Maritime piracy report sees first Somali hijackings after five-year lull

The global report highlights persisting violence in piracy hotspots off Nigeria and around the Southern Philippines – where two crew members were killed in February. Indonesia also reported frequent incidents, mostly low-level thefts from anchored vessels.

In total, 33 vessels were boarded and four fired upon in the first three months of 2017. Armed pirates hijacked two vessels, both off the coast of Somalia, where no merchant ship had been hijacked since May 2012. Four attempted incidents were also received.

IMB’s Piracy Reporting Centre has monitored attacks on the world’s seas since 1991. The report highlights three major concerns:

1. Gulf of Guinea kidnappings

Of the 27 seafarers kidnapped worldwide for ransom between January and March 2017, 63\% were in the Gulf of Guinea. Nigeria is the main kidnap hotspot, with 17 crew taken in three separate incidents, up from 14 in the same period last year. All three vessels – a general cargo ship, a tanker and a bulk carrier – were attacked while underway 30-60 nautical miles off the Bayelsa coast. Three more ships were fired upon at up to 110 nautical miles from land, and many other attacks are believed to go unreported.

“The Gulf of Guinea is a major area of concern, consistently dangerous for seafarers, and signs of kidnappings increasing. IMB has worked closely with the response agencies in the region including the Nigerian Navy which has provided valuable support, but more needs to be done to crack down on the area’s armed gangs,” said Pottengal Mukundan, Director of IMB. “We urge vessels to report all incidents so that the true level of piracy activity can be assessed.”

2. Growing violence around the Southern Philippines

Here, nine ships reported attacks in the first quarter of 2017 compared with just two in the same period last year. These include an armed attack on a general cargo vessel in which two crew were killed and five kidnapped for ransom. Kidnappers captured five more people in attacks on a fishing trawler and a tug.

According to IMB, militant activity may be behind the escalating violence in waters around the Southern Philippines. Armed groups use speedboats to target seafarers and fishermen in slow-moving, low vessels.

Areas such as the Sulu Sea and Sibutu Passage are particularly risky. IMB recommends that ships avoid these waters by transiting West of Kalimantan, if possible – and, as ever, follow the industry’s latest best practice measures, to protect against attacks.

3. First Somali hijackings after five-year lull

Somali pirates successfully hijacked a small bunkering tanker and a traditional dhow, both within their territorial waters. A total of 28 crew were taken hostage and subsequently released within a relatively short time. IMB suspects that these incidents were opportunistic, particularly as the hijacked vessels were not following the Best Management Practices for Protection against Somalia Based Piracy (BMP4) recommendations.

“IMB continues to encourage all vessels transiting waters around Somalia to follow the BMP4 recommendations. The recent attacks should serve as a warning against complacency, as Somali pirates are still capable of carrying out attacks,” said Mr Mukundan.

“The presence of international navies who patrol these waters is extremely important as it provides an added layer of deterrence to the pirates and more importantly helps to secure one of the most important trade routes of the world,” he added.

The IMB Piracy Reporting Centre supports the anti-piracy efforts of international navies by relaying all reports to the response agencies, as well as broadcasting alerts to ships via the INMARSAT Safety Net Service.

Piracy and armed robbery prone areas worldwide

IMB’s latest piracy report gives detailed descriptions of all 43 attacks in 16 countries, and advice for mariners, including a list of particularly high-risk areas where extra caution and precautionary measures are vital.

The IMB Piracy Reporting Centre is the world’s only independent 24-hour manned centre to receive reports of pirate attacks from around the world. IMB strongly urges all shipmasters and owners to report all actual, attempted and suspected piracy and armed robbery incidents to the IMB PRC. This first step in the response chain is vital to ensuring that adequate resources are allocated by authorities to tackle piracy. Transparent statistics from an independent, non-political, international organisation can act as a catalyst to achieve this goal.

Source: IMB (International Maritime Bureau)

Morocco phosphate ship held in South Africa port over Western Sahara claim

The seizure of the vessel, carrying 50,000 tonnes of phosphate to New Zealand, may be a test for the Polisario's use of a European court decision last year that ruled Western Sahara should not be considered part of the Moroccan kingdom in EU and Moroccan deals.

