North P&I Club opens new Piraeus office

|

| Tony Allen, Regional Director, North P&I |

Centrally located in Piraeus, the new office, which has over 560 square feet of office space, is designed to hold more than double the current number of staff and reflects the Club’s commitment to future growth in the region. The Club announced a raft of external lateral hires and internal promotions to their Greek team last month.

Designed to mirror the look and feel of North P&I’s global headquarters in Newcastle, the office features an open floor plan design, collaborative workspaces and a suite of meeting rooms. The new office demonstrates the Club’s ongoing commitment to the Greek market and Piraeus and will be available as a valuable resource for our local Membership. In addition, the expanded office space gives greater flexibility for our staff to meet the ever changing needs of our Members.

As the new office formally opens on the 17 September, two new additional members of staff will be joining the Piraeus team. Claims executives Lucie Ryan and Angelina Kofopoulou, will relocate from Newcastle to the new office in Piraeus to further enhance the services provided by the local team.

Regional Director Tony Allen commented “This is an exciting time to be part of North’s Greek team. I’m thrilled to see the new office open and our expanded team fully settled in their new home. North’s singular focus on delivering excellent member service has seen the range of services delivered locally from this team develop dramatically over the past few years. The new office will bring us much closer to our existing local members, helping us to continue developing and delivering service excellence.”

North’s Purpose: to enable our members to trade with confidence.

North P&I Club is a leading global marine insurer providing P&I, FD&D, war risks and ancillary insurance to 195 million GT of owned and chartered tonnage. Through its guaranteed subsidiary Sunderland Marine, North is also a leading insurer of fishing vessels, small craft and aquaculture risks. The Standard and Poor’s ‘A’ rated Club is based in Newcastle upon Tyne, UK with regional offices and subsidiaries in China (Hong Kong and Shanghai), Greece, Japan, Singapore and Sunderland Marine offices worldwide. North is a leading member of the International Group of P&I Clubs (IG), with over 12\% of the IG's owned tonnage. The 13 IG clubs provide liability cover for approximately 90\% of the world's ocean-going tonnage and, as a member of the IG, North protects and promotes the interests of the international shipping industry. For further information visit: www.nepia.com.

GAC UK becomes the fourth GAC agency in the world to support Green Award

|

| GAC UK MD Herman Jorgensen Green Award Chairman Dimitrios Mattheou and Executive Director Jan Fransen (2) |

GAC UK encourages quality shipping and environmentally friendly practices through the Green Award scheme. Green Award provides a platform to maritime organisations and companies for promotion of the best practices and elimination of sub-standard shipping on a voluntary basis. The global ship agent follows GAC Belgium, GAC Netherlands and GAC Shipping Greece and has becomes the fourth GAC agency that has joined Green Award.

Green Award Chairman Mr Dimitrios Mattheou accompanied by Green Award’s executive director Mr Jan Fransen, wholeheartedly welcomed GAC UK into the certification scheme. The ceremony took place on 6 September, 2018, in Athens (Greece).

Handing over a Green Award board to Herman Jorgensen, Managing Director at GAC UK, Mr Mattheou said: “At Green Award we aim at promoting high safety, quality and environmental standards within the maritime community on a voluntary basis. The realization of the importance of and a strong will to change for the best, to support the best practices and excellence in shipping, are crucial for achieving sustainable results. We are glad that GAC Group, which is a perfect example of such a strong will, is so consistently committed to this approach and enrolls its fourth agency to Green Award. It is unique as they are the first and only ship agent with 4 branches in our system. They demonstrate their dedication to Corporate Social Responsibility principles and contribute to recognition of frontrunners of the maritime industry.”

Herman Jorgensen added: “GAC UK has taken numerous measures to promote sustainability in its business and beyond. We welcome initiatives like Green Award which are good for the environment and great for business, too. Signing up to Green Award underlines our commitment to improving the environment by supporting shipowners and operators with the same ethos, recognizing and rewarding companies with a 10\% reduction on GAC UK ship agency fees.”

About GAC Group

GAC is a global provider of integrated shipping, logistics and marine services. Emphasising world-class performance, a long-term approach, innovation, ethics and a strong human touch, GAC delivers a flexible and value-adding portfolio to help customers achieve their strategic goals.

