The Marshall Islands Registry Recognizes Green Award Ships

In support of quality shipping and promotion of high environmental standards, the RMI Registry joined the Green Award scheme. Ships registered in the RMI and certified by Green Award will be granted a 30\% discount on the annual marine services fee.

|

The news was announced on 11 September 2018 at a festive welcome ceremony held in Athens. Green Award Chairman, Captain Dimitrios Mattheou, and Executive Director, Jan Fransen, presented a Green Award plaque to Theo Xenakoudis, Director, Worldwide Business Operations of International Registries, Inc. (IRI), which provides administrative and technical support to the RMI Registry. Captain Mattheou called this cooperation a huge step in the direction of an environmentally conscious and safe maritime industry of the future. “Striking a balance between economically sound and environmentally and socially responsible shipping is of paramount importance. That’s a task for the entire maritime community. By supporting Green Award, the RMI Registry joins the frontrunners of the industry actively taking measures to reduce their ecological footprint and encourage improvement of safety,” continued Captain Mattheou.

”Age is often an indicator of a greener fleet, and the RMI fleet is the youngest of any of the top 10 registries. We have always aimed to make our fleet environmentally friendly and so we are pleased to see that more than 16\% of Green Award vessels are RMI flagged. The RMI has also maintained its Qualship 21 status for 14 consecutive years and, in addition, more than 28\% of the United States Coast Guard’s E-Zero designation vessels are RMI flagged. It is noteworthy to see that so many RMI owners and operators are going beyond the industry’s standard for environmental performance measures,” said Mr. Xenakoudis.

Owners and operators interested in learning more about the RMI Registry’s new incentive for Green Award certified vessels can email This email address is being protected from spambots. You need JavaScript enabled to view it..

IRI is the world’s most experienced, privately held maritime and corporate registry service provider, specializing in the needs of the shipping and financial services industries across a broad commercial and economic spectrum. Headquartered just outside of Washington, DC in Reston, Virginia USA, IRI operates 28 offices in major shipping and financial centers around the world. The RMI Registry holds a leading position among the top five (5) flags worldwide with the most ships certified by Green Award.

Green Award is a voluntary international certification scheme for ships that go beyond the industry’s regulations in terms of safety, quality, and environmental performance. It provides a platform for maritime stakeholders to demonstrate the joint Corporate Social Responsibility and benefit from extra efforts invested in the improvement beyond legally required standards. Participation of the industry’s key stakeholders is crucial to recognize excellent ships and motivate others for improvement. The Marshall Islands Registry joining Green Award is a perfect example of such collaboration.

About IRI/The Marshall Islands Registry

International Registries, Inc. and its affiliates (IRI) provide administrative and technical support to the Republic of the Marshall Islands (RMI) Maritime and Corporate Registries. The RMI Registry is the second largest registry in the world, surpassing 162 million gross tons with 4,442 vessels at the end of August 2018.

IRI has a network of 28 worldwide offices located in major shipping and financial centers throughout the world that have the ability to register a vessel, including those under construction, record a mortgage or financing charter, incorporate a company, issue seafarer documentation, and service clientele.

The RMI fleet has received the highest ratings in port State control (PSC) international rankings. The RMI is on the White Lists of both the Paris and Tokyo Memorandums of Understanding (MoUs) and has also met the flag criteria for a low risk ship under the Paris and Tokyo MoU’s New Inspection Regimes. The RMI is the only major registry to be included on the United States Coast Guard’s (USCG’s) Qualship 21 roster for 14 consecutive years The RMI is the only one of the top three flag States that holds Qualship 21 status, an acknowledgment that is paramount for the RMI owners and operators.

The most important asset to the RMI Registry is its customers and IRI strives to provide them with full service from any office, 24 hours a day.

About Green Award Foundation

Green Award certifies sea-going oil and chemical tankers, bulk carriers, LNG and LPG carriers, container carriers, inland navigation barges and inland passenger ships. Its assessment criteria cover environmental, quality and safety aspects, and performance of management and the crew. With this comprehensive approach and a diverse team of the industry’s experts supporting the scheme, Green Award secures the quality of its audits and real value of its certificate.