Western Sahara has been disputed since 1975 when Morocco claimed it and the Polisario movement fought a guerilla war for the Sahrawi people's independence there. A ceasefire in 1991 split the region in two between what Morocco calls its southern Sahara and an area controlled by Polisario.

The two sides have been since locked in diplomatic and legal tussles though tensions flared last year when U.N. peacekeepers had to step in between Moroccan forces and Polisario brigades in the buffer zone near the Mauritania border.

The Marshall Island-flagged NM Cherry Blossom, carrying phosphate from Laayoune in the Moroccan part of the disputed territory for state-run OCP, has been held in Port Elizabeth by a civil maritime court order, OCP said.

"The order issued in South Africa regarding the cargo of the NM Cherry Blossom is a standard temporary measure made on the basis of only one party's allegations," OCP legal counsel Othmane Bennani Smires told Reuters by telephone.

"We are fully confident of a favourable resolution once the actual facts of this case are presented to the South African court."

He said OCP's Phosboucraa subsidiary and its activities are in full compliance "with the United Nations framework and relevant international legal norms and standards".

The sparsely populated stretch of desert bordering the Atlantic Ocean, Western Sahara has rich offshore fishing as well as phosphate and possibly oil reserves. OCP, or Office Cherifien de Phosphate (OCP) is the world's leading phosphate exporter.

Southern African maritime authorities were not immediately available to comment or confirm details but OCP confirmed the other party in the case was Polisario.

Polisario chief negotiator Mohamed Khadad said they had filed the case based on the Western Sahara's status defined by the U.N. as a non-self governing territory, to protect its natural resources, and also based on the EU court decision.

"There is no possibility to exploit the natural resources of the Western Sahara without the consent of the people of the Western Sahara," Khadad told Reuters.

"We are convinced, we have been following it from the port of the Laayoune," he said. "It is a matter of law. We will abide by the last decision of the court."

In January, Morocco rejoined the African Union regional body, where Polisario's self-declared Sahrawi Arab Democratic Republic (SADR) is also a member. South Africa along with Algeria have been key supporters of the SADR.

The NM Cherry Blossom case comes as the U.N. Security Council has backed attempts to restart talks between Morocco and Polisario for a mutually acceptable political solution to the question of the region's self-determination.

Talks have failed for years to bring an end to the dispute. Morocco wants the region to have autonomy within Moroccan sovereignty while Polisario calls for a referendum on self-determination, including on the question of independence. (Writing by Patrick Markey; Editing by Tom Heneghan)

United States (US) Regulatory, Financial, and Political Issues Affecting Shipping

IRI/The Marshall Islands Registry and Blank Rome LLP held a seminar on United States (US) Regulatory, Financial, and Political Issues Affecting Shipping on 26 April 2017 at the Metropolitan Hotel in Athens, Greece. The seminar was an opportunity for industry stakeholders to meet and discuss the current environment and the challenges ahead. The seminar was a success, with around 170 in attendance to hear the speakers and participate in the panel discussions.

Jeanne M. Grasso, Partner, Blank Rome LLP opened the first session of the seminar, focused on US regulatory and enforcement issues and moderated by Stefanos N. Roulakis, Associate, Blank Rome LLP, with a presentation on ballast water management challenges and realities. Following this, Lieutenant Samuel M. Danus, Port State Control Oversight, US Coast Guard (USCG), and Brian Poskaitis, Senior Vice President, Fleet Operations, IRI, presented on the topic of the USCG’s Qualship 21 Program. A panel discussion on operations in US waters relating to oily water separators, whistle blowers, and other legal risks, led by Jeanne M. Grasso; Gregory F. Linsin, Partner, Blank Rome LLP; George Margelis, Environmental Compliance Manager, TMS Dry Ltd; and Brian Poskaitis concluded the session.