Established since 1956, the privately-owned group employs over 9,000 people in more than 300 offices worldwide.

Sign up for GAC’s free HOT PORT NEWS email for daily updates from ports around the world and RED HOT PORT NEWS for free SMS alerts of breaking news at www.gac.com/hpn.

Follow GAC Group on Facebook at www.facebook.com/GACGroup and LinkedIn at www.linkedin.com/company/gac-group

About Green Award Foundation

Green Award certifies sea-going oil and chemical tankers, bulk carriers, LNG and LPG carriers, container carriers, inland navigation barges and inland passenger ships. Its assessment criteria cover environmental, quality and safety aspects, and performance of management and the crew. With this comprehensive approach and a diverse team of the industry’s experts supporting the scheme, Green Award secures the quality of its audits and real value of its certificate.

With over 120 ports and other maritime related organisations providing discounts to the certified companies and ships, the scheme motivates ship owners and managers to invest in the improvements on board and ashore and serves as a reliable Corporate Social Responsibility and risk reduction tool for participating shipping companies, ports and maritime service providers.

www.greenaward.org

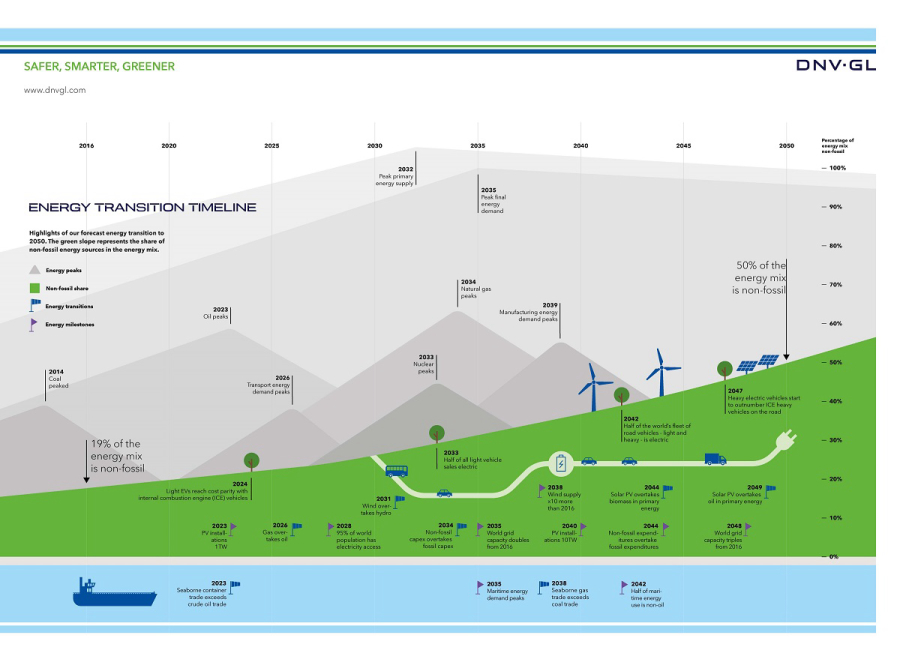

DNV GL: Energy transition offers innovators a competitive edge through “carbon robust” ship designs

|

| The DNV GL Maritime Forecast to 2050 provides an independent forecast of the maritime energy future and examines how the energy transition will affect the shipping industry. |

“The energy transition is undeniable,” says Remi Eriksen, Group President and CEO of DNV GL. “Last year, more gigawatts of renewable energy were added than those from fossil fuels and this is reflected in where lenders are putting their money.”

Following on from the 2017 report, the new Maritime Forecast to 2050 focusses on the challenges of decarbonizing the shipping industry. It examines recent changes in shipping activity and fuel consumption, future developments in the types and levels of cargoes transported, and future regulations, fuels and technology drivers.

“Decarbonization will be one of the megatrends that will shape the maritime industry over the next decades, especially in light of the new IMO greenhouse gas strategy,” says Knut Ørbeck-Nilssen, CEO DNV GL – Maritime. “Combined with the current and future trends in technology and regulations, this means that investment decisions should be examined through a new lens. Therefore, we propose a ‘carbon robust’ approach, which looks at future CO2 regulations and requirements and emphasizes flexibility, safety, and long term competitiveness. With this new framework, we hope to help empower robust decision making on assets.”