With over 120 ports and other maritime related organisations providing discounts to the certified companies and ships, the scheme motivates ship owners and managers to invest in the improvements on board and ashore and serves as a reliable Corporate Social Responsibility and risk reduction tool for participating shipping companies, ports and maritime service providers.

www.greenaward.org

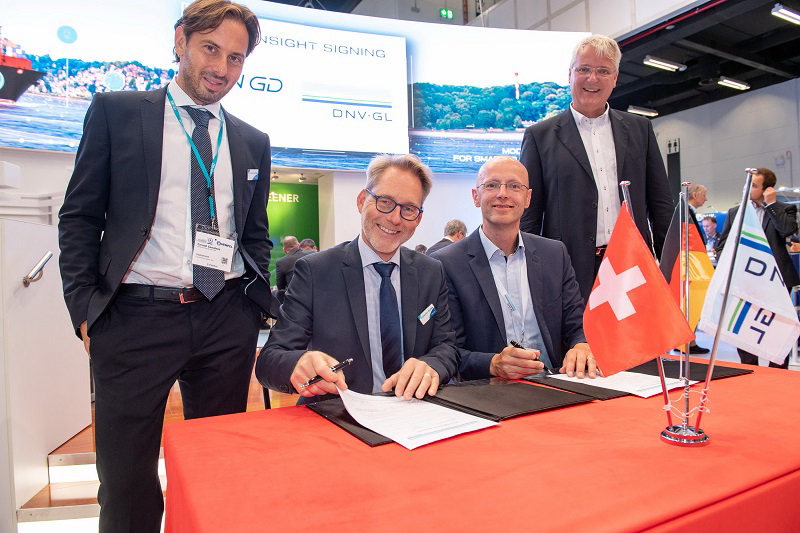

DNV GL at SMM 2018 WinGD, VAF Instruments and Viswa Lab connect to ECO Insight

“We are very much looking forward to cooperating with innovative companies like WinGD, VAF Instruments, and Viswa Lab,” says Torsten Büssow, DNV GL’s Global Head of Fleet Performance Management. “We want to offer an integrated solution for fleet performance that provides better analytics while streamlining the work of the crew onboard, by avoiding double data entry and additional administrative task.”

WinGD will deliver engine information and analytics to ECO Insight, while VAF Instruments as a manufacturer of thrust, power and fuel meters as well as propulsion performance monitoring solutions will support the accuracy of hull degradation assessments. Viswa Lab, as a fuel testing company, will directly feed fuel test results into ECO Insight to include fuel quality data, such as calorific value or water content in the performance assessment of vessels.

ECO Insight is the largest performance solution in shipping with installations on more than 2,000 vessels. In addition, already 22 industry partners connect their data and analytics to the solution. The data integration with all three new partners has already begun and will be completed soon for the first joint customers.

About WinGD: WinGD (stemming from Winterthur Gas & Diesel) is the leading developer of low speed gas and diesel engines for marine propulsion. Headquartered in Switzerland, since its inception as the Sulzer Diesel Engine business in 1893, it carries on the legacy of excellent design.

About VAF Instruments: VAF Instruments is the most preferred supplier of the top 100 shipyards and market leader in maritime measurement systems today. It has gained world-wide reputation as a specialist in developing, manufacturing and marketing systems that enable their clients to improve propulsion efficiency or assist to comply to regulations.

About Viswa Lab: As part of the Viswa Group, Viswa Lab has established itself as a “problem solving lab” and earned its reputation since its start in 1991, after consistently helping customers with detailed analysis of problem fuels and providing solutions for these fuels. Viswa Lab has been successfully accredited by ISO 17025 and ISO 17020.

About DNV GL

Driven by our purpose of safeguarding life, property and the environment, DNV GL enables organizations to advance the safety and sustainability of their business. We provide classification, technical assurance, software and independent expert advisory services to the maritime, oil & gas and energy industries. We also provide certification services to customers across a wide range of industries. Operating in more than 100 countries, our professionals are dedicated to helping our customers make the world safer, smarter and greener.

About DNV GL – Maritime

DNV GL is the world’s leading classification society and a recognized advisor for the maritime industry. We enhance safety, quality, energy efficiency and environmental performance of the global shipping industry – across all vessel types and offshore structures. We invest heavily in research and development to find solutions, together with the industry, that address strategic, operational or regulatory challenges. For more information visit www.dnvgl.com/maritime

Signing with WinGD and DNV GL (At table, L to R: Volkmar Galke, WinGD Global Head of Sales, Torsten Büssow, DNV GL Global Head of Fleet Performance Management)

Signing with VAF Instruments (Front L to R: Torsten Büssow, DNV GL Global Head of Fleet Performance Management, Douwe Vellinga, Marketing and Sales Director VAF Instruments)

Signing with Viswa Lab (Front L to R: Torsten Büssow, DNV GL Global Head of Fleet Performance Management, Simon Hall, Regional Sales Director, Viswa Lab)

DNV GL and DSIC sign JDP to develop LNG fuelled 23,000 TEU ultra large container vessel

|

| At the SMM trade fair today in Hamburg, Dalian Shipbuilding Industry Company Ltd. (DSIC) and classification society DNV GL announced the signing of a joint development project (JDP) agreement to develop a new 23,000 TEU LNG fuelled ultra large container vessel (ULCV). (L to R Signing the agreement were: Guan Yinghua, Deputy Technical Director DISC and Norbert Kray, Senior Vice President and Regional Manager for Greater China at DNV GL - Maritime) |

Interest in alternative fuels has moved from the margins to the centre of the maritime world as environmental regulations designed to reduce shipping’s emissions to air come into effect. For many operational uses, the combination of technical maturity, efficiency, availability, and emissions reduction mean that liquefied natural gas (LNG) is now a viable solution.

