Seadrill Limited (“Seadrill”), where Seadrill is responsible for operating and maintenance costs. As previously announced, Seadrill commenced Chapter 11 proceedings and filed prearranged cases in the Southern District of Texas, U.S in September 2017. According to Seadrill, this is part of a comprehensive restructuring plan entered into with various creditors including Ship Finance, certain third party and related party investors and substantially all their secured lenders on a recapitalization of the company. Seadrill believes the comprehensive restructuring plan will provide them with a five-year runway and a bridge to an industry recovery, facilitated by a $1.06 billion capital injection, extended and re-profiled secured bank debt and debt for equity exchanges, all of which contribute to substantially reducing Seadrill’s financial leverage. As part of Seadrill’s restructuring plan, Ship Finance has agreed to reduce the contractual charter hire for the three rigs by approximately 29\% for a period of five years, beginning January 2018, with the reduced amounts added back in the period thereafter. The term of the leases for West Hercules and West Taurus will also be extended by 13 months until December 2024. Seadrill will continue to pay full charter hire until the restructuring plan is approved, and net of interest and debt amortization, the contribution from the three rigs was approximately $15.2 million, or $0.16 per share in the third quarter. Concurrently, Ship Finance has agreed with the banks that finance the rigs to extend the loans for a period of four years, starting from the original maturity date of each of the three separate loan facilities, with reduced amortization during the extension period compared to the current level. This extension is subject to approval of the restructuring plan, and the cash flow from the three rigs during the extension period, net of interest and amortization, is estimated to be approximately $29 million per year. Seadrill has sub chartered the harsh environment jack-up rig West Linus to ConocoPhillips until the end of 2028. In June, Seadrill announced that the semi-submersible rig West Hercules, which has been idle, has been awarded a short term sub-charter in the North Sea, with expected start up in April 2018. The semisubmersible rig West Taurus is currently in layup in Spain. The 2007-built drilling rig Soehanah, is now employed under a one-year drilling contract with a national oil company in Asia until June 2018, with an option to extend the charter until June 2019. The rig is debt free, and the EBITDA contribution from the charter is approximately $0.9 million per quarter.

Liner

Ship Finance has a fleet of 22 container vessels and two car carriers. With the exception of one smaller 1,700 TEU container vessel, all container vessels are employed on long term charters. The container market has strengthened during 2017, and most of the operators announced positive results in the third quarter. With a more robust underlying market and increased margins for the operators, there is higher activity in the chartering market, both for modern eco-type vessels, and also for older vessels trading in the short term market. The Company recently agreed to new charters for the two car carriers, Glovis Conductor and Glovis Composer, until mid 2018. The base charter rate for this period is lower than the level in the previous charter period, and the EBITDA contribution from the two vessels is estimated to be approximately $1.1 million per quarter during this period.

Dry Bulk

The Company owns 22 dry bulk vessels, 15 of which are employed on long term charters and seven of which trade in the spot market. The Company has the potential to generate additional revenues through the profit share agreement for eight Capesize vessels on long term charter to Golden Ocean Group Limited. There was no profit share recorded in the third quarter, but market rates in the dry bulk sector have improved over the last few months, and the Capesize spot market is now above the profit share threshold according to broker reports. Our dry bulk vessels trading in the spot market are all Handysize vessels between 32,000 and 34,000 dwt. These vessels earned average time charter equivalent rates of approximately $6,700 per trading day in the third quarter. With the recent strengthening in the dry bulk market, we expect average daily rates from these vessels to increase in the fourth quarter. The Company intends to continue trading these vessels in the spot market until long term rates improve.