In the first Maritime Forecast, DNV GL introduced the concept of the “carbon robust” ship. The 2018 Forecast develops this concept with a new model that now evaluates fuel and technology options by comparing the break-even costs of a design to that of the competing fleet of ships. This aims to support maritime stakeholders in evaluating the long-term competitiveness of their vessels and fleet and to future-proof their assets.

A case study utilizing the model in several vessel designs reveals some striking findings, including that investing in energy efficiency and reduced carbon footprint beyond existing standards can increase the competitiveness of a vessel over its lifetime. The study also suggests that owners of high-emitting vessels could be exposed to significant market risks in 2030 and 2040.

“The uncertainty confronting the maritime industry in increasing as we head towards 2050. This makes it more important than ever before to examine the regulatory and technological challenges and opportunities of future scenarios to ensure the long-term competitiveness of the existing fleet and newbuildings,” said Knut Ørbeck-Nilssen.

The Maritime Forecast predicts a rise of nearly a third (32\%) in seaborne-trade measured in tonne-miles for 2016–2030, but only 5\% growth over the period 2030–2050. This is based on the results of DNV GL’s updated global model, which is described in detail in the DNV GL Energy Transition Outlook 2018. The model encompasses the global energy supply and demand, and the use and exchange of energy within and between ten world regions.

You can watch a livestream of the event and download the full report here: https://eto.dnvgl.com/2018/maritime

About DNV GL

Driven by our purpose of safeguarding life, property and the environment, DNV GL enables organizations to advance the safety and sustainability of their business. We provide classification, technical assurance, software and independent expert advisory services to the maritime, oil & gas and energy industries. We also provide certification services to customers across a wide range of industries. Operating in more than 100 countries, our professionals are dedicated to helping our customers make the world safer, smarter and greener.

About DNV GL – Maritime

DNV GL is the world’s leading classification society and a recognized advisor for the maritime industry. We enhance safety, quality, energy efficiency and environmental performance of the global shipping industry – across all vessel types and offshore structures. We invest heavily in research and development to find solutions, together with the industry, that address strategic, operational or regulatory challenges. For more information visit www.dnvgl.com/maritime

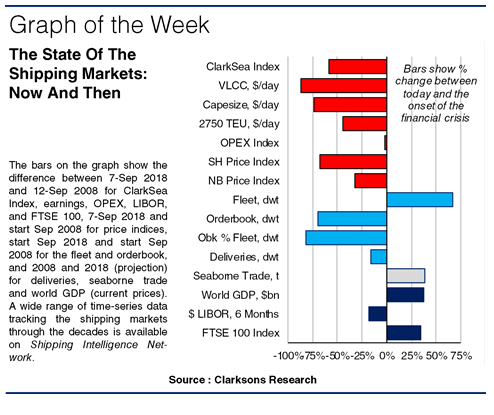

10 Years On From Lehman, How Is Shipping’s “Hangover”?

To a shipping industry used to extreme cycles but transitioning to recession with rapid trade collapse and a huge newbuilding orderbook the initial shock was severe and the “hangover” prolonged. This week’s Analysis compares the situation almost ten years to the day.

Bye Bye Boom…

Even for an industry well used to severe cycles (and with warning signals if you looked hard enough), after five years of freight rates sustained at levels not seen for a century, the transition to recession after Lehman was dramatic. The most catastrophic collapse was in Capesize. From surging to a frenzied $300,000/day in June 2008 (fanned by a $180/t iron ore price, stockpiling and congestion) earnings collapsed to $6,000/day in October and $2,000/day in November. Initially the tanker market was more stable, helped by single hull conversion and trader storage, while the container market saw 12\% of the fleet laid up by late-2009.

Not The 80s Revisited?

As our graph shows, unsurprisingly rates and prices today sit well below the week preceding Lehman. But although the shipping recession has felt prolonged, it’s been far from a “dead” decade with surprising upside at times. Even in 2009, Capesize earnings rose to $70,000/day as China’s steel output yo-yoed. There were also spikes in LNG (2012), LPG (2014-5), tankers (2015) and offshore (2013-14); and heavy (over!) newbuild ordering (2010, 2013) and record years for S&P (2017), so plenty of business has been done, helped by low interest rates. Arguably the container sector has had the most pain (but it’s a close call, and spare a thought for the bankers?).