A panel discussion, regarding sources of capital and restructuring and moderated by R. Anthony Salgado, Blank Rome LLP, comprised the second session. Participating in the panel were Jerry Kalogiratos, Chief Executive and Chief Financial Officer, Capital Product Partners L.P.; Harrys Kosmatos, Corporate Development Officer, Tsakos Energy Navigation, Ltd.; Simos Spyrou, Chief Financial Officer, Star Bulk Carriers Corp.; and Ioannis Zafirakis, Director, Chief Operating Officer and Secretary, Diana Shipping Inc.

Joan M. Bondareff, Of Counsel, Blank Rome LLP; Scott D. Hatch, Principal, Blank Rome Government Relations LLC; Stephen C. Peranich, Principal, Blank Rome Government Relations LLC; and Matthew J. Thomas, Partner, Blank Rome LLP gave a presentation on the new administration in Washington, D.C.’s policy changes and legislation affecting shipping and international trade to conclude the seminar.

At the close of the seminar, a cocktail reception was held where attendees had the opportunity to mingle with other members of the Greek shipping community.

IRI/The Marshall Islands Registry is honored to have hosted this seminar alongside Blank Rome LLP and the exemplary speakers who provided their expertise to the discussion and looks forward to holding similar informative sessions for the industry to meet and exchange ideas in the future.

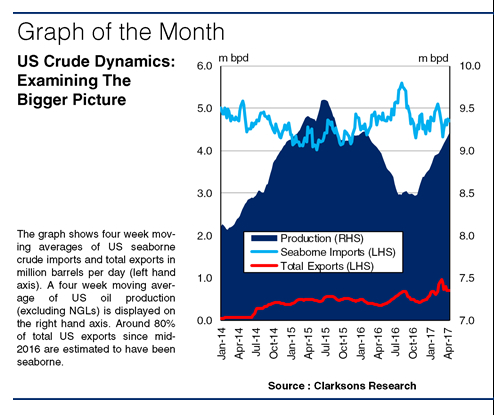

Reviewing The Situation: US Crude Trade Trends

However, there is considerable uncertainty over the trajectory of US crude volumes this year given the many different factors at play. What are the most important drivers to consider?

Ups And Downs

One key driver of changes in US crude imports is US oil production. Following the US ‘shale revolution’, 2014 saw the US become the world’s top oil producer, with output peaking at 9.6m bpd in mid-2015. However, the subsequent oil price collapse exerted pressure on shale producers, and US oil output dropped to 8.4m bpd in 2H 2016. Overall, US oil production declined by 0.40m bpd in 2016, supporting a 0.45m bpd (10\%) increase in US seaborne crude imports to 4.64m bpd. But, with domestic output rising again since late 2016 in line with an improved oil price, there are potentially negative implications for crude imports. However, there remain a range of scenarios for the oil price this year, and given the sensitivity of US producers to oil price levels, the outlook for US oil output and crude imports remain subject to uncertainty.

|

Hitting New Records

Adding an extra dimension to the current dynamics are US crude exports. The US lifted its crude export ban at the end of 2015 after 40 years, although due to the saturated international oil market and falling domestic production, US exports initially remained limited. However, since early 2017, exports have risen notably, hitting a record 1.2m bpd in February, with reports of increased shipments on long-haul routes to Asia. This has reflected the recent revival of output, improved US export infrastructure and some buyers seeking to diversify supply. Rising exports have contributed to the uncertainty over US crude imports this year, as many US refineries are geared for heavy grades of crude. If exports can provide an outlet for surplus light oil production, imports of heavy oil may not be as significantly affected by increasing output.

Even More In The Mix

Meanwhile, US crude inventories have also made headlines lately, with stocks reaching record highs of over 1.2bn bbls in February. However, in early April, stocks were drawn down for two consecutive weeks. If refineries continue to draw upon US inventories, this could potentially dent crude imports. Yet another variable is the potential fluctuations in landborne trade between the US and Canada, which could displace seaborne imports. Finally, pipeline developments such as Dakota Access and much further ahead Keystone XL, could better facilitate US refiners’ access to crude, which could also undermine US seaborne imports.

So, while the current projection is for US crude imports to soften this year, there remains uncertainty given the many factors involved. Rising US crude exports could also drive interesting changes in crude trade patterns. Thus, it remains to be seen precisely how US crude trade will develop, but the outcome either way will still be significant for the crude tanker market.