Financing and Capital Expenditure

As of September 30, 2017, Ship Finance had approximately $254 million of available liquidity2 , including approximately $248 million in cash. In addition, the Company had marketable securities of approximately $116 million, based on prevailing market prices at quarter end. These include 11 million shares in Frontline Ltd. and financial investments in senior secured bonds and other securities. In June, Ship Finance successfully placed a NOK 500 million senior unsecured bond in the Scandinavian credit market with an interest rate of NIBOR + 4.75\% per annum and maturity in June 2020. During the quarter, the Company entered into hedge instruments whereby the bond was swapped to approximately $64 million with an average fixed interest rate of 6.9\% per annum. The proceeds were used to part refinance the NOK 600 million bonds originally due in October. Subsequent to quarter end, the Company announced that it had entered into separate agreements with certain holders of its 3.25\% Senior Unsecured Convertible Notes due 2018 (the “Notes”) to convert a portion of the outstanding Notes as a proactive measure to further strengthen the Company’s balance sheet. Approximately $121 million in aggregate principal amount of the Notes were converted into common shares of the Company at prevailing market prices. The number of shares economically3 outstanding following these conversions is approximately 102.9 million.

Strategy and Outlook

The long term strategy of the Company is to continue building our distribution capacity on the back of an asset portfolio consisting of high quality vessels and strong counterparties. Since the start of 2017, Ship Finance has proactively taken a series of steps to significantly strengthen its balance sheet and position the Company to pursue growth opportunities. Through our long term business relations, we believe we have premium access to deal flow in our core business areas, and the Company has significant investment capacity available for new accretive deal opportunities. Investing in cyclical markets requires discipline, both in terms of market timing and in the manner in which transactions are structured. Our approach is dynamic and focused on minimizing downside risk while maximizing revenues to support our distribution capacity. The near term focus will mainly be on the tanker, bulker and container markets, and we have significant flexibility in the structuring of new deals.

Accounting Items

Under accounting principles generally accepted in the United States of America (“U.S. GAAP”), subsidiaries owning the drilling units West Hercules, West Taurus and West Linus have been accounted for as ‘investment in associates’ using the ‘equity method’. All these equity accounted subsidiaries are wholly owned by Ship Finance, but due to the conservative structure of the leases, Ship Finance has not been deemed to be the ‘primary beneficiary’ according to U.S. GAAP. As a result of the accounting treatment, operating revenues, operating expenses and net interest expenses in these subsidiaries are not shown in Ship Finance’s consolidated income statement. Instead, the net contribution from these subsidiaries is recognized as a combination of ‘Interest income from associates’ and ‘Results in associates’. In Ship Finance’s consolidated balance sheet, the net investments are shown as a combination of ‘Investment in associates’ and ‘Amount due from related parties – Long term’. The reason for this treatment is that a part of the investment in these subsidiaries is in the form of intercompany loans.

Source: Ship Finance International Limited

SNAME President visits Athens

The SNAME GREEK SECTION monthly event was honored by Mr. Martin Toyen, President of Global SNAME, who visited Athens on 10-12 October, 2017. The interesting speech of the President of SNAME GREEK SECTION, Dr. Ioannis Kokarakis (BUREAU VERITAS), was followed by a reception for the Young Naval Architects, NTUA and TEI students, as well as very important Technical Directors from major shipping companies. The Board of the Executive Committee discussed the forthcoming SOME International Symposium that the SNAME Greek Section organizes on 20 & 21 March 2018 in Athens at the Eugenides Foundation in Paleo Faliro (with the noble allocation of the Amphitheater by the Foundation). It was agreed to extent a Call of Content, for the submission of either research papers or 20-minute PPT presentations by the 17th of November 2017. SNAME SOME objectives are to present up-to-date Research and Academic papers and applied operational solutions from Technical and other segments of Shipping Companies and Class Societies. SNAME SOME another aim is to award Scholarships to students of Naval Architecture & Marine Engineering with funds collected from sponsors. At present, Theodoros Kardaras, a student at NTUA Naval Architecture, was awarded of SNAME's scholarship. Mr. Martin Toyen was given a tour in Athens by Mr. Petros Lalangas, Ms. Yanna Pavlopoulou and the Βoard of the Student SNAME GREEK SECTION. More at: http://sname-ntua.com/president_visit.html

|

| Some Photos of Mr. Marty Toyen, SNAME President recent visit in Athens and of the joint Board Meeting of SOME SNAME GREEK SECTION Organizers |

|

|

|

|

|

|

DNV GL: Standardisation can help enable the digital transformation of shipping

|

Whether for operational optimization, model calibration for digital twins, design optimization or other applications, the maritime industry is exploring the opportunities offered by digital technologies. The first demonstration and pilot projects are already well underway and the industry is asking what is needed to transform these into fully scalable products. The answer could be a greater emphasis on standardisation.