Shipyard Surge...

Although shipyard output has dropped by 16\% over the ten years (to 80m dwt), that’s far from the whole story! Having built up a record backlog (c.650m dwt, a daunting 55\% of the fleet) and at prices that “on paper” were very profitable, the unravelling of the financial and contractual complexities became an appallingly complex task (especially with 30\% of the capacity involved “greenfield”, and financial structures such as the KG). With analysts tracking cancellation and slippage closely, shipyard production eventually peaked in 2011 (the fastest output growth in peace time). At times fleet growth has felt relentless (peaking at 9\% in 2011, a more helpful 2.6\% in 2018) as shipbuilding has worked through its overcapacity. Although demolition has doubled in the ten years since, the world fleet is still a staggering 67\% larger today (1.96m dwt!) than at the onset of the financial crisis.

Trading Up?

The immediate sea trade deterioration was severe, with volumes declining for only the second time in 30 years in 2009 (by 4\%, with oil down 3\%, dry bulk down 3\% and containers down 9\%). Trends since have been more encouraging, with a 38\% increase (exactly the same \% as GDP growth) to 12.0bn tonnes (big winners include dry bulk (+1.7bt), supported by a series of Chinese fiscal stimulus and infrastructure investments). After a “tough” ten years, that’s a more positive note to end on! Have a better decade!

The author of this feature article is Stephen Gordon. Any views or opinions presented are solely those of the author and do not necessarily represent those of the Clarksons group.

The world’s energy demand will peak in 2035 prompting a reshaping of energy investment

London, September 10 2018 – Global spending on energy, as proportion of economic output, is set to slow sharply because the world’s energy demand will decline from 2035 onwards - that is according to DNV GL’s Energy Transition Outlook. The historically significant change in our energy needs is largely down to rapid electrification and its inherent efficiency.

The decarbonization of the energy mix will be reflected in investment trends with money spent on renewables set to triple by 2050. Conversely, fossil fuel spending will drop by around a third. Overall, the rate of energy expenditure will slow to such a degree that by mid-century, as a percentage of GDP, the world will be spending 44\% less than today.

- Electrification and its inherent efficiency will contribute to humanity’s energy demand declining from the mid-2030s onwards

- Global expenditure on energy, as a percentage of GDP, will fall 44\% by 2050

- Energy mix is rapidly decarbonizing; coal has peaked, oil will peak in 2023 and natural gas will become largest single source from 2026. Renewables and fossil fuels to equally share supply by mid-century.

- The rapid transition we forecast will not be fast enough to meet the sub-2 ⁰C climate goal. A strong combination of several measures is the only way for the world to meet the ambitions of the Paris Agreement.

Since the Industrial Age, economic growth and energy usage have grown hand in hand but that relationship is set to decouple definitively in 2035 when energy demand will start to drop and GDP continues to rise.

“The attention of boardrooms and cabinets should be fixed on the dramatic energy transition that is unfolding. As money and policy increasingly favour gas and renewables, the rapidly electrifying energy system will deliver efficiency gains that outpace GDP and population growth. This will result in a world needing less energy within half a generation from now,” said Remi Eriksen, Group President and CEO of DNV GL. “The transition is undeniable. Last year, more gigawatts of renewable energy were added than those from fossil fuels and this is reflected in where lenders are putting their money.”

Fossil fuels will play an important if reduced role in our energy future with its share of the energy mix set to drop from around 80\% today to 50\% by the middle of the century, with the other half provided by renewables. Natural gas will become the single largest source in 2026 and it will meet 25\% of the world’s energy needs by 2050. Oil will peak in 2023 and coal has already peaked. Solar PV (16\% of world energy supply) and wind (12\%) will grow to become the most significant players amongst the renewable sources with both set to meet the majority of new electricity demand.

The electrification trend is already enveloping the automotive industry. By 2027 half of new cars sold in Europe will be battery powered and the same will be true five years later in China, India and North America. This will contribute to an overall reduction in the transport sector's share of global energy demand from 27\% to 20\% by 2050.