Source: Clarksons

Capital Ship Management Corp. takes delivery of the vessel C/V ‘ATHENIAN’

About Capital Ship Management Corp.![]()

Capital Ship Management Corp. (a subsidiary of Capital Maritime & Trading Corp.) is a distinguished oceangoing vessel operator, offering comprehensive services in every aspect of ship management, currently operating a fleet of 58 vessels with a total dwt of 6.18 million tons approx. The fleet under management includes the vessels of Nasdaq-listed Capital Product Partners L.P.

China, Greece to deepen ties through Belt and Road Initiative

|

| Liu Qibao (R), head of the Publicity Department of the Central Committee of the Communist Party of China (CPC), shakes hands with Greek Prime Minister Alexis Tsipras in Athens, Greece, April 27, 2017. China and Greece have agreed here to boost cooperation through the Belt and Road Initiative. (Xinhua/Ye Pingfan) |

China-Greece relations have sustained a healthy and stable development since the two countries established diplomatic relations 45 years ago, Chinese official Liu Qibao told Greek Prime Minister Alexis Tsipras on Thursday.

Liu, head of the Publicity Department of the Central Committee of the Communist Party of China (CPC), said China is willing to work with Greece to further deepen mutual political trust, mutually beneficial cooperation and people-to-people exchanges.

China is also ready to make efforts with Greece to implement the Belt and Road Initiative, thus promoting the development of the China-Greece all-round strategic partnership, said Liu.

The Belt and Road Initiative, proposed by Chinese President Xi Jinping, aims to build a trade and infrastructure network connecting Asia with Europe and Africa along the ancient Silk Road and maritime trading routes, bringing mutually beneficial economic outcomes for every nation involved.

During the meeting, Liu introduced the new ideas and new strategies of national governance put forward by the CPC Central Committee with Xi as the core.

He said the CPC is willing to deepen communication with Tsipras' Syriza party on ideas of party and state governance in order to lay a solid foundation both politically and socially for the development of the two countries' relations.

Tsipras said both the Greek government and the Syriza party attach great importance to developing relations with China and wish to take the Belt and Road Initiative as an opportunity to further advance bilateral cooperation in the fields of trade, investment, culture, science and technology, as well as tourism.

Liu led a Chinese delegation for a visit to Greece from Tuesday to Friday at the invitation of the country's ruling Syriza party.

During the visit, Liu also held talks with Kyriakos Mitsotakis, president of the New Democracy party, and participated in the launching ceremony of the "China-Greece Cultural Exchanges and Cultural Industry Cooperation Year" along with Greek Deputy Prime Minister Yiannis Dragasakis.

At the ceremony, Liu oversaw the signing of two memoranda of understanding on film co-production and translation and the publication of classic and modern Greek and Chinese literary works.

He also attended two exhibitions that opened at the inauguration, one featuring the cultural heritage of Hangzhou in eastern China's Zhejiang province, and the other showcasing the upcoming 2022 Winter Olympics to be held in Beijing and Zhangjiakou.

source:XINHUA

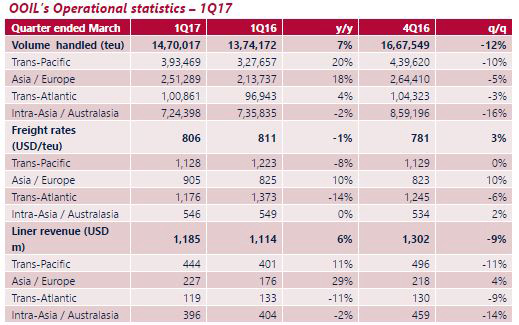

Drewry: Orient Overseas International Limited – 1Q17 operational data update

The company’s key drivers of revenue growth –Asia/Europe and Transpacific routes – recorded gains of 29\% and 11\% respectively, while the volumes on these routes increased by 18\% and 20\% during the same period. The average revenue per teu reported at USD 806 in 1Q17 is the highest in the past four quarters, but remained almost flat on y/y basis. Route wise, the rates came in 10\% higher on the Asia-Europe route, but softened on both the Transpacific and Transatlantic routes, which witnessed a negative growth of 8\% and 14\% y/y respectively. The freight rates on Intra-Asia/Australasia remained flat compared to last year. Additionally, while the loadable capacity increased by 1\%, the overall load factor was 5\% higher than in 1Q16.