“Standards are used in many industries to advance efficiency, safety and environmental performance,” says Pierre Sames, Group Technology and Research Director, DNV GL. “With the rise of the Internet of Things in shipping, we believe that many stakeholders can benefit from developing a standardisation strategy to take advantage of a more digital maritime industry.”

DNV GL’s new position paper focuses on the collection of ship sensor data, as increased sensor availability lets us collect both existing and new types of data more efficiently, with the result that more data is available than ever before. But as more data is being collected, exchanged and prepared for use, the origin, quality level, context, and legal status can become less transparent – the result being that end users are less likely to trust and therefore use the data.

"At DNV GL we have been involved in many digitalisation pilot and demonstration projects,” says Steinar Låg, Senior Researcher in Maritime Transport at DNV GL. “By looking at the results of these projects we identified several technical barriers that are hampering the data flow and usage. Too much time is spent matching and structuring different systems, while data collection products from different vendors often have incompatible outputs – making it difficult to combine the data of multiple systems. This makes the processes less efficient and more difficult for shipowners to obtain a complete picture of a vessel or their fleet.”

The report discusses the need for standardisation in six key areas: Ship data models, sensor naming and referencing, maritime taxonomies and code books, sensor metadata, shipboard data recorder, as well as sensor quality and reliability. However, as future technologies develop, there may be a need for new standards to support other applications, such as model-based simulations and autonomous ships.

“At DNV GL we will continue to work with industry stakeholders on new standards at the same time as we develop new rules, class notations, recommended practices and type approval programmes,” says Pierre Sames. “Standards are a key factor in removing barriers and enabling the growth of digital applications in the maritime industry and we hope this study will inspire others to invest in the development and adoption of standardisation.”

The full report can be downloaded here.

About DNV GL

Driven by our purpose of safeguarding life, property and the environment, DNV GL enables organizations to advance the safety and sustainability of their business. We provide classification, technical assurance, software and independent expert advisory services to the maritime, oil & gas and energy industries. We also provide certification services to customers across a wide range of industries. Operating in more than 100 countries, our professionals are dedicated to helping our customers make the world safer, smarter and greener.

About DNV GL – Maritime

DNV GL is the world’s leading classification society and a recognized advisor for the maritime industry. We enhance safety, quality, energy efficiency and environmental performance of the global shipping industry – across all vessel types and offshore structures. We invest heavily in research and development to find solutions, together with the industry, that address strategic, operational or regulatory challenges. For more information visit www.dnvgl.com/maritime

Ship operating costs stabilise as market recovery lifts pressure

|

After two years of marked decline, average vessel operating costs stabilised in 2017 as pressure on owners was lifted by a nascent recovery across most cargo shipping markets. Trends in ship operating costs are heavily linked to developments in the wider shipping market, external cost pressures notwithstanding.

But the recovery has not been uniform across all sectors, and risks remain. Despite a brighter economic outlook, the industry is still weighed down by excess capacity, poor profitability and high levels of debt and many owners are struggling to survive. Poor financial returns have kept the pressure on costs and we expect this to remain the case for the foreseeable future.

Drewry estimates that the average daily operating cost across the 44 different ship types and sizes covered in the report rose 0.9\% in 2017, following a 7.5\% fall over the previous two years (see graph below). Costs rose for most cargo sectors, with the exception of container shipping which achieved a third consecutive year of cost reductions.

The depressed state of shipping markets has forced operators to focus on cost reduction as a means of survival. In the past few years big savings have been achieved in stores and spares, while many owners have been forced to slash repair and maintenance spending, keeping any work to an absolute minimum. Meanwhile, falling asset values and excess capital for hull insurance have depressed insurance premiums. Finally, owners’ largest cost head, manning, has changed little in recent years as wage increases have been kept to a minimum.