“In developing this new 23,000 TEU LNG fuelled ULCV design, we will show that DSIC can deliver vessels at the cutting edge of the market after two 20,000 TEU container vessels were successfully delivered to COSCO SHIPPING Group this year,” said Mr. Yang Zhi Zhong, President of DSIC. “We see a continuing strong market for ULCV vessels, with lower slot costs especially valued on the main trading routes. At the same time the expansion in bunkering infrastructure in both China and Europe means that LNG is becoming a viable solution for container vessels, lowering costs and ensuring compliance with incoming regulations.”

“We would like to thank DSIC for selecting DNV GL to take part in this project and trusting our expertise in LNG-fuelled and container shipping,” said Knut Ørbeck-Nilssen, CEO of DNV GL – Maritime. “The new JDP will build on the long and productive cooperation between DSIC and DNV GL, and we look forward to working with DSIC to ensure that the design meets the relevant class and international standards and regulations.”

DNV GL media hub for SMM: www.dnvgl.com/press18

About DNV GL:

DNV GL is a global quality assurance and risk management company. Driven by our purpose of safeguarding life, property and the environment, we enable our customers to advance the safety and sustainability of their business. Operating in more than 100 countries, our professionals are dedicated to helping customers in the maritime, oil & gas, power and renewables and other industries to make the world safer, smarter and greener

About DNV GL – Maritime

DNV GL is the world’s leading classification society and a recognized advisor for the maritime industry. We enhance safety, quality, energy efficiency and environmental performance of the global shipping industry – across all vessel types and offshore structures. We invest heavily in research and development to find solutions, together with the industry, that address strategic, operational or regulatory challenges. For more information visit www.dnvgl.com/maritime

DNV GL awards AiP to Jiangnan Shipbuilding Company for 175K CBM Mark III Flex LNG Carrier “LNG JUMBO”

“Jiangnan and DNV GL have successfully collaborated on joint design development and classification for various ship types, particularly in our star product gas carriers,” said Lin Ou. “We have completed China's first Mark III/Mark III Flex model tanks and moved into the membrane type liquefied gas carrier market. With this latest AiP, we have laid a solid foundation for introducing this ship type to the market and will further enrich our product portfolio in gas carriers and gas-fuelled ship types, which will benefit our clients and at the same time reduce emissions. Both Jiangnan and DNV GL will gain from the deeper and broader cooperation that this AiP represents.”

The ship uses the GTT Mark III Flex cargo containment system, and is equipped with four standard cargo holds, with a capacity of in total 175,000 cubic meters. The ship's shore connection is flexible and compatible with most shore facilities, and it can pass through the Panama Canal. The proposed WINGD X-DF low-pressure, low-speed two-stroke dual-fuel main engine propulsion system offers higher propulsion efficiency and lower fuel consumption in combination with an optimized twin skeg design and additional energy saving devices. In gas mode, the propulsion system meets IMO NOx Tier III requirements without the need for exhaust gas treatment systems. Additionally, a USCG certified ballast water treatment system means the design is ready for the incoming regulations.

“I am very pleased to be able to present this certificate to Jiangnan Shipyard, continuing a very productive and longstanding relationship,” said Knut Ørbeck-Nilssen. “Jiangnan Shipyard had been continuously developing their ability to offer new and advanced vessel designs and we are very proud to have been part of this process. As the gas segment continues to gain importance in shipping, new designs that offer greater efficiency and compliance alongside safety are important in advancing the segment, and we are very proud to support Jiangnan Shipyard in realizing this new concept.”

About DNV GL

Driven by our purpose of safeguarding life, property and the environment, DNV GL enables organizations to advance the safety and sustainability of their business. We provide classification, technical assurance, software and independent expert advisory services to the maritime, oil & gas and energy industries. We also provide certification services to customers across a wide range of industries. Operating in more than 100 countries, our professionals are dedicated to helping our customers make the world safer, smarter and greener.

About DNV GL – Maritime

DNV GL is the world’s leading classification society and a recognized advisor for the maritime industry. We enhance safety, quality, energy efficiency and environmental performance of the global shipping industry – across all vessel types and offshore structures. We invest heavily in research and development to find solutions, together with the industry, that address strategic, operational or regulatory challenges. For more information visit www.dnvgl.com/maritime

Awarding the AiP at the SMM Trade Fair in Hamburg. First row from left to right: Hu Keyi, Chief Engineer of Jiangnan Shipyard; Knut Ørbeck-Nilssen, CEO of DNV GL – Maritime; Lin Ou, Chairman & President of Jiangnan Shipyard.