|

| Source: Company, DFRS |

Rebound in Transpacific – a good omen for OOIL. A strong demand recovery in the US has been driving a rebound in the volume and spot rates for the Transpacific trade since 4Q16. When combined with the rates holding up better post the CNY holidays, this drove OOIL’s revenue and volume growth for 1Q17 on y/y basis. With the Transpacific route being one of its core revenue drivers, the developments will hold OOIL in good stead. Drewry’s data suggests that the East-West Freight Rate Index in 1Q17 was about 40\% higher than in 2016. We believe rates on both East-West trades and globally will continue to improve in 2017 and help OOIL remove its red ink from its income statements last year.

Six vessel deliveries this year could strain its balance sheet: In our view, despite OOIL being in the red in FY16, it remains a safe bet. However, its six 20k teu vessels, which are due for delivery this year, could strain its balance sheet as the company will have to fork out a lot of money when the vessels are actually delivered. Based on its FY16 results, the total cash on its book was USD 1.6bn – 19\% down compared to the previous year. Its leverage (Net-debt-to-Ebitda) was around 8x over just 3x in 2015, while net gearing rose to 46\% over 37\% in 2015, albeit still lower than the industry’s 130\%.

Valuation – maintain Attractive. We maintain our Attractive rating for OOIL as we believe a positive development in liner revenues is just around the corner. Our fair value of HKD 50 is 20\% higher than the current trading price of HKD 41.5 (as on 28 April 2017). The company has been one of our preferred players in the container shipping sector and can still deliver better earnings than its peers, supported by its effective management. The company scores a green light both on Drewry’s bespoke value and risk ranking, indicating Attractive valuation and low risk.

Source: Drewry Financial Research Services

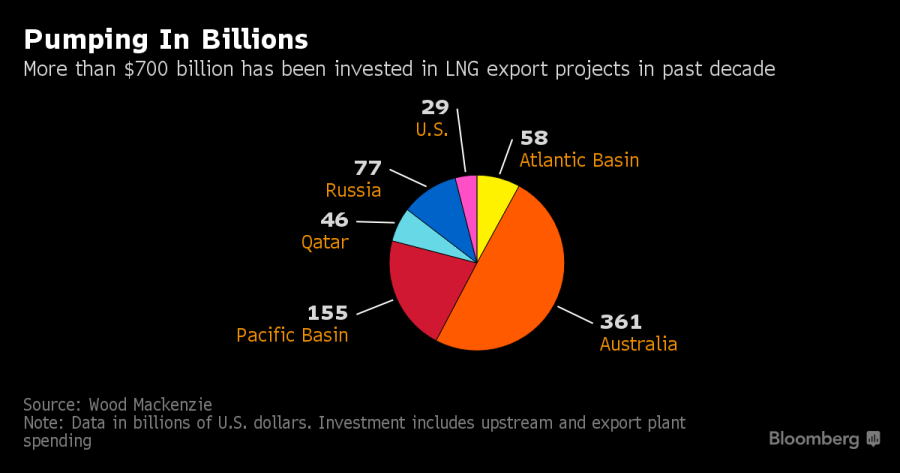

Oil Tankers to Cruise Ships Fueled by LNG Offer Hope on Glut

Sovcomflot’s Aframax ships, capable of shifting 600,000 barrels of oil through the icy waters of the Baltic Sea to the port of Rotterdam, will be the first tankers run on LNG.

That’s good news for fuel supplier Royal Dutch Shell Plc and the other energy companies that have invested more than $700 billion in LNG projects over the past decade. While ships won’t transform the market -- Energy Aspects Ltd. estimates that LNG as a marine fuel will account for less than 2 percent of total demand by 2025 -- Russian tankers and Mediterranean cruise liners will help ease a global glut.