The reduced requirement for energy will be reflected in investment with overall expenditure set to drop to 3.1\% of global GDP from 5.5\% today. As fossil fuels will have a smaller slice of a smaller pie, spending will fall by around a third to USD 2.1 trillion. This will be offset by the tripling of both renewables (USD 2.4 trn) and grid expenditure (USD 1.5 trn). The nature of the spending will also alter with wind and solar projects typically requiring greater upfront CAPEX and then less operating expenditure, the opposite to oil and gas.

The planet is set to warm beyond the 2 degree limit as set by the Paris Agreement, although the affordable nature of the energy transition means there is capital available for extraordinary measures to further reduce carbon emissions. There is no silver bullet and energy efficiency, renewables and carbon capture and storage (CCS) must all be ramped up to combat climate change.

“We need to capitalize on the affordability of the energy transition and take extraordinary measures to create a sustainable future. We have a window of opportunity to increase energy efficiency, renewable energy and carbon capture and storage to meet the Paris Agreement but we must act now,” said Eriksen.

DNV GL serves both the renewables and oil & gas industries and the Energy Transition Outlook has become a leading impartial voice on the energy future. In its second year, the model has been refined further and has produced a more aggressive electrification forecast (45\% of energy demand by carrier versus 40\%) whilst the total energy demand is slightly higher (6\%).

- Published: 10 September 2018

- Author: Peter Lovegrove

Peter Lovegrove

Media Relations and Video Production Manager

Phone: +47 409 04 294

This email address is being protected from spambots. You need JavaScript enabled to view it.

For images, graphs and videos related to the Outlook click here

To download the reports click here

To download the Maritime Forecast to 2050, where our wider outlook for the maritime industry is presented click here

Shipping is increasingly caught in the trade war line of crossfire

BIMCO’s chief shipping analyst Peter Sand comments “85.3\% of Chinese seaborne imports from the US and 58.5\% of US seaborne imports from China could become affected by the trade war, if the US and China implement tariffs on a further USD 200 and USD 60 billion worth of goods respectively.

The dry bulk shipping industry is the most affected in terms of volumes largely due to the Chinese tariffs, but the whole trade war still impacts only 1.9\% of total dry bulk seaborne trade in 2017. 2,002 Handymax loads are now affected.

This is equal to the impact on the container shipping industry which also sees 1.9\% of total containerized seaborne trade affected.

For the first time in this trade war, the latest round has seen China unable to respond equally to the USD 200 billion measures announced by the US. With China importing much less than it exports to the US, if the trade war continues to unfold, China will have to look away from tariffing imports to find its retaliatory measures.

This trade war is constantly developing, in size as well as shape, with nothing looking like an end game yet. The next steps – are likely to see China using new “weapons”. For example, including service sectors or targeting US investments in China. The next steps from the US are set to morph too. The impact on the global shipping industry will depend on the measures taken.”

The US: Container shipping will be seriously hit by the next crossfire

From 23 August 2018, the second part of the USD 50 billion list, worth USD 16 billion, originally announced in late May, has been tariffed with commodities such as plastics and oil products targeted. The first list, worth USD 34 billion came into force on 6 July 2018 and targeted mainly machinery and electronic goods.

The US also published a list of goods worth USD 200 billion which it planned to add 10\% tariffs to. They have later raised the proposed tariff levels to 25\%. This list covers more consumer goods than previously seen varying from bicycles to fish and Christmas lights, and will undergo further review before a decision is made about possible implementation.

These rounds come after the US imposed 25\% and 10\% tariffs on steel and aluminium which the US announced on 8 March 2018 and now apply to all but four countries, namely Australia, Brazil, South Korea and Argentina. This is after temporary exemptions granted to the EU, Canada and Mexico were removed as of 1 June 2018.

Of the goods which already face tariffs, namely the targeted steel and aluminium commodities and the USD 34 billion worth of goods, most are dry bulk and container goods. 23.3 million tonnes of the affected steel and aluminium commodities were imported by the US via the sea in 2018. Dry bulk commodities will also be affected if the USD 200 billion list is implemented, with 4.1 million tonnes of the targeted commodities imported to the US from China in 2017, these goods include wood commodities and cements. In total the dry bulk goods affected by US tariffs are equivalent to 548 Handymax loads (50,000 DWT).