The LNG Jumbo design. Image care of Jiangnan Shipyard

China tops the table: DNV GL and Menon Economics release “Leading Maritime Nations of the World” 2018

|

| “The Leading Maritime Nations of the World” report was released at the SMM trade fair in Hamburg today. |

The new report follows up the 2017 report by Menon and DNV GL on the “Leading Maritime Capitals of the World”, but shifts the focus to an extensive review of the maritime industry at the national level. The 30 nations were ranked by size and magnitude on all four key maritime pillars and their subgroups. As the shipping sector is the main engine of the entire maritime industry, more weight was given to the shipping sector.

The 2018 report ranks China as the world’s leading maritime nation, due to its top four ranking in all of the maritime pillars. China’s position is particularly strong on the ports and logistics pillar, with the world’s largest container and bulk ports. “The strength of China is overwhelming, particularly on the pillar of ports and logistics, but also in shipping,” says Erik W. Jakobsen, Managing Partner in Menon Economics and co-author of the report. “It should not surprise us, though, since China is the largest exporting and importing country of the world. The other economic superpower, USA, follows China on the ranking, with major ports and maritime cities both on the east and west coast.”

USA is placed second, scoring high on all four dimensions, followed by Japan. Germany, Norway and South Korea, share the 4th place. Germany’s strength lies in its consistency, with a top 5 spot in three categories, whereas Norway has its strongest position within Maritime Finance & Law and maritime technology. South Korea scores top in Maritime Technology and is among the top 10 in Shipping and Ports & logistics.

"For the top 3 maritime nations, the study’s rankings mirror the size of their national economies,” says Shahrin Osman, Regional Head of Maritime Advisory for South East Asia, Pacific and India, at DNV GL Maritime, who co-authored both the 2017 and 2018 reports. “Interestingly however, in the joint fourth position of Norway, South Korea, and Greece in the 7th position, we can see that ‘smaller’ countries can still have an outsize influence and importance to the maritime world, due to their traditions, history and innovations. We hope that this report will be a valuable resource for national maritime authorities or governmental ministries, serving as an inspiration, a benchmark, and demonstrating a development path to leadership in the shipping world.”

Download a copy of the full report and watch a short video on the new report here: https://www.dnvgl.com/maritime/webinars-and-videos/videos/lmn18.html

DNV GL media hub for SMM: www.dnvgl.com/press18

About DNV GL:

DNV GL is a global quality assurance and risk management company. Driven by our purpose of safeguarding life, property and the environment, we enable our customers to advance the safety and sustainability of their business. Operating in more than 100 countries, our professionals are dedicated to helping customers in the maritime, oil & gas, power and renewables and other industries to make the world safer, smarter and greener

About DNV GL – Maritime

DNV GL is the world’s leading classification society and a recognized advisor for the maritime industry. We enhance safety, quality, energy efficiency and environmental performance of the global shipping industry – across all vessel types and offshore structures. We invest heavily in research and development to find solutions, together with the industry, that address strategic, operational or regulatory challenges. For more information visit www.dnvgl.com/maritime

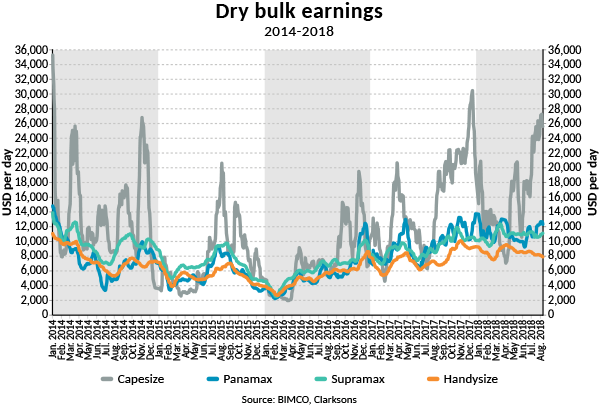

Dry bulk shipping: An improving market, even as iron ore imports slip and the fleet grows faster

After a steady decline since April, earnings for handysize ships slipped back into lossmaking territory on the very last day of July – and rates have kept sliding in August. In sharp contrast, the capesizes have turned around a fairly weak start to the year, and are now at USD 16,019 per day on a year-to-date average per 10 August. Disregarding the short spike in December 2017, capesize earnings are managing to stay at a high level not seen since March and November 2014.