“People need to find more customers for LNG,” said Michael Newman, a shipbroker at Fearnleys A/S in London. “Big mega-projects are increasingly being replaced by smaller trains and smaller volumes, such as those for use of LNG as a transport fuel.”

Since 2014, the spot price of LNG has dropped by two-thirds to $5.4 per million British thermal units as supply swelled, crude slumped and large buyers such as Japan and Korea slowed purchases. That’s pushing the industry to look beyond long-term contracts with power utilities to find other sources of demand.

At the same time, stricter environmental standards are pushing shipowners to consider cleaner fuels such as LNG, which contains virtually no sulfur. The International Maritime Organization will from 2020 impose a sulfur cap of 0.5 percent on marine fuel, down from the current global limit of 3.5 percent.

Against that favorable backdrop, the number of LNG-fueled ships will more than double to 200 by 2020 from 77 last year and just five in 2005, according to London-based Energy Aspects.

That will boost LNG bunkering demand, excluding fuel burned by LNG carriers, to 1 million tons in three years and as much as 5 million to 7 million tons by 2025, Energy Aspects said. Total LNG demand is forecast to rise to 364 million tons in 2025, from 260 million tons last year, according to Bloomberg New Energy Finance.

BNEF estimates that LNG oversupply will peak in 2020, before turning into a shortage after 2025.

Cruise Option

Apart from the Sovcomflot contract, Shell will also supply fuel to the world’s first LNG-powered cruise ships, which will be operated by Carnival Corp. in northwest Europe and the Mediterranean from 2019.

That will come six years after the Viking Grace -- operating between Turku in Finland and Stockholm in Sweden -- became the first large passenger ship to use LNG in January 2013.

Carnival, which has a fleet of 102 ships, has seven vessels on order that will run on LNG.

“When our ships come along, they will be some of the biggest consumers in the maritime sector” of LNG fuel, Tom Strang, senior vice-president maritime affairs at Carnival, said in an April 6 phone interview. “We are confident that there is going to be plenty of LNG. The question is, is there LNG where we need it?’’

The infrastructure to support the use of LNG in the shipping industry is expanding, with major European ports required to have bunkering for the fuel by 2025, the International Gas Union said in a report this month.

“Ports are also largely indicating the willingness to move quickly to support demand, once it begins to strengthen,” the gas lobby group said.

Bunkering Network

The Gate terminal in Rotterdam has added facilities for loading smaller vessels and bunkering operations. Shell, the terminal’s first customer, will introduce a dedicated bunkering vessel this summer, according to Stefaan Adriaens, commercial manager at Gate.

“We see an uptick in well-founded inquiries for using this jetty,” said Adriaens. The facility has attracted Skangas as its second client, he said.

Total SA agreed this month to buy LNG from Pavilion Energy Pte for onward sale to ships in the port of Singapore, one of the world’s biggest. The French oil giant wants to supply 1 million tons of LNG annually to fuel ships by 2025.

“Developing a competitive worldwide LNG bunkering network will be key for the industry,” Total Chief Executive Officer Patrick Pouyanne said in a statement on April 4.