While containerized goods have already been targeted, by the USD 50 billion round, the biggest impact on these will come if the proposed USD 200 billion are implemented. So far, the tariffed goods total to 6.6 million tonnes of seaborne trade from China to the US in 2017.This is equivalent to 660,000 TEU (10 tonnes per TEU/global average), which amounts to 5.9\% of US West Coast container imports in 2017. If you assume a lighter/heavier cargo per transported TEU or FEU, naturally the number of containers change accordingly.

A further 22.4 million tonnes of seaborne containerized goods would be impacted by the US 200 billion list, which amounts to a further 20.1\% of USWC imports in 2017, or 2.24 million TEU. In total, if this latest round of tariffs were also to be implemented, 1.5\% of the global seaborne container trade would be affected.

Oil products have also been targeted with 0.5 million tonnes worth of this seaborne trade tariffed from 23 August with a further 0.7 million tonnes in the line of fire of the USD 200 billion list.

China: Running out of Ammunition

The Chinese USD 16 billion list also came into force on 23 August 2018, a modified list compared to the original publication, with the removal of crude oil an important development. This revised list contains wood commodities as well as some coals and metals.

Following the publishing of the USD 200 billion list by the US, China responded by releasing four lists worth in total USD 60 billion, to be tariffed between 5\% and 25\%. This contrasts to the prior rounds of the trade war, where every retaliation has been of equal worth to the other party’s measure. However, the trade war has now reached a stage where China is unable to respond equally as it imports much less from the US than it exports. In 2017 they imported USD 129 billion worth of US goods and having already targeted or proposed tariffs on USD 113 billion of US imports, China is fast running out of goods to tariff. This compares to the almost USD 506 billion worth of goods that the US imported from China in 2017, leaving them with more room for manoeuvre.

China has previously put tariffs on USD 3 billion worth of American goods, in response to the American steel and aluminium tariffs. These are primarily food, beverages, iron and steel products. The next retaliation from China came in the form of tariffs on a list of products worth USD 34 billion which entered into force 6 July, matching both the American date and list value.

The dry bulk shipping industry remains by far the most affected by Chinese tariffs in terms of volumes. The largest ‘one commodity’ targeted by the trade war are US soybeans which as of 6 July 2018 face 25\% tariffs when imported into China, but the impact of these on Chinese buyers may be limited. A fall in the price of US soybeans since the tariff’s implementation, has resulted in US soybeans being 21\% cheaper than Brazilian soybeans (Source: Bull Positions), the second largest exporter of soybeans to China, thus eroding much of the added costs brought about by the tariffs.

By excluding crude oil imports from its USD 16 billion list, China has halted tariffs on 10.5 million tonnes worth of seaborne crude imports from the US. Instead the most recently implemented tariffs target mainly dry bulk goods, amounting to 22.2 million tonnes. The proposed USD 60 billion would also affect the dry bulk industry the most, with 10.5 million tonnes of listed dry bulk commodities shipped from the US to China. In 2017, 72.2 million tonnes of the involved commodities (both with tariffs implemented and proposed) were imported via the sea by China from the US. This represented 1.4\% of total seaborne dry bulk trade in 2017 and is equivalent to 1,454 Handymax loads (50,000 DWT).

“While the narrowly measured amount of impacted cargoes may seem small in perspective of the entire market – the impact is the opposite. The shipping industry is trapped between a rock and a hard place in an already troubled market place.

In the tramp shipping market, uncertainty about where the next cargo will come from makes it very difficult to reposition your ship after discharge. For the liner shipping market, matching deployed capacity on trade lanes with actual demand becomes even harder.

Poorer service offers to customers and lower profitability seems inevitable”, ends Peter Sand.

bimco.org

World Maritime Day theme 2019: "Empowering Women in the Maritime Community"

This will provide an opportunity to raise awareness of the importance of gender equality, in line with the United Nations' Sustainable Development Goals (SDGs), and to highlight the important contribution of women all over the world to the maritime sector.

|

The Council of the International Maritime Organization (IMO), meeting for its 120th session at IMO Headquarters in London, endorsed the theme, following a proposal by IMO Secretary-General Kitack Lim.

“IMO has a strong commitment to helping achieve the Sustainable Development Goals (SDGs) and continues to support the participation of women in both shore-based and seagoing posts, in line with the goals outlined under SDG 5: 'Achieve gender equality and empower all women and girls',” Mr Lim said.