One of the drivers in the market during the first half of the year has been US coal exports, which were up by 31\% in the first six months, peaking at 10 million tonnes in April. In early August, international coal prices started to weaken, but remain at a high enough level for US exports of thermal and coking coal to be attractive for buyers – especially in the Far East. BIMCO expects this to remain a driver, unless coal prices drop to a level that price out US coal for Asian buyers.

In 2012, US coal exports were generating more tonnes miles than Chinese coal imports. While US exports have rebounded since Q3-2016, current tonnes-miles demand remains below previous highs.

The usual mega driver, Chinese imports of iron ore, is disappointing this year. It started at the second-highest imports level on record in January, only to deliver fairly steady – but a bit lower – volumes from there onwards, compared to last year. Total imported iron ore volumes are down by 0.8\% in the first seven months from last year. The slowdown has been going on for more than a year now, with H2-2017 volumes only 0.96\% higher than H2-2016.

In recent years, Chinese steel mills have delivered an unchanged output, but the switch away from domestically mined iron ore caused imports to keep growing. This year, China’s steel production is at a record high level, as more efficient mills are opening. High production is also coming on the back of strong steel-producing margins. Many of these mills are electric arc furnaces (EAF), which make steel out of scrap iron. China has always preferred blast furnace (BF) production to EAF, but EAF output has rapidly increased recently and now affects shipping. This results in more steel produced without more iron ore and coking coal needed in the process.

If that is a sign of what’s to come, Chinese iron ore imports could begin to drop faster than we have seen so far in 2018. China’s availability of scrap steel is forecast to double from 2015, to reach 300 million tonnes by 2030 (source: World Steel Association). Note that China may still be cutting absolute steel-production capacity, but it is overcapacity and substandard capacity they are cutting – not production output.

Supply

Monthly year-on-year growth data for the dry bulk fleet shows that the slowing expansion has bottomed out. Since the end of March, the fleet has grown by an average of 2.2\% compared with the same month last year. The change in trend comes on the back of stablising capesize fleet growth, and the return of a growing panamax fleet. The latter is mainly a result of the sudden and almost complete end to demolition activity involving the 65,000-99,999 DWT workhorses of the fleet. Only 8\% (214,000 DWT) of total demolished capacity in 2018 were panamaxes, down from 24\% in the past four years.

Across the board, demolition of dry bulk ships has slowed to a trickle: only 2.6m DWT has been demolished. This compares with 14.7m DWT in 2017 and 29.5m DWT in 2016. It’s a crystal-clear reflection of higher freight rates that now stop owners from scrapping ships.

The halt in demolition activity also means that we need to revise upwards our fleet-growth estimate for 2018. This narrows the improvement of the fundamental balance. Where the former is down to human nature in the shipping market (not handling the supply side with care), the latter relates somewhat to the trade war, the drought in Europe and Australia limiting grain exports, and China growing its iron ore imports more slowly than forecast.

The fleet will now grow by 2.7\% if our revised demolition estimate of just 5m DWT is realised.

Looking into 2019, a sensitivity analysis shows that a reduction of demolition in 2019 – to 5m DWT from 9m DWT (estimated) currently – will lift the fleet growth to 2.3\%, which is also above our long-term estimate of demand growth.

Our previous dry bulk report was titled ‘No more room for newbuilds’. Three months have passed since then and 5.8m DWT has been ordered during that time; 14 of 24 ships were panamax and six were capesizes. BIMCO has long held the view that demand growth is better for the larger ship sizes compared with the smaller ship sizes, but if overcapacity reigns that upside will never materialise.

Outlook

When profits finally arrive, everyone breathes a sigh of relief. Several years of very bad markets have come to an end, but how do we retain the profitable freight rates? We all know the answer – make sure fleet growth does not exceed demand growth.

In 2018, demand has outpaced fleet growth and year-to-date (10 August) panamax average earnings stand at USD 11,181 per day, up from USD 8,654 (+29\%) per day. You could argue that owners should have kept up the pace of demolition, making an extra USD 1,000-2,000 per day on the 11,000+ ships in the fleet. But as the industry is so fragmented, with thousands of owners globally, every ship is important to its owner. As you can’t scrap one-quarter of a ship, the industry relies on the larger owners to do ‘the right thing’ to balance the markets by means of demolition. In 2017, 121 shipowners scrapped 219 ships. In 2018, a mere 34 shipowners sold 37 ships for scrapping – the lowest level since 2007.

The trade war has already taken many dry bulk commodities hostage. More tariffs were due to come into force on 23 August, as additional US dry bulk products get tariffed by China – whereas no new Chinese dry bulk products have been hit by new US tariffs. The amount of US dry bulk commodities included in this round is much higher than originally proposed, as a last-minute removal of crude oil from the list was swapped for more dry bulk commodities.