source:bloomberg.com

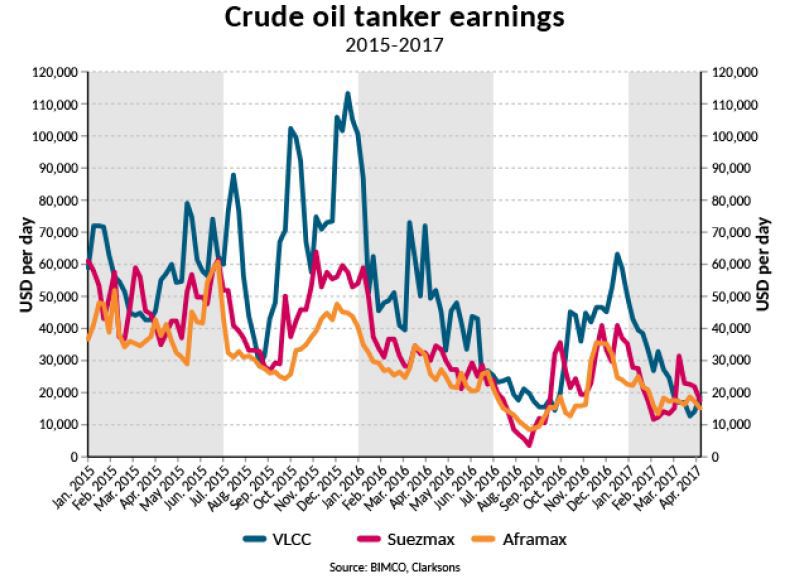

BIMCO: Tanker owners have their work cut out handling the supply side in 2017

For one, VLCCs may not yet have bottomed out. By 7 April 2017, average earnings stood at USD 18,853 per day, down from USD 63,284 per day on 16 December 2016. The demand situation for both crude oil tankers and oil product tankers in 2017 and 2018 is closely connected to the destiny of worldwide oil stocks. So far, we have seen supply cuts from OPEC, from their highest supply level ever at 33.9 mb/d in October 2016.

However, we have also seen an increase of supply from the US. This has lifted US crude oil stocks to their highest level ever, and global stocks have sidestepped. BIMCO believes that we must wait until the second half of 2017, when global oil demand picks up, to see an eventual drop in global oil stocks (crude oil and oil products). Focusing on the oil product tankers only, the month of March proved to be a relief. Handysize tanker earnings even surpassed that of all crude oil tankers, reaching USD 23,984 per day on 24 March. On that day, suezmax crude oil tankers reached only USD 22,700 per day.

Since the removal of restrictions on US crude oil exports in December 2015, this has been a developing story. It has also been an interesting one, as shipping has certainly benefited strongly and quickly. Not so much in sheer volumes, as US crude oil exports went from 465,000 barrels per day (b/d) to 520,000 b/d (+11.8\%), but exports started to find destinations globally and not just cross-border into Canada. In 2015, 92\% of US exports went north; in 2016 that share was just 61\%. The other destinations that we find in the top five include the Netherlands, Italy and China. South Korea, Japan and the UK are also amongst the importers – all served by tankers. US crude oil imports have also grown, benefiting crude oil tankers even more.

Additionally, US oil product exports keep rising, going both short-haul to Mexico, Caribs and South America and long-haul to Japan, China and India.

Supply

As discussed in our previous tanker shipping market overview and outlook, the total amount of demolished tanker capacity was very low in 2016. Owners appeared more focused on taking delivery of new ships during this time. This has now changed – at least to some extent. In 2016, 2.6 million DWT was sold for demolition. By end-March 2017, 0.9 million had left the fleet for recycling at shipbreaking facilities. Although slightly busier than 2016, it has been a slow start to what BIMCO expects will be a busy year for tanker demolition. As we expect the freight market and asset values to have yet another year under pressure. Demolitions are forecast to rise fourfold to a total level of 11.5 million DWT, out of which 9 million DWT is expected to be taken out of the crude oil tanker fleet.

BIMCO forecasts crude oil tanker deliveries in 2017 to be on a par with 2016, which saw 23 million DWT of new shipping capacity. This highlights the need to handle the supply side, as demand growth will not support the market to the extent it did in 2016. The year to date has seen 9.8 million DWT being delivered with just 0.7 million DWT of crude oil tanker capacity being demolished – including one VLCC.

In terms of new orders, 2017 has seen 12 VLCCs and 8 LR2s amongst others. There have been 38 new orders in total for 5.7 million DWT, including 16 product tankers with a total capacity of 1.3 million DWT. The 12 VLCCs and other orders resulted in a rise in the crude oil tanker order book during the past two months. This is quite amazing considering the present challenges in the market. As touched upon in a regular BIMCO news piece, a record 12 VLCCs were delivered in January. This inflow brought the VLCC fleet above 700 ships. For oil product tankers, 2016 was a six-year high for deliveries, with supply growing by 6.1\%. 2017 has seen the fleet grow by 1.3\% already, as it aims for 3.2\% for the full year. BIMCO expects demolition of oil product tanker tonnage to be 3–4 times higher than 2016, at 3 million DWT.