“This theme will give IMO the opportunity to work with various maritime stakeholders towards achieving the SDGs, particularly SDG 5, to foster an environment in which women are identified and selected for career development opportunities in maritime administrations, ports and maritime training institutes and to encourage more conversation for gender equality in the maritime space,” Mr. Lim said.

While shipping has historically been a male dominated industry, IMO has been making a concerted effort to help the industry move forward and help women achieve a representation that is in keeping with twenty-first century expectations. This work has been focused through IMO's gender and capacity building programme, which is now in its thirtieth year.

Back in 1988, few maritime training institutes opened their doors to female students. IMO was in the vanguard of United Nations specialized agencies that forged a global programme known as the Integration of Women in the Maritime Sector. Carried out over several phases, it put in place an institutional framework to incorporate a gender dimension into IMO's policies and procedures, with resolutions adopted to ensure access to maritime training and employment opportunities for women in the maritime sector.

“Today, IMO's newly renamed, Women in Maritime programme is going strong. Empowering women fuels thriving economies across the world, spurs growth and development, and benefits all of us working in the global maritime community as we strive towards safe, secure, clean and sustainable shipping,” Mr. Lim said.

Female graduates of IMO’s global training institutes, the World Maritime University (WMU) and the International Maritime Law Institute (IMLI) are today working as maritime administrators and decision makers. They have a positive impact as role models in encouraging new female recruits. IMO also supports the empowerment of women through gender-specific fellowships; by facilitating access to high-level technical training for women in the maritime sector in developing countries.

IMO has supported the creation seven regional associations for women in the maritime sector across Africa, Asia, the Caribbean, Latin America, the Middle East and the Pacific Islands. Access to these regional networks have provided members with a platform to discuss gender issues; a golden thread of worldwide maritime communication and improved implementation of IMO instruments.

The selection of the theme, "Empowering Women in the Maritime Community" will ensure a renewed focus on the IMO women in maritime programme, and on achieving the goals of SDG 5, throughout 2019.

imo.org

Strong support for Copenhagen Shipping Summit

|

Michael Lund, Deputy General Secretary, BIMCO states: “BIMCO is very much looking forward to be part of the first Copenhagen Shipping Summit. BIMCO will contribute with a Power Panel Discussion addressing key developments impacting shipping business today, with the focus on challenges and future prospects for the dry-bulk and oil tanker shipping markets, including the 2020 global sulfur cap experiment.”

About the co-operation with BIMCO, Jakob le Fevre, Managing Director, Shipping Summit states: "We are extremely pleased with the cooperation. BIMCO is the world's largest shipowner association. With over 2,000 members in 120 countries, including over 1,000 shipping companies, I cannot imagine any other organization that better matches the ambitions we have with the summit "

The Engineers' Association is planning a conference the first day, focusing on Sustainable Shipping.

Jan Rose Hansen, Chairman of Danish Engineer´s Association says “Danish Engineer´s Association welcomes and supports the new initiative Copenhagen Shipping Summit. In 2017 several Danish organizations, companies and research institutions joined forces within a partnership labelled the Ocean Plastic Forum. Partners are a present five industry associations, six companies, three universities and two NGO´s operating within one legal frame. Danish Engineer´s Association act as secretariat for the partnership and we are planning a conference about this topic at the Summit. “

MDC (Maritime Development Center) will conduct an event focusing on HR & Management.

Mikkel Navarro Hansen, MD of MDC, said in this regard: "MDC contributes to MARPROS new initiative with an event that emerges from the work of MDC's HR & Crew Management Forum. MDC continuously supports the work of developing the maritime workplace of the future across the maritime value chain. Recently, MDC has kicked off the debate on More Women at Sea. MDC is pleased to meet the business on the Copenhagen Shipping Summit platform - about this and other relevant topics that can support our business's positive development."

The venue for Copenhagen Shipping Summit is The Øksne Hall and it takes place 10-11th April. The target audience is the maritime business in broad terms, but with keen focus on the Summit themes which are: The future for Shipping, Maritime Recruitment Trends - ashore and at sea, Empowering Women in the Maritime Community and Sustainable Shipping. A large Executive Dinner in the H C Andersen Castle in Tivoli will take place the first day after the conferences.