What comes next? More dry bulk commodites are being tariffed by both parties in the trade war. Full disclosure of this is found in a separate and updated BIMCO overview of the trade war and its impact on shipping.

As we close in on the fourth quarter, and the US soya bean export season, the real effects of one of the main tariffed commodities will be exposed. What we know right now is that Brazilian exports have been higher than last year, but – so far – they remain nowhere near a level where they can fully substitute for US exports to China.

Other negatives coming out of the trade-restrictive measures are the protective actions taken by EU to shield its steel market and industry against steel that would have been imported by the US, but now seeks a new buyer. India is rumoured to be following suit.

As demand for transportation of dry bulk commodities increases throughout the year, BIMCO expects the recovery of freight rates to continue slowly but steadily. Expect higher volumes for coal, iron ore and wheat to dominate the market in the second half of the year.

source:BIMCO

Peter Döhle Schiffahrts-KG signs agreement with ERMA FIRST for BWTS

After a thorough review of the different Ballast Water Treatment Systems (BWTS), Peter Döhle Schiffahrts-KG has decided to partner with ERMA FIRST for the delivery of its approved BWTS on their entire fleet, comprised of different sizes and types of vessels, including but not limited to Bulk Carriers and Container Vessels.

Konstantinos Stampedakis, Managing Director of ERMA FIRST commented: ‘It is our honor to work with such a well-esteemed company. Our aim is to provide a full service package that includes regulation compliance, low capital costs, system operation simplicity, low energy requirements and a vast after sales support network, in order to make sure that both parties remain satisfied and our mutual benefits are met. We are confident that we will meet our customer’s needs at the most professional and efficient way.”

The ERMA FIRST BWTS FIT is USCG type approved and IMO approved for all water types. The system is simple, flexible, and suitable for small and large ballast-pump capacities. In addition, it comes with a small footprint and low power consumption.

During ballasting, the water goes through the filter, where organisms and sediment (with a diameter larger than 40 microns) are separated and further discharged overboard. The filtered water enters the Electrolytic Cell. Naturally, from the chlorides of the water, free chlorine is produced through the electrolysis process at a very low concentration (around 4-6 mg/L). The treated water then, enters the ballast tanks. During de-ballasting, the system will only monitor the residual oxidants and will further intervene if necessary. The main stages of the system (filtration and disinfection) are bypassed.

|

|

First class approval programme for AM manufacturers

“AM is a technology that holds a great deal of promise for the maritime industry,” says Knut Ørbeck-Nilssen, CEO of DNV GL – Maritime. “Our responsibility as the world’s leading classification society is to give manufacturers a clear path they can take to offer their innovative products, while ensuring that our customers can have the same confidence in an AM product as they do in any other that has undergone approval by class.”

The AoM programme is designed to verify a manufacturers’ ability to consistently manufacture materials and products to given specifications and in accordance with the DNV GL rule requirements. As part of applying for AoM, manufacturers must firstly undertake a proof of concept to demonstrate that they have feasible technology and products.

“The release of the AoM programme opens up new opportunities for both producers and users of these products, creating potential efficiencies in logistics and supplies chains, as well as in on-board maintenance and repair,” says Knut Ørbeck-Nilssen. “Above all, however, we must ensure that safety and quality standards are upheld, and this new programme allows producers to demonstrate their fitness to the shipping industry.”

DNV GL has been investigating the opportunities and challenges posed by AM since 2014. In 2017, DNV GL published the first guideline for the use of AM in the maritime and oil & gas industries. Earlier this year DNV GL opened the Global Additive Manufacturing Centre of Excellence in Singapore, an incubator and testbed for the research and development of additive manufacturing technology for the oil & gas, offshore and marine sector.

To find out more go to: http://dnvgl.com/am

DNV GL media hub for SMM: www.dnvgl.com/press18

About DNV GL:

DNV GL is a global quality assurance and risk management company. Driven by our purpose of safeguarding life, property and the environment, we enable our customers to advance the safety and sustainability of their business. Operating in more than 100 countries, our professionals are dedicated to helping customers in the maritime, oil & gas, power and renewables and other industries to make the world safer, smarter and greener

About DNV GL – Maritime

DNV GL is the world’s leading classification society and a recognized advisor for the maritime industry. We enhance safety, quality, energy efficiency and environmental performance of the global shipping industry – across all vessel types and offshore structures. We invest heavily in research and development to find solutions, together with the industry, that address strategic, operational or regulatory challenges. For more information visit www.dnvgl.com/maritime

Additive manufacturing is a term that covers industrial processes that create three dimensional objects by adding layers of material.

IMO 2020: mayhem or opportunity for the refining and marine sectors?

The IMO, the United Nations’ body responsible for the safety and environmental performance of the shipping sector, has ruled that from 1 January 2020, marine sector emissions in international waters be slashed.