Outlook

As cargo volumes are not expected to grow that much in 2017, the increase in demand (if any) must come from longer sailing distances, and changes to the volumes from one country to the next. China rules the crude oil tanker market, as in many other shipping markets, having been solely responsible for the incremental crude oil tonne mile demand growth since 2010.

The country is set to do it again in 2017. What we have seen so far in terms of Chinese car sales, is supporting this. Though the subsidy has been reduced in 2017, the numbers are holding up. The US could spoil the party, however. As discussed above, US imports and domestic production have both contributed to rising crude oil stocks. A continuance of that could prove difficult to uphold. 2016 was an abrupt break of trend that has seen US seaborne crude oil imports drop consistently since their peak in 2005. 2017 is proving to be a year of change for oil tankers, as was indicated during 2016 with freight rates coming down. After two years of solid demand growth, 2017 is a year of tepid demand growth around 0–2\%. As fleet expansion is also slowing down, though still at a higher growth rate than demand, the shipowners have their work cut out. Managing the supply side is essential to ease the pain and avoid a marked dip in the fundamental balance that would take years to overcome.

Source: Peter Sand, Chief Shipping Analyst; BIMCO

DNV GL launches new PSC Planner application

The PSC Planner has been designed to help ship owners, managers and operators increase their operational efficiency by giving them an overview of a vessel’s or fleet’s PSC performance and to benchmark that performance against the IACS classed world fleet. It also helps the crew on board by showing them particular areas to focus on when they are preparing for their next inspection.

Claudia Ohlmeier, Group Leader Port State Control, DNV GL – Maritime

“The rise of risk based port inspection regimes means it is more important than ever for ships to keep a clean PSC record,” says Claudia Ohlmeier, Group Leader Port State Control, DNV GL – Maritime. “With the PSC Planner shore side and on board personnel can see both the big picture and ship specific details. Crews can easily access the inspection results of their vessel and trends at their next port of call, which lets them ensure they are focusing on critical areas, while onshore staff can easily see where their fleet ranks and can identify and prioritise items or underperforming vessels for targeted improvements. Ultimately this is all about working toward the goal of having a safe ship, with a good reputation, that is complying with the rules effectively and efficiently.”

The PSC Planner provides information on a vessel’s last PSC inspection as well as a summary of the results of all PSC inspections over the last 36 months. It also gives an overview of the PSC performance of both fleets and individual vessels, as well as benchmarking against the IACS classed world fleet.

For vessels that are in DNV GL class or use other DNV GL services, the PSC Planner offers extra tailored data. It shows customers the NIR (New Inspection Regime) risk factors for the Paris, Tokyo, and Black Sea MoUs and their PSC inspection priorities. For individual vessels, customers can check the Ship Risk Factor associated with calling at a selected port and the top PSC inspection priorities in any port.

Customers can also check a list of the top deficiencies their ship has received in the main PSC code categories and a list of the top deficiencies that have been identified in a selected port, in general and for the same ship type. The PSC Planner can also create a bespoke checklist for customers with the top ten focus items based on the ship and port so they can prepare optimally for individual vessel inspections, saving valuable time and effort.

You can find out more here: https://www.dnvgl.com/maritime/mydnvgl-service-overview/psc-planner.html

About DNV GL

Driven by our purpose of safeguarding life, property and the environment, DNV GL enables organizations to advance the safety and sustainability of their business. We provide classification, technical assurance, software and independent expert advisory services to the maritime, oil & gas and energy industries. We also provide certification services to customers across a wide range of industries. Operating in more than 100 countries, our professionals are dedicated to helping our customers make the world safer, smarter and greener.

About DNV GL – Maritime

DNV GL is the world’s leading classification society and a recognized advisor for the maritime industry. We enhance safety, quality, energy efficiency and environmental performance of the global shipping industry – across all vessel types and offshore structures. We invest heavily in research and development to find solutions, together with the industry, that address strategic, operational or regulatory challenges. For more information visitwww.dnvgl.com/maritime

![]()

Powered by ![]() © Μaritimes 2019

© Μaritimes 2019