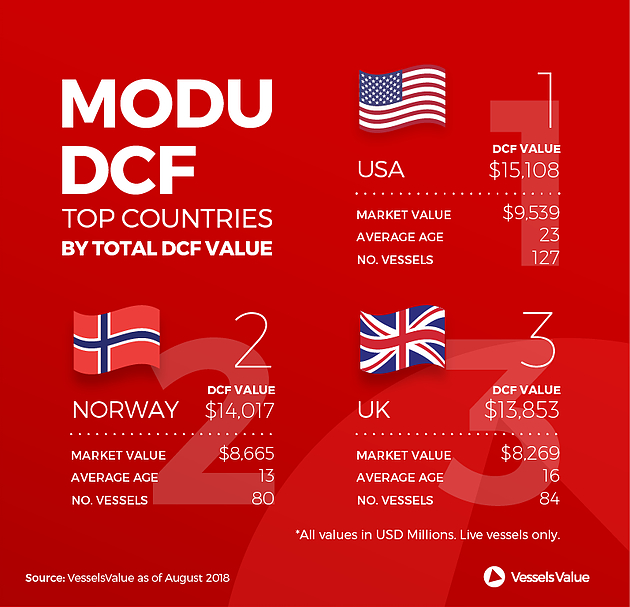

American MODU DCF Value 1.5 times higher than Market Value

By comparing DCF values to Market values, customers of VesselsValue can look for buy/sell/hold signals. For instance, if you can purchase a vessel when the market value is lower than the DCF value, you could potentially earn more money over the course of its lifetime than you spent. Therefore, this is a buy signal.

On the other hand, if the DCF value is lower than its market value, this implies you can sell the vessel for more than it will earn you for the rest of the vessel’s life.

|

The US MODU DCF Value is currently 1.5 times higher than its Market Value, today valued at $15.1 billion and $9.5 billion respectively, making it the highest valued MODU fleet globally by both measures.

In second place, with a much smaller and younger average aged fleet, are the Norwegian MODUs, which have a total DCF value of $14 billion compared to a Market Value of $8.7 billion.

TOP Ships Inc. Announces Credit Committee Approval for up to $92.5 Million in Financing for Two Suezmax Newbuilding Vessels

Under the proposed terms of the Financing Agreements, the vessels will be sold when they are delivered from the shipyard, which is currently planned for April and May of 2019, respectively. The proposed Financing Agreements include pre and post-delivery financing and have a term of seven years. The Company has continuous options to buy back the vessels after the three year anniversary of each vessel’s delivery up until the expiry of the Financing Agreements.

As previously announced, upon their deliveries the vessels are scheduled to enter into three year time charters with an oil major at a daily charter rate of $25,000 per vessel.

Evangelos Pistiolis, the President, Chief Executive Officer and Director of the Company, said:

“Successful completion of this transaction would mark two very important milestones; significant reduction of our unfunded capital requirements, as this funding would cover about 84\% of the remaining yard installments required in order to take delivery of the Suezmax vessels which are the assets with the most capital requirements in our orderbook, and entry into the Chinese financing market.”

Overview of financing of remaining yard installments:

M/T Eco California (expected delivery January 2019): Pre-delivery loan facility: secured 100\% of remaining pre delivery installments / Post-delivery finance: in discussions with various financiers.

M/T Eco Marina Del Ray (delivery March 2019): Pre-delivery loan facility: secured 100\% of remaining pre delivery installments / Post-delivery loan facility: in place.

M/T Eco Bel Air (Hull No 874 – delivery April 2019): Pre-delivery loan facility: Credit Committee approval obtained for about 55\% of remaining pre delivery installments / Post-delivery loan facility: Credit Committee approval obtained, currently negotiating final terms.

M/T Eco Beverly Hills (Hull No 875 – delivery May 2019): Pre-delivery loan facility: Credit Committee approval obtained for about 55\% of remaining pre delivery installments / Post-delivery loan facility: Credit Committee approval obtained, currently negotiating final terms.

Additionally the Company is in discussions with new financiers as well as its existing senior secured lenders for drawing down additional funds from the Company’s outstanding loan facilities that currently have low loan to value ratios, which are secured by the Company’s existing vessels. The Company is also in discussions with its CEO and controlling shareholder, Mr. Evangelos Pistiolis, for an increase in the Family Trading credit line.

Source: TOP Ships Inc.

![]()

Powered by ![]() © Μaritimes 2019

© Μaritimes 2019