"However, there are limits to how long cost cutting can be sustained,” said Drewry’s director of research products Martin Dixon. “This is evident from the uptick in spending on stores & spares as well as repairs and maintenance in 2017. Meanwhile, the recovery in crude oil prices from the lows of 2015 has forced up the cost of lubricants.”

These factors have helped to stabilise overall ship operating costs, while the early signs of a recovery in many cargo markets have given owners some breathing space.

Looking ahead, pressure to restrain costs will continue as many sectors remain overtonnaged and any recovery will rely on fragile fundamentals. Hence, Drewry expect costs under the immediate control of owners, such as manning, spares, repairs & maintenance and management & administration, to be tightly managed.

“But some cost elements are harder to control as they are driven by influences outside an owner’s control,” added Dixon. “Large losses being booked by reinsurers for a series of natural disasters this year will have the effect of driving up hull & machinery as well as P&I premiums in future years.”

However, given the more benign outlook for the remaining cost heads, overall ship operating cost inflation is expected to remain moderate over the next few years.

www.drewry.co.uk

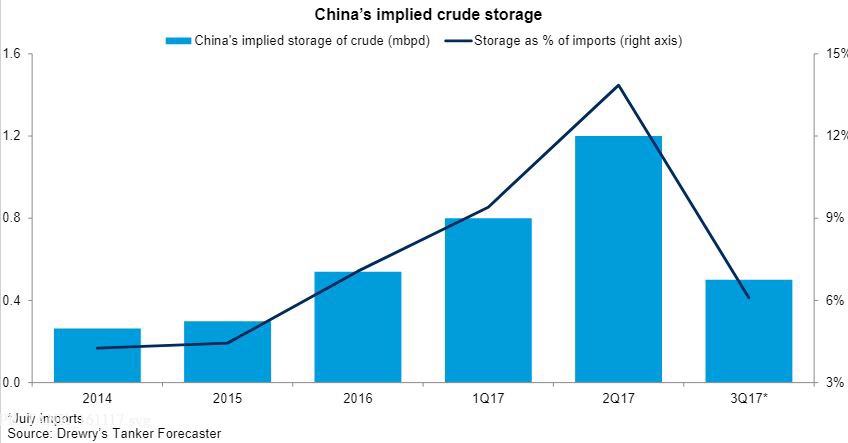

Slowdown in China’s crude stoking activity to hurt tonnage demand in the crude tanker shipping market in 2018

|

Although tonnage supply growth in the crude tanker market is expected to be low next year after surging in 2017, this will not be enough to push tonnage utilisation rates higher as demand growth is expected to be sluggish. A slowdown in global oil demand growth and a likely decline in China’s stocking activity will keep growth in the crude oil trade moderate next year.

After a sharp decline in 2016, freight rates in the crude tanker market have declined further this year despite strong tonnage demand growth in these two years, thanks to a surge in tonnage supply. Fleet growth is expected to come down to 3.2\% in 2018, after increasing by close to 6\% each year in 2016 and 2017. However, this is unlikely to provide any respite to owners as rates will continue to decline in 2018 on account of a slowdown in crude oil trade growth as global oil demand growth is expected to fall to 1.4 mbpd in 2018 from 1.6 mbpd in 2017.

In addition to this, a likely slowdown in China’s stocking activity poses a big risk to tonnage demand in the crude tanker market. China’s stocking activity, which remained one of the leading factors behind the strong growth in the crude oil trade over the last two years, may fall significantly in 2018. According to the IEA’s data on China’s implied stock changes, the country should have accumulated close to 520 million barrels since 2015, well above the total special petroleum reserve (SPR) capacity that was supposed to fully come online by 2020. A sharp decline in stocking activity in the third quarter of this year to 0.5 mbpd from 1.2 mbpd in the second quarter suggests that we might see a significant decrease in the inventory build-up by China in 2018.