To comply, the marine sector will have to reduce the sulphur emissions by over 80\%, which can be achieved by switching to lower sulphur fuels. The current maximum fuel oil sulphur limit of 3.5 weight per cent (wt\%) is to be reduced to 0.5 wt\%. The new tougher limits will be the largest reduction in the sulphur content of a transportation fuel undertaken at one time.

Scale of the Issue

The marine sector, which consumed 3.8 million barrels per day (b/d) of fuel oil in 2017, is responsible for half of global fuel oil demand. Most of this fuel oil has a sulphur content of between 1 and 3.5wt\%, making it a high-sulphur fuel. The marine sector also consumes just over 1 million b/d of marine gas oil, which is a lower-sulphur, higher-value distillate. However, this represents just 5\% of the global demand for diesel and gas oil demand, the majority of which is consumed in the heavy-duty trucking sector.

If the marine sector fully complied with the IMO regulation by simply switching from high-sulphur fuel oil (HSFO) to marine gas oil, the impact on the refining sector would be dramatic.

Firstly, the strong surge in distillate demand caused by the replacement of HSFO would require refineries to run at high utilisation, which becomes increasingly costly.

Secondly, the value of HSFO would collapse until it found an outlet in lower-value end-uses. At the right price – around US$20 per barrel, less than a third of its August 2018 price level – it could compete with coal for electrical power generation.

Distillate prices would need to increase, in part to make up the shortfall from lower revenues from HSFO now priced at distressed levels and then to support the costs of higher refinery utilisation. This price spread between HSFO and distillate could increase by a factor of four from its current level of US$25 per barrel. This should provide a huge incentive for refiners to invest to upgrade HSFO to either a 0.5wt\% sulphur fuel oil (termed VLSFO, very low sulphur fuel oil), or distillate. However, there is little such investment under way.

Options for the marine sector

The IMO is working with its member states to develop a regulatory framework that will achieve full compliance. But this is complex, given the fragmented nature of the marine sector and that non-compliance would happen in international waters, far from land.

Even with the forthcoming introduction of a carriage ban – ships are not permitted to have non-compliant fuels in their bunker tanks, with the regulation enforced by the port authority – it is difficult to envisage full and immediate global compliance.

The ways in which the marine sector can comply without needing to purchase marine gas oil include:

-Buying VLSFO, if available;

-Switching propulsion systems to other fuels, such as liquefied natural gas, which is an option for new-build vessels;

-Installing exhaust gas cleaning facilities (termed “scrubbers”), which enable the shipper to continue to burn cheaper HSFO by washing the exhaust gases to reduce the SOx emissions.

The key difficulties are the uncertainty around compliance and that refining and marine investments are in direct competition, prompting a “wait and see” approach from both sectors. Wood Mackenzie believes the installation of commercial scrubbers has the advantage of being less expensive. It would also be faster to put in place than a major refining upgrade, which is highly capital-intensive and can take many years to implement.

Refining sector implications

Wood Mackenzie believes that global compliance with the new IMO regulation will reach about 80\% in 2020.

Our analysis indicates that more than 2 million b/d of HSFO will be displaced from the bunker sector. However, some of that can be re-blended to produce a compliant VLSFO, but VLSFO will be priced at a premium to crude, rather than the typical discount.

Displaced HSFO can be processed within the global refining system’s spare residue upgrading capacity, but its discount to crude needs to widen to make using this spare capacity economical.

Once the regulation comes into force, the bunker sector will need more than 1 million b/d of additional marine gas oil. However, its pricing premium to crude needs to widen to cover both refiners’ revenue shortfall from the weakening of HSFO prices and the extra costs of higher refinery utilisation.

Wood Mackenzie also believes that by 2020, the price differential between gas oil and HSFO will be roughly double the 2017 differential. That makes a decision by the marine sector to opt for scrubbers commercially attractive.

This shift in refined product pricing results in:

-Crude differentials changing, with the discounts for medium and heavy/sour crudes (to Brent) widening significantly;

-Sweet/sour crude differentials changing, but primarily for those very low sulphur crudes that can produce a VLSFO;

-Refining margins increasing, but the impact is unevenly distributed. Those doing best will have sophisticated refineries that capture the feedstock advantage (by processing heavy sour crudes and importing heavy residues) and also the product premiums (by not producing fuel oil and having a high distillate yield).

However, there are many uncertainties around the compliance levels and the ways in which VLSFO can be supplied. Given the scale of the change, the oil value chain is likely to see high volatility during 2020.

The countdown to 2020 begins

The IMO’s regulatory change to the emissions of the international marine sector has the potential to be highly disruptive to the pricing and availability of compliant fuels. The costs of ocean going freight will increase as the marine sector uses more costly fuels, which has wide reaching consequences across the global economy.