“We expect China’s stocking activity to decline to 0.25 mbpd in 2018 from an average 0.75 mbpd in 2017, curbing global trade growth,” commented Rajesh Verma, Drewry’s lead analyst for tanker shipping. “The anticipated decline in China’s stocking activity added to a slowdown in worldwide oil demand will keep global crude oil trade growth modest in 2018, which in turn will keep rates under pressure despite some slowdown in fleet growth,” added Verma.

www.drewry.co.uk

Why the Cruise Industry Is Booming in the Middle East

Onto the cruise ship climbed several burly security guards with cases of "conventional weapons," which would provide, as the captain explained, an added layer of protection for a potentially tricky passage.

"This is just like a James Bond movie," said Dr. Jack King, an orthodontist from Dayton, Ohio—and one of 548 passengers sailing on a three-week voyage from Rome to Dubai.

A week later, near Abu Dhabi, an alarm sounded, signaling the arrival of another boat. This time, it was stocked with 500-gram tins of Sterling Caviar and Champagne for Encore guests to enjoy in the warm surf of a private beach.

Cruising from the Mediterranean to the Persian Gulf brings a sense of intrigue—and often, a fair share of five-star accoutrements. And more and more travelers are catching on.

A total of 87 cruise ships docked in Dubai in 2009, a number that nearly doubled to 157 during the 2016-2017 winter season. At last count, 18 companies were docking in the Middle East this winter, with five cruise lines doing a full season there; additional companies, including Carnival Corp.’s P&O Cruises, are planning new itineraries to come online in 2019.

Here’s why: With Middle Eastern countries investing heavily in infrastructure, cruise lines now see the region as an attractive place to move their Europe fleets in the winter season, while travelers see the itineraries as an easy way to check off several bucket list attractions they may not previously have visited.

No Worries Needed

The National Policy Framework on alternative fuels

Poseidon Med II work on promoting LNG and elemed work on promoting electricity have been highlighted, with specific emphasis to the development of LNG port infrastructure, the development of regulation for LNG bunkering, as well as the pilot shore-power installation in Killini port (within elemed project), the exploration of including electric energy in the list of marine fuels, with equivalent or even more favourable terms.

Overall, this is of great success for the projects work so far promoting alternative fuels in marine transportation, highlighting the valuable role of Poseidon Med II and elemed in advocating towards the implementation of an effective regulatory framework for alternative fuels.

Indicative references in the FEK:

Poseidon Med II (see p. 46517 – 46518, Chapters 7-8).

Elemed (see p. 46505-6, sections 1.2.1; 3.2; 9.1)

Alphaliner ups 2017 container volume growth forecast to 6.4\%

Alphaliner surveyed 75\% of the world’s top 200 container ports with the third quarter volume growth of 7.7\% above that of 5.8\% and 7.4\% growth in the first and second quarters of the year. As a result the analyst has increased its forecast for full year container volume growth to 6.4\% from 6\% previously.

The highest growth was seen in the Latin American region with volumes up 10\% as a whole.

Typically strong volume is expected to result in more or upgraded services in the Latin American trades.

“The strong volume recovery in Latin America could lead to a major revamp of Asia- South America services in the coming months. New tonnage is expected to be introduced as carriers vie for market share following Maersk’s acquisition of Hamburg Süd,” Alphaliner’s weekly report said.

Chinese ports, including Hong Kong, also saw good volume growth of 9.3\% in the third quarter. Leading the way Ningbo with 13.3\% increase 6.38m teu and Guangzhou at 11.9\% to 5.2m teu in Q3 2017.

Faring rather less well in Southeast Asia was Port Klang with a 15.1\% drop in volumes to an estimated 2.81m teu in the third quarter. The Malaysian port, ranked 12th largest in the world, has been hit by the restructuring of alliances.

However, while global container volumes showed good growth lines continue to face issues with overcapacity.

“Despite the high volume growth rate recorded in the third quarter, carriers have largely failed to capitalise on the improved demand conditions,” Alphaliner commented.

“Total effective capacity growth has outpaced the growth in demand, reaching 8.1\% at the end of September this year, due to the combined effects of new ship deliveries and a reduction in the idle fleet.”

The growth in capacity has put pressure on container freight rates which fell 4\% last week alone.

http://www.seatrade-maritime.com

![]()

Powered by ![]() © Μaritimes 2019

© Μaritimes 2019