Given the need for compliance on 1 January 2020, the impact could well be felt from mid-2019 onwards and last for a few years, as the refining and shipping sectors determine how to survive and best adapt.

Source: Wood Mackenzie

“Bad” bunkers in the US Gulf, Caribbean and Far East

|

Certain compounds – phenols and fatty acids, amongst others – have been identified in the fuel which have reportedly led to engine problems. The operational issues generally involve excessive formation of sludge or sediments, linked to the blocking of filters and fuel pumps and eventually damage to engine components.

As yet there is no clear explanation as to how these compounds would cause these reported problems.

Samples and time bars

Identifying and retaining the relevant samples for analysis is critical. The bunker supply contract, for example, may provide that the sample retained by the bunker barge is binding for the purposes of determining quality; such contracts also typically have a short deadline for notification of quality disputes failing which the claim may be time barred. The charterparty may contain its own provisions regarding the samples which are to be determinative in terms of quality.

Given the range of tests that may be necessary (explained further below), parties stemming bunkers at affected ports should endeavour to ensure that the samples taken during bunkering are sufficient (using one litre bottles as a minimum). It is recommended that the crew closely monitor the sampling procedure and check that the samples from the delivering barge are properly collected. In cases where problems have already occurred, consideration should be given to taking further samples on board the vessel, including of any sludge or sediment which may have developed.

What do the fuel specifications say?

Fuel of this type is typically supplied under the ISO 8217 standards. We understand the most commonly used are the 2005 and 2010 editions, although there are more recent editions issued in 2012 and 2017.

These specifications all provide for routine testing of certain parameters such as density, water and ash content etc. (known as “Table 2” tests). However, these standard tests do not identify the presence of the compounds referred to above. Indeed there is no general test for the presence of these compounds, but various methods have been used which can identify unusual chemicals. These include:

Fourier Transform Infra Red (FTIR). This technique is useful for identifying classes of various chemicals in relatively large amount in the fuel (but does not identify individual chemicals).

Direct injection gas chromatography-mass spectrometry (GC-MS).

Headspace GC-MS. (This can identify some volatile chemicals which may not be seen in direct GC-MS).

SPE polar extraction followed by derivatisation and GC-MS.

Often a combination of these tests provides the best chance of identifying any “unusual” materials in the fuel. To the extent that such materials are identified, the relevant provisions of the specification are Clause 5 and (in the 2010 and subsequent editions) Annex B, which have three relevant requirements:

(i) That the fuel be a “homogenous blend of hydrocarbons derived from petroleum refining” (the 2017 edition refers to the fuel consisting “predominantly” of such hydrocarbons);

(ii) That the fuel be free of any added substance or chemical waste which adversely affects the performance of the machinery; and

(iii) Annex B notes that determining the harmful level of any “deleterious materials” is not straightforward, and provides that supply facilities should “have in place adequate quality assurance and management of change procedures to ensure that the resultant fuel is compliant with the requirements of clause 5”.

While determining the precise quantity of any unusual compounds is challenging and there is no common expert guidance on what amount (if any) of a given compound is safe, Clause 5 provides a greater degree of protection for the purchaser in this context than the “Table 2” tests.

Worryingly however we are now starting to hear that suppliers are in some instances revising supply contracts to eliminate Clause 5. Given the broader requirements of Clause 5 over the particular specifications identified by the Table 2 tests, this will have the effect of significantly reducing a purchaser’s recourse against the supplier because, in simple terms, under the supply contract the supplied fuel will be within the contractual specification (assuming it meets the Table 2 tests) even if it fails the wider Clause 5 requirements.

It is also easy to imagine a situation where a time charter party includes the Clause 5 requirements as part of the bunker specification clause but where the time charterer, perhaps unwittingly, purchases fuel where Clause 5 is omitted from the bunker supply contract. In such a situation and assuming the bunkers were ‘off-spec’ under the broad Clause 5 requirements, the time charterer could under the charterparty be held liable for any losses suffered by the owners but without any recourse to the supplier.

We therefore recommend that the purchasers of such bunkers, be they owners or time charterers, check carefully that Clause 5 is included in the supply contract before purchase.

Solutions

There are myriad legal and technical issues arising out of the above, which will vary depending on the terms of the relevant charterparty and bunker sale contract, and the jurisdiction regulating any possible tort claims between the physical supplier and the receiving vessel. The Club is involved on behalf of its members and customers in a significant number of disputes in various jurisdictions.

Where our members and customers are affected, we encourage them to contact their dedicated claims handler for specific advice on their case and on practical solutions which may be available to resolve any dispute.

Source: Skuld

![]()

Powered by ![]() © Μaritimes 2019

© Μaritimes